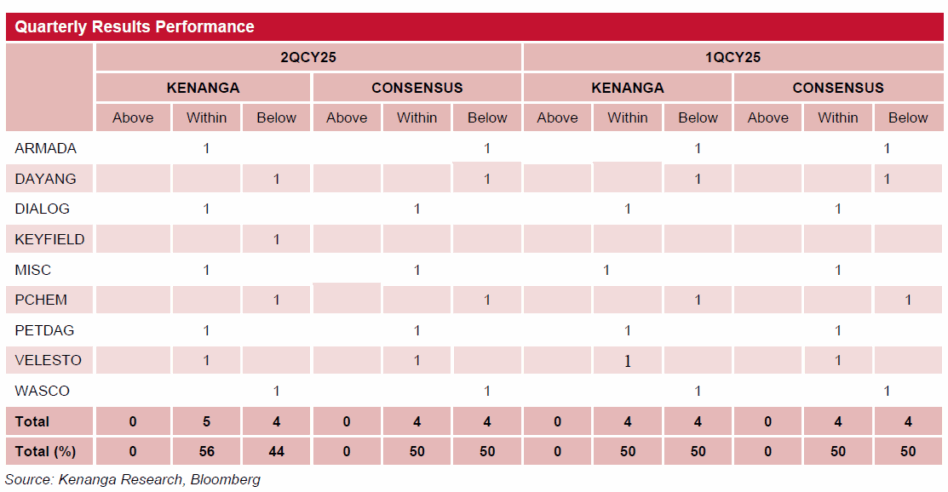

IN THE quarter, there was no outperformance of earnings within the oil and gas sector, which was the second consecutive quarter from last quarter.

“This indicates that earnings seem to have peaked for the majority of our coverage since financial year 2024 (FY24), which was an extremely outstanding year especially for upstream service providers,” said Kenanga.

In quarter two financial year 2025 (2QFY25), upstream service providers partially disappointed with DAYANG and WASCO reported weaker-than-expected earnings due to weakening work orders and OSV utilisations and pipe coating work orders, respectively.

PCHEM continued to miss as its specialty chemical division continued to underperform due to sthe stiff competition from China while its F&M and O&D business continued to post lower earnings due to tepid product prices.

The safe haven from the earnings perspective remains at the bigger caps with mid-stream exposure with names like DIALOG , MISC and PETDAG delivering within expectation results.

FY25F earnings outlook seems to be weaker year-on-year (YoY) for the upstream service providers, and it seems to imply that earnings for the subsector as a whole is coming off a cycle peak in FY24 and we could not discount the possibility of further YoY weakness in FY26.

Nevertheless, from our meetings with the companies, we still get the general sense that both FY25 and FY26 will more than likely to be still profitable for upstream service providers.

Hence, the share price impact to the service providers in the coming quarters if earnings underperform might be more manageable compared to previous downcycles. In downstream, however, the picture is gradually changing as PCHEM appears to be reaching bottom-earnings for the cycle in FY25.

Across the board, down-stream product prices still remained tepid and do not appear to be worsening further, a sign of finding a bottom at least.

That aside, there are already early optimisms on capacity rationalisations in the polyolefins segment as Korea and China are reportedly looking to reduce capacities, particularly the ones that are ageing and inefficient.

In our view, while 2HFY25F earnings outlook remain tepid, investors appear to have already looked beyond that and are looking forward to a potential recovery in FY26 as capacity cuts (or in China capacity addition slowdown) might trigger at least a short-term up-cycle in polyolefin prices for a year.

Hence, we advise investors to keep a keen eye on this space to watch out for news on petrochemical facilities in the coming months and ascertain whether the capacity plans follow through or not.

We believe that the two-pronged strategy of staying in defensive midstream stocks and taking more risks in downstream names appears to be the best bet for investors at least in the short to medium-term.

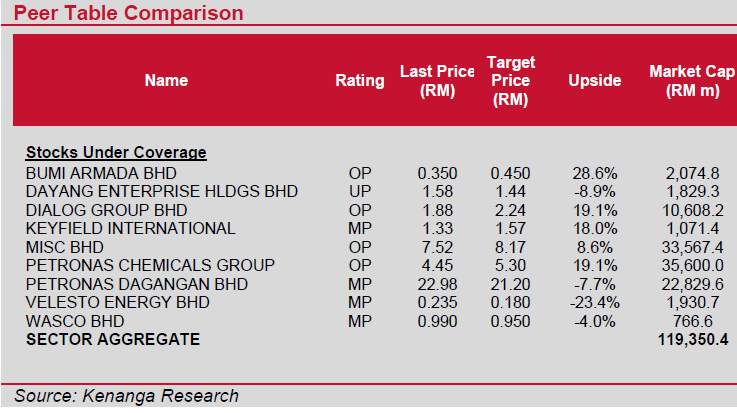

While upstream service providers’ share prices have come off significantly (50% off the peak), we believe that it is prudent to wait for the earnings down-cycle to play out a bit more in the coming quarters before going for the buy the dip strategy.

On the local front, Petronas capex remains uncertain for FY26 given the lack of details on the gas aggregation profit sharing details with PETROS, thereby hindering upstream capex in East Malaysia.

Therefore, we believe a better time to relook the sector is during early 2026 as by then it would be likely that most of the negative outlook on FY26 earnings are already priced in.

Partially offsetting the downside is the potential for upstream service providers to ramp up their dividend payouts due to their net cash balance sheets. —Sept 19, 2025

Main image: CxPlanner