BRENT crude has strengthened materially over the past 1–2 months in 2026, rebounding from the low-US$60s in early January to the low-US$70s by late February.

“The move has been predominantly risk-premium driven rather than fundamentals-led. Physical balances remain relatively manageable, but escalating geopolitical tensions in the Middle East have reintroduced uncertainty into near-term supply expectations,” said TA Securities.

Tensions intensified on 28 February following coordinated strikes by the US and Israel on Iran, prompting retaliatory missile and drone responses across the region.

The developments have heightened market sensitivity to potential disruptions involving Iranian exports and, more critically, the security of transit chokepoints such as the Strait of Hormuz.

“As roughly one-fifth of global oil consumption transits through Hormuz, even marginal disruption risk commands a meaningful pricing response,” said TA.

At this stage, price action appears largely headline-driven, with volatility reflective of uncertainty around escalation trajectory rather than confirmed physical supply losses.

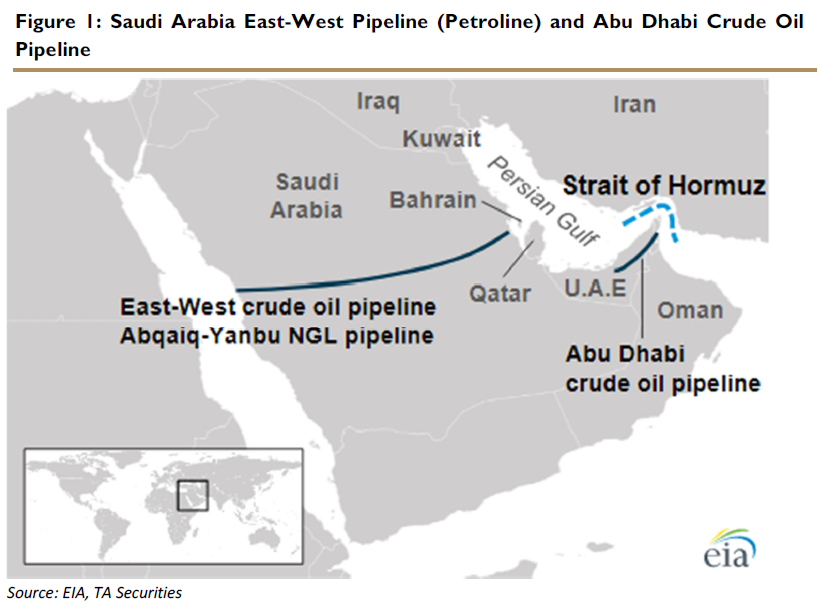

The Strait of Hormuz remains the single most critical maritime chokepoint in the global energy System. Critically, bypass capacity is insufficient to fully offset Hormuz flows.

Saudi Arabia’s East-West Pipeline (Petroline), which runs from Abqaiq to Yanbu on the Red Sea, has a nameplate capacity of ~5 mb/d.

However, practical operational throughput is typically closer to 2–3 mb/d, depending on utilisation and logistics constraints. The UAE’s Habshan–Fujairah pipeline provides an additional ~1.5–1.8 mb/d of bypass capacity.

Combined realistic relief capacity is therefore estimated at ~3–5 mb/d under optimised conditions, versus ~19–20 mb/d normally transiting Hormuz.

This implies that over 70% of typical Hormuz flows would lack viable alternative routing in a major disruption scenario, underscoring why the market embeds a disproportionate risk premium when tensions escalate.

Under a contained escalation scenario, similar to previous US–Iran exchanges, TA would expect heightened volatility without sustained physical supply loss. Tanker insurance premiums rise, freight rates firm, and front-month time spreads tighten modestly.

However, as long as Hormuz transit remains operational and export infrastructure is not materially damaged, effective supply loss remains minimal. In this case, the geopolitical premium gradually fades as tensions deescalate.

Brent would likely retrace toward our structural forecast range of USD50–70/bbl, reflecting a market that remains fundamentally adequately supplied.

“We remain Underweight on the sector, as we expect recent Brent strength to prove largely risk-premium driven and susceptible to normalisation should geopolitical tensions de-escalate,” said TA.

Absent confirmed and sustained physical supply disruption, TA see Brent reverting towards their structural range of US$50–70/bbl, reflecting manageable global balances and sufficient spare capacity buffers.

“In this environment, we favour companies with more resilient earnings profiles and lower sensitivity to oil price volatility,” said TA. —Mar 3, 2025

Main image: Twenty Two