AN improved or worsening economic outlook remains the core rerating driver. An overly negative result increases the likelihood of further overnight policy rate (OPR) cuts, which are bad for earnings and valuations.

The usual themes persist: Headwinds such as net interest margin (NIM) compression, possible asset quality and provisioning issues, and weak economic growth prospects afflict the industry, while tailwinds vary on a case-by-case basis.

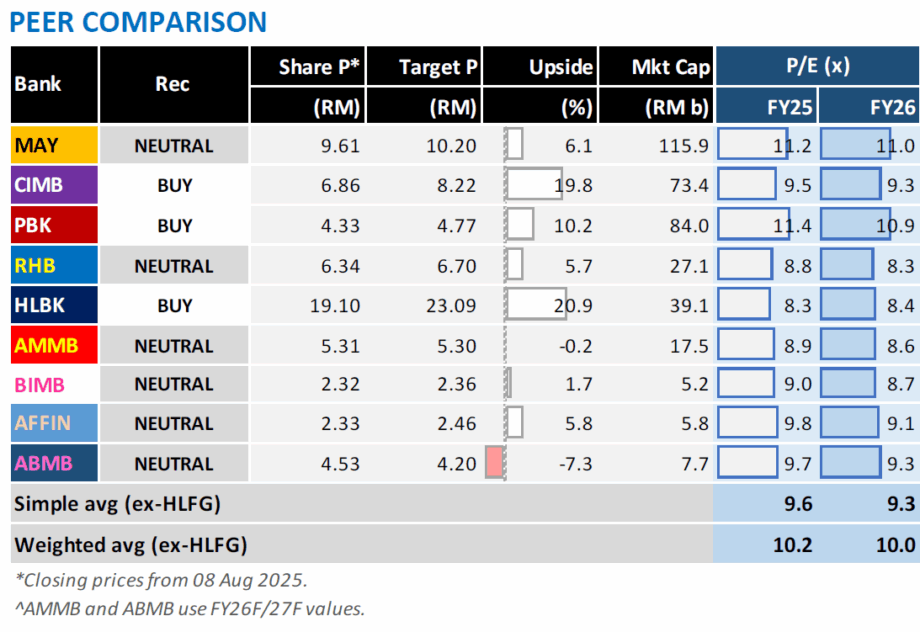

“Hence, we continue to advocate for our bottom-up approach to stocks with a preference for defensive names,” said MBSB Research.

Most banks should see NIM compression coming from the recent OPR hike. We are not expecting anything overly dramatic.

There is some offset coming from SRR relaxation. The liquidity situation is said to improve in the second half of calendar year 2025 (2HCY25).

A few banks believe that they are poised to outperform others on this front. Namely, AFFIN and RHB, which are both expecting to see a large influx of current account savings account balances this quarter.

We are expecting a strong non-interest income (NIM) quarter, as positive bond yield movements and currency volatility bode well for the trading and forex income front.

While some banks are guiding for improving fee income momentum, poor market conditions this quarter could impact unit trust and private banking segments.

AMMB management has guided for this in their recent results day. PBK may also be affected, given its large dependence on its unit trust income.

As most banks are already well-buffered, expect only a few instances of large overlay allocations.

Asset quality should see some uptick in select segments. Banks have already revised NCC guidance in the previous quarter. We expect most to adhere to the renewed guidance.

Most have expressed contentment with the current level of loan loss coverage. Hence, we think instances of heavy provisions will be few.

Except for BIMB, none of the renewed guidance seems to deviate too far from NCC levels seen in previous years.

We are more optimistic on 2HCY25’s provisioning outlook, as recoveries related to a large oil and gas exposure should begin flooding then.

Asset quality should remain neutral for the most part, but we expect some banks to see some worsening in select segments.

The residential mortgages segment has been earmarked as a source of potential concern (ABMB, AFFIN; BIMB showed concerning gross impaired loan (GIL) uptick on this front last quarter, but is guiding for improvement).

Out of the banks under our coverage, RHB seems the most pessimistic, explicitly guiding for a GIL ratio worsening to accelerate in 2HCY25.

MBSB Research maintains their NEUTRAL call and identifies top downside risks such as economic slowdown which affects growth prospects and steeper-than-expected NIM compression. —Aug 11, 2025

Main image: The Star