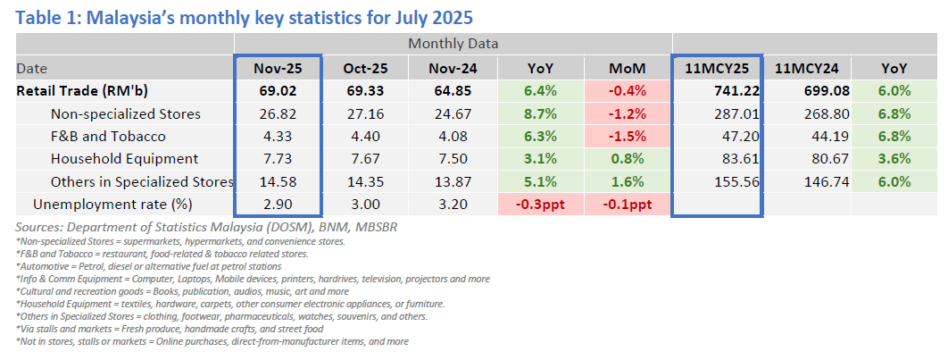

MALAYSIA’s retail trade rose +6.4% year-on-year (yoy) to RM69.02 bil in Nov-25, supported by continued year-on-year growth across most sub-segments despite a modest month-on-month (mom) pullback of -0.4%.

Non-specialised stores remained the main growth driver at +8.7%yoy, alongside food, beverages & tobacco (+6.3%yoy) and other specialised stores (+5.1%yoy), while household equipment saw firmer growth of +3.1%yoy.

Sequentially, softer spending was observed in nonspecialised stores (-1.2%mom) and F&B & tobacco (-1.5%mom), partly offset by gains in other specialised stores (+1.6%mom) and household equipment (+0.8%mom).

Cumulatively, the 11 months of calendar year 2025 (11MCY25) retail sales expanded +6.0%yoy to RM741.22 bil, underscoring sustained household consumption momentum, albeit with signs of normalisation before the holiday season in December.

Malaysia’s labour market strengthened in Nov-25, with the unemployment rate easing to 2.9%, marking an 11-year low.

Employment growth remained firm at +3.1%yoy, continuing to outpace labour force expansion of +2.8%yoy for the 52nd consecutive month, underscoring sustained job creation and resilient labour demand.

On prices, headline CPI edged slightly higher to +1.4%yoy, while core CPI was unchanged at +2.2%yoy, signalling still-manageable underlying inflationary pressures. Overall, a tight labour market and moderate inflation continue to support household

purchasing power and underpin steady private consumption momentum. Anchored by a tight labour market, manageable inflation and continued fiscal backing under the Ekonomi MADANI framework.

Enhanced STR and SARA allocations in Budget 2026 are expected to sustain disposable income and consumption, particularly across the mass-market segment, while tourism-related initiatives ahead of Visit Malaysia Year 2026 should provide incremental support to retail and F&B activity in key urban and tourist locations.

Combined with ongoing job creation and more accommodative financing conditions post-OPR cut, the consumption backdrop remains constructive.

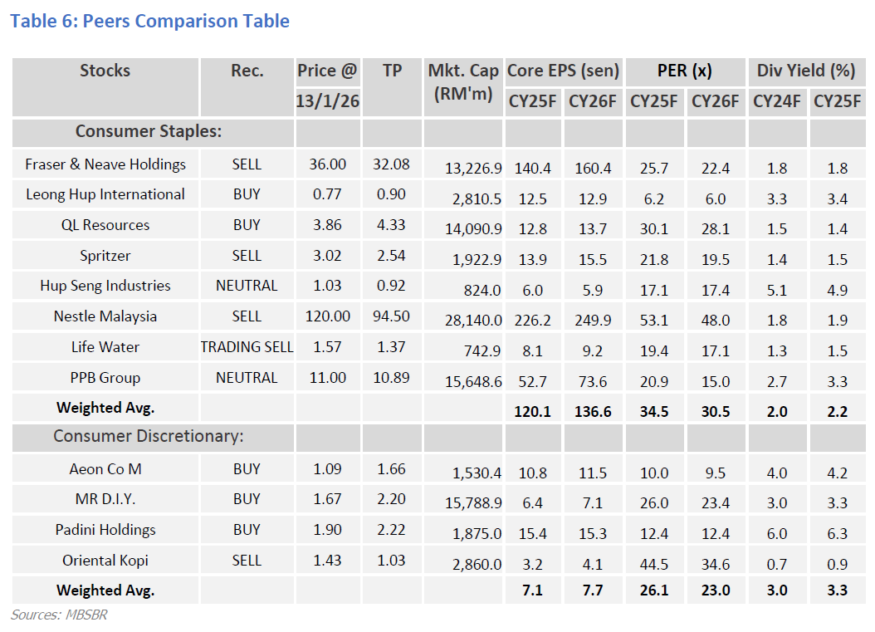

Within the sector, AEON remains a key pick for its defensive mass-market exposure and stable PMS income, MR DIY for its resilient value-driven retail model, and Leong Hup International for leveraged exposure to steady regional staple food demand. —Jan 14, 2025

Main image: Extensiv