Kenanga trimmed their 2025 Brent crude forecast to USD77/bbl (from USD80/bbl previously) and introduce a 2026 forecast of USD74/bbl, slightly above the US Energy Information Administration’s (EIA) estimates (2025: USD74/bbl) as we factored in a weaker demand outlook in 2025 especially in 1H25.

Our relatively more optimistic view compared to the consensus stems from the belief that the market has largely priced in a crude production surplus for 2025, while demand growth assumptions remain overly conservative.

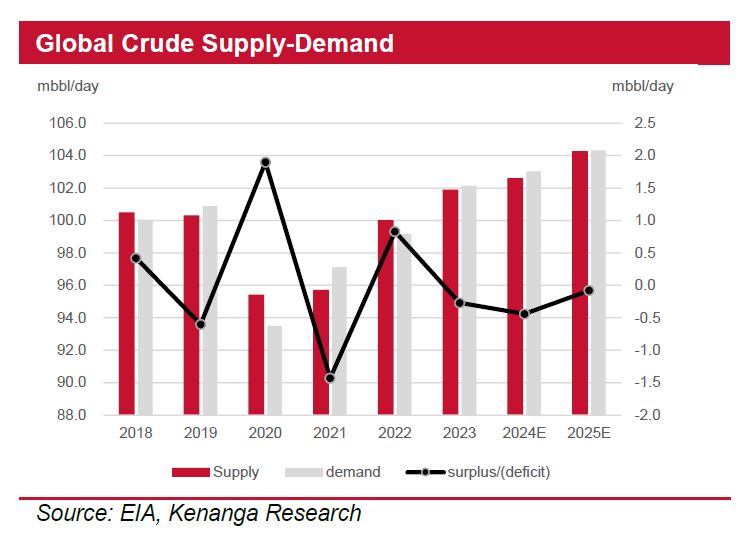

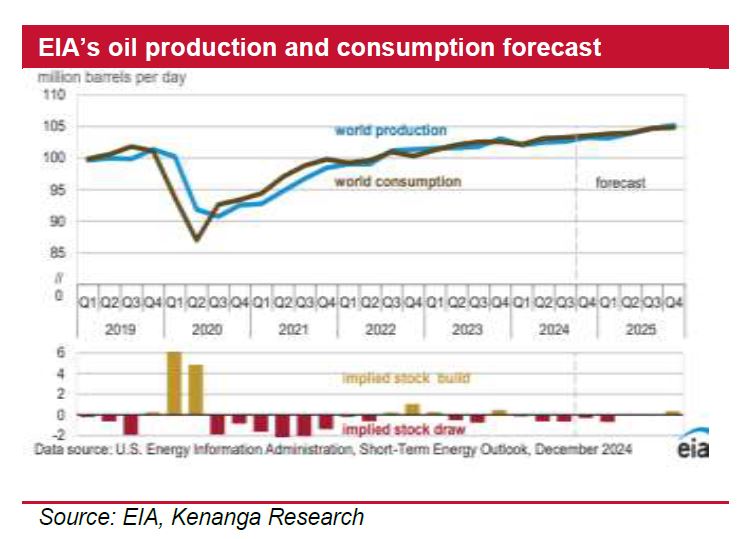

The EIA’s December 2025 report forecasts global oil consumption to grow by 1.3m bbls/day, below the pre-pandemic 10-year average of 1.5m bbls/day and slower than the recovery pace in 2021–2023.

With Europe and China expected to adopt financial easing measures in 2025, we see potential for positive surprises in crude demand growth.

We maintain our 2025 Brent crude forecast at USD80/bbl and introduce a 2026 forecast of USD74/bbl, slightly above the US Energy Information Administration’s (EIA) estimates (2025: USD74/bbl).

We maintain our 2025 Brent crude forecast at USD80/bbl and introduce a 2026 forecast of USD74/bbl, slightly above the US Energy Information Administration’s (EIA) estimates (2025: USD74/bbl).

Our relatively more optimistic view stems from the belief that the market has largely priced in a crude production surplus for 2025, while demand growth assumptions remain overly conservative.

The EIA’s December 2025 report forecasts global oil consumption to grow by 1.3m bbls/day, below the pre-pandemic 10-year average of 1.5m bbls/day and slower than the recovery pace in 2021–2023.

With Europe and China expected to adopt financial easing measures in 2025, we see potential for positive surprises in crude demand growth.

China and Europe accounts for c.25% of total crude demand hence any 1% upside to demand from the two regions could provide c. 0.25% increase in world demand.

According to The Star, discussions on gas distribution in Sarawak between Petronas and PETROS have concluded, with the government now refining the agreement’s details and implications.

We estimate that any potential capex cut by Petronas due to this agreement would not exceed RM10b annually, a modest reduction from its projected RM60b per year.

We believe that the calculation is justified, considering that Sarawak must still pay for the LNG infrastructure previously developed by Petronas, including LNG trains and liquefaction plants.

Additionally, we believe it is in the mutual interest of PETROS and Petronas to eventually ramp up upstream investments to maximise their long-term revenue potential.

According to Fitch Solutions, Southeast Asia’s national oil companies (NOCs) are projected to increase their combined capex by 29% YoY to USD31b in 2025, driven by 58 greenfield projects and 22 field expansions.

According to Reuters, PTTEP plans to allocate USD5b in 2025 as part of its USD21.2b five-year plan, focusing on key assets and overseas projects, with the Lang Lebah gas field in Sarawak’s SK410B block expected to reach a final investment decision.

Petrovietnam targets double-digit growth, implying higher capex, while Indonesia’s Pertamina aims to increase oil and gas output by 4-5% YoY, signalling sustained investment momentum.

Overall, regional NOCs remain in capex expansion mode, and once PETROS’ gas agreement details are finalised, Petronas could ramp up its spending by 2H25.

In recent months, Pan-Malaysia contracts have finally been awarded after years of one-year extensions, offering a more predictable long-term outlook for upstream maintenance players.

According to The Edge Malaysia, the Pan-Malaysia umbrella contract is valued at up to RM10b over 10 years, though we believe the total value could exceed this if Shell’s packages are included.

For instance, DAYANG (OP; TP: RM3.80) secured two packages from Petronas worth RM3b over five years for the firm period and an additional package from Shell potentially valued at RM1b over five years.

Other players like T7, Sapura Energy, and Carimin have also been awarded packages under this structure. As a result, we expect upstream maintenance activities to sustain growth into 2025.

The domestic upstream service players are witnessing a robust pick-up in demand from Petronas and other oil producers. Short -term daily charter rates (DCR) for accommodation work boats (AWB) have surged to RM150,000/day for charters of three months or less, surpassing the 2013–2014 bull market levels.

However, mid-sized anchor handling tug supply (AHTS) vessels (~5000 bhp) are transacting at RM40,000/day or below, still shy of their previous peak of RM47,000/day, reflecting continued demand for brownfield maintenance jobs over greenfield projects.

From a risk-reward perspective, we recommend focusing on maintenance-driven OSV players like KEYFIELD (OP; TP: RM3.18), which stand to benefit from immediate DCR hikes. Greenfield-driven OSVs (e.g., AHTS) could see improvement in 2H25 as the PETROS-Petronas overhang diminishes with the finalisation of the gas agreement. —Jan 10, 2025

Main image: etrosync