TODAY, Nestlé Malaysia (NESTLE) stands as more than just a food manufacturer. It is a barometer of Malaysian consumer health: when Malaysians spend more, trade down, or tighten budgets, Nestlé’s earnings often tell part of that story.

Its future now hinges on familiar challenges—managing commodity costs, maintaining affordability, strengthening sustainability efforts, and staying relevant to increasingly value-conscious consumers.

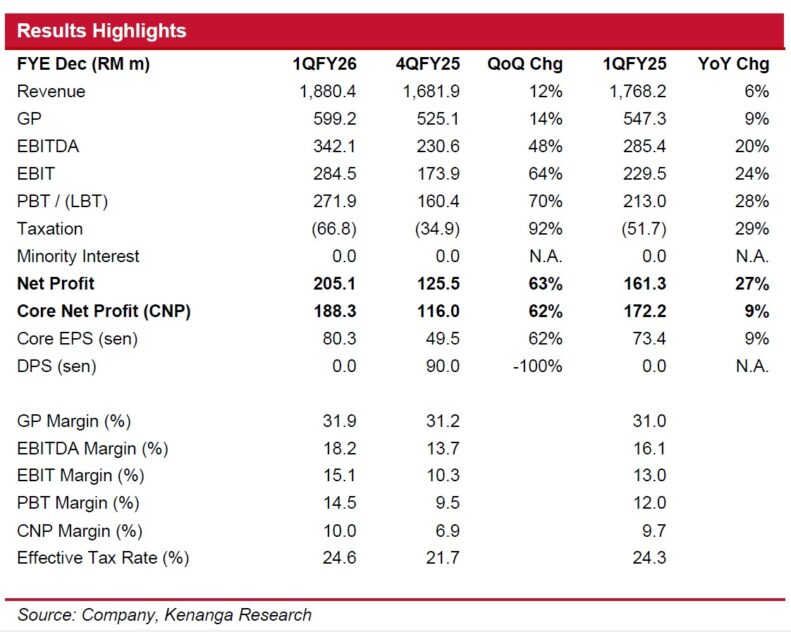

NESTLE’s quarter one financial year 2026 (1QFY26) core net profit of RM188 mil came in at 31% of both Kenanga’s full-year forecast and the street’s estimate.

1QFY26 revenue rose 6%, driven by resilient domestic demand, particularly during the festive season, as well as ongoing contribution from export markets.

“We believe this was partly supported by the RM100 one-off SARA cash aid disbursed in mid-Feb,” said Kenanga.

Core net profit grew 9%, likely driven by better economies of scale from higher sales volume.

1QFY26 revenue climbed 12% on broad-based contributions across its diversified portfolio, further boosted by seasonally stronger demand during Chinese New Year and Hari Raya.

The stronger top line translated into a 64% increase in earnings before interest and tax, with margins expanding 4.8 ppts quarter-on-quarter.

This was likely due to better cost control and scale efficiencies, with 1Q margins also seasonally higher. Consequently, core net profit surged 62% despite a higher effective tax rate.

“We see emerging cost pressures from the Middle East conflict, which could raise logistic and packaging costs, driven by higher fuel prices and resin supply tightness,” said Kenanga.

If sustained, potential further price pass-through may dampen demand as consumers down-trade to more affordable alternatives, though the RM100 one-off SARA cash aid should provide near-term support.

Meanwhile, easing commodity prices are expected to offer some relief.

Cocoa prices have declined significantly to near 2023 levels, while coffee bean prices are down 12% year-to-date but remain above historical averages.

Together with a stronger MYR, this should gradually ease input cost pressures.

However, the relatively modest year-on-year gross margin expansion in 1QFY26 suggests lingering higher-cost inventory and hedging lags.

“Overall, we expect a gradual margin recovery this year, supported by improving operational efficiencies on higher sales volumes,” said Kenanga.

While sales are now largely back to pre-boycott levels, this has been partly driven by prior price hikes amid elevated commodity costs, and Kenanga believe margins are likely to remain below 2023 levels in the near term amid renewed cost pressures.

Kenanga likes NESTLE for its strong brand and diversified product range, and the inelasticity in the demand for staple food products. However, despite ongoing margin recovery, uncertainty remains around the sustainability of current margin levels.

“We believe valuations are fair at current levels. Reiterate Market Perform,” said Kenanga. —Apr 29, 2026

Main image: stock.adobe.com