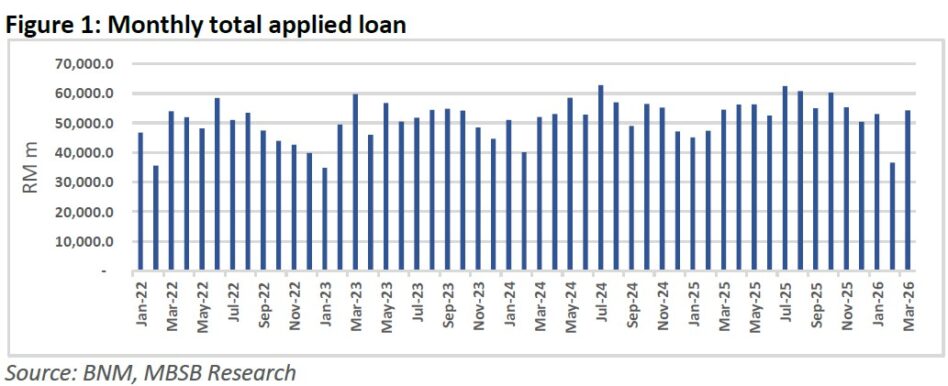

THE LOCAL property market showed signs of stabilisation in March 2026, with housing loan applications rebounding sharply after a subdued February, though analysts caution that mounting inflationary pressures and rising property overhang could cloud the sector’s near-term outlook.

Total loan application for purchase of property recovered to RM54.2 bil in March 2026 after a sharp decline of 30.9% month-on-month (mom) in February 2026.

Note that the easing loan demand in February 2026 was due to the shorter month of February and impact of festive holidays on loan demand.

Meanwhile, loan application was flattish on a year-on-year basis, easing by -0.5% year-on-year (yoy) in March 2026 as loan applications softened amid geopolitical tensions from the US–Iran conflict.

Cumulatively, loan applications were softer in quarter one calendar year 2026 (1QCY26) at RM143.9 bil (-2% yoy).

“Going forward, we may see softening buying interest on properties in the near-term as higher fuel costs are expected to drive inflationary pressure and dampen affordability among homebuyers,” said MBSB Research.

Approved loan for purchase of property increased to RM22 bil (+40.7%mom) in March 2026 after declining by 29.6%mom in February 2026.

The increase in approved loan was mainly due to rebound in loan applications.

On a year-on-year basis, approved loan declined by -5.4%yoy in March 2026, mainly dragging by the lower approval ratio of 40.6% in

March 2026 as compared to approval ratio of 42.7% in March 2025.

Cumulatively, total approved loans were little changed at RM59.9 bil (+0.1%yoy) in 1QCY26.

Looking ahead, approved loan growth is expected to remain subdued, driven by softer loan application momentum.

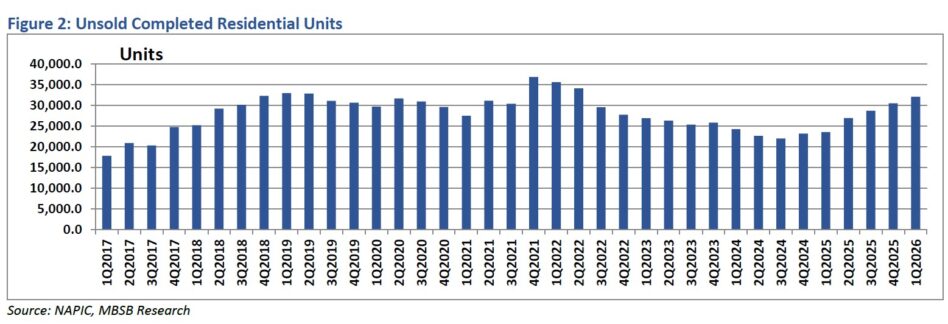

According to data released by National Property Information Centre (NAPIC), unsold completed residential units continue to increase, climbing to 32,801 units in 1QCY26 from 30,471 units in 4QCY25.

The increase in unsold completed residential units was mainly contributed by higher unsold completed residential units in KL (+1,678 units), Malacca (+471 units) and Pahang (+445 units).

Meanwhile, Perak has the highest unsold completed residential units of 4,063 units, followed by Johor (3,852 units), Selangor (3,745 units), KL (3,733 units) and Penang (3,165 units).

Residential property overhang has seen a renewed uptick after increasing for sixth consecutive quarter since 4QCY24 as supply continues to outpace demand.

The uptrend has resulted in residential property overhang levels reaching a three-year high.

Similarly, serviced apartment overhang has also risen to 19,263 units in 1QCY26 from 18,752 units in 4QCY26 as serviced apartment overhang in KL and Johor increased.

“Overall, we see the rising property overhang presents downside risks to the sector as the higher unsold completed properties may slow launches of developers going forward,” said MBSB.

MBSB sees that property purchasing sentiment may moderate amid inflationary pressures.

While they see that 1QCY26 earnings for developers to be largely in line and supported by higher sales secured in 2024 and 2025, MBSB thinks that the oil price hike should compress margin of developers in the second half of 2026.

Meanwhile, the research house thinks that the increasing property overhang to the highest level since 3QCY22 poses a headwind to developers.

“Hence, we maintain our Neutral stance on the sector,” said MBSB. —May 19, 2026

Main image: The Economic Times