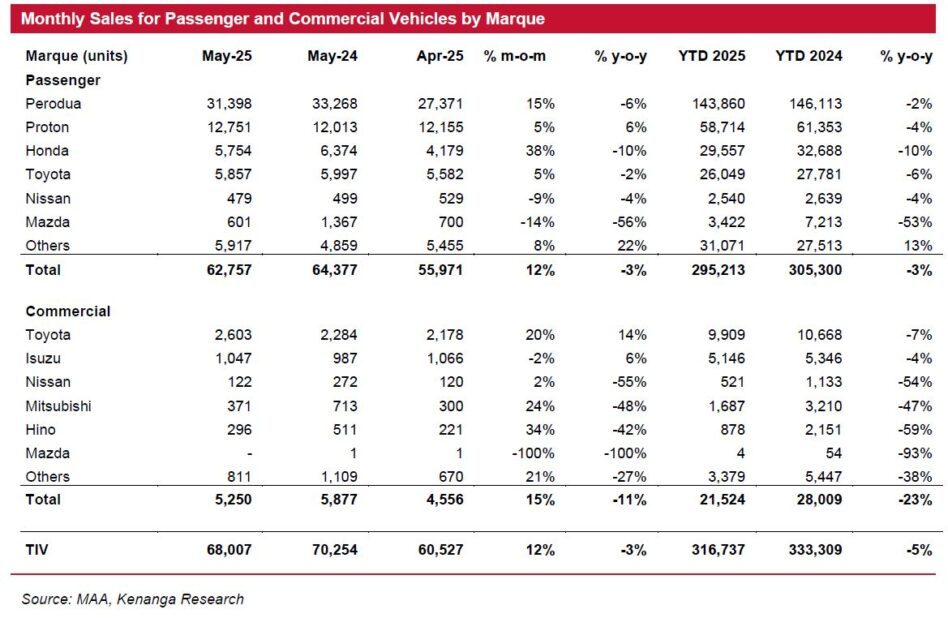

TOTAL industry volume soared 12% month-on-month (MoM) on longer working month in the absence of festivities dovetailing with substantial booking flows from Malaysian Autoshow 2025 held earlier in May 2025.

Meanwhile, TIV declined 3% year-on-year (YoY) mainly due to the shifting in new models launches toward the second half (2H) for this year by Perodua and other Japanese marques.

“Looking ahead, we believe June 2025 TIV will be weaker than May 2025 due to scheduled plant maintenance shutdown during the Hari Raya Aidiladha holidays,” said Kenanga Research (Kenanga).

National marques stood their ground, reaping market share from the non-nationals marques, backed by strong sustained demand in the affordable segment, attractive new launches, and a downtrading trend by mid-market buyers (in preparation for RON95 fuel subsidies rationalisation expected by the second half of 2025).

Within the non-nationals marques, Mazda suffered the most due to slower new launches and being affected by intense competition from Chinese marques.

“For the month of May 2025, BYD takes the position of 3rd place (7% of non-nationals TIV share) which was typically held by Mazda, and Chery fell to 4th place (4% of non-nationals TIV share) which we believe was due to the dilution of market share as more Chinese brands entered the market including Chery own sub-brand,” said Kenanga.

A two-speed automotive market locally will persist stretching to end-2025 and flowing into 2026.

It will be business as usual for the affordable segment as its target customers, the B40 and lower tier M40 groups, will be spared the impact of the impending RON95 subsidy rationalisation and could also potentially benefit from the introduction of the progressive wage model.

Government is still finalising the mechanism to use for the RON95 subsidy rationalisation and expects that 90% of the Malaysian will not be affected.

Initially, government looks to float the RON95 price to market rate for foreigners only, and then to the T15 tier group after finalising the income bracket range classification to improve income targeting scheme.

The upper-tier M40 and T15 groups may hold back from buying new cars, down-trade to smaller cars or switch to hybrids and EVs to cut their fuel bills upon the introduction of fuel subsidy rationalisation.

Concurrently, household bills will also be affected by the higher fuel bills, as well as expected 14% increase in base tariff for the higher-end usage which could also drive consumers to switch to solar-panels, in-turn boosting the demand for EV to funnel the excess grid electricity.

Additionally, EV routine maintenance costs are considerably lower than ICE’s due to fewer moving parts and wear & tear parts.

Vehicle sales will also be supported by new BEVs that enjoy SST exemption and other EV facilities incentives up until 2025 for complete build-up and 2027 for complete knockdown.

The new registration for BEVs leapt from 274 units in 2021 to over 3,400 units in 2022, 13,301 units in 2023, and 21,789 units in 2024, or 3% of TIV.

“We expect more favourable incentives from the government which has set a national target for EVs and hybrid vehicles of 20% of TIV by 2030 and 38% by 2040,” said Kenanga.

Meanwhile, the government will speed up the approval for charging stations. The number of proposed charging stations is currently at 4,299 (3,611 built to date) and this should more than double to 10,000 by the end of 2025. —June 20, 2025

Main image: The Manufacturer