THE Malaysian Automotive Association (MAA) reported that November 2025 total industry volume (TIV) jumped 29.9% month-on-month (MoM) to 75.9k units, driven by a low base in October, a rush to purchase imported BEVs ahead of the expiry of tax-exemption in end-2025, and strong year-end promotions.

Jabatan Pengangkutan Jalan Malaysia (JPJ) registration data also showed BEV registrations rising 23% MoM to 4.3k units in October. Passenger vehicle sales climbed 31.8% MoM to 70.3k units, while commercial vehicles rose 10.4% MoM to 5.7k units.

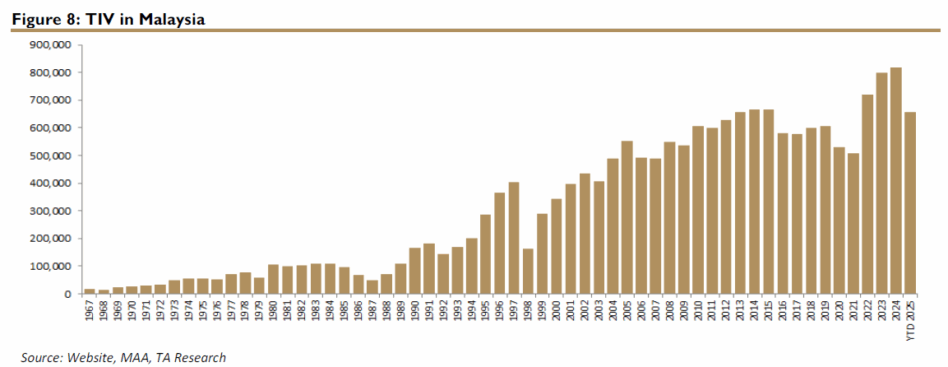

However, cumulative 10M2025 TIV slipped 1.8% YoY to 655.3k units, as softer demand in both passenger (-0.9% YoY) and commercial (-12.6% YoY) segments reflected moderated consumer sentiment and cautious business spending.

National passenger vehicle sales rose sharply in October 2025, increasing 36.5% MoM to 49.1k units, supported by stronger deliveries from both Perodua and Proton. Perodua posted a robust 45.8% MoM rebound to 34.1k units, while Proton improved 19.1% MoM to 15.0k units, aided by sustained demand across its core models.

On a YoY basis, national marques delivered a steady 6.8% growth. However, cumulative 10M2025 national passenger vehicle sales slipped marginally by 0.5% YoY to 414.3k units, dragged mainly by Perodua’s softer volumes (-1.7% YoY), while Proton continued to chart positive momentum with a 2.2% YoY improvement to 125.1k units.

Non-national passenger vehicle sales saw a strong rebound in October 2025, rising 22.1% MoM to 21.2k units, with most of the major marques posting sequential improvements.

Honda led the recovery with a 51.5% MoM jump to 6.6k units, while Mazda also recorded a sharp 42.7% increase. Toyota’s sales improved 13.6% MoM, though its YoY performance remained soft.

Nissan was the notable laggard, declining 30.7% MoM. On a YoY basis, the non-national car sales rose 5.4%, supported by stronger contribution from Honda.

Cumulatively, 10M2025 non-national car sales eased 1.5% YoY to 192.1k units, weighed by weaker volumes from Honda (-15.6% YoY), Toyota (-5.1% YoY) and Mazda (-44.3% YoY), while Nissan delivered a modest 3.7% YoY contraction.

As highlighted previously, the Malaysian automotive market remains highly competitive, with manufacturers offering aggressive promotions to attract buyers. This intensifying competition, coupled with the final push to achieve sales KPI alongside clearing 2025 inventory will likely be the trend for the remainer of 2025.

Following the stronger-thanexpected TIV in October, we now revise our 2025 full-year TIV forecast to 800k units (-2.1% YoY) from 750k. Our sector stance and stock recommendation are currently under review (UR) pending the release of quarterly results and analyst briefings. —Nov 21, 2025

Main image: intech