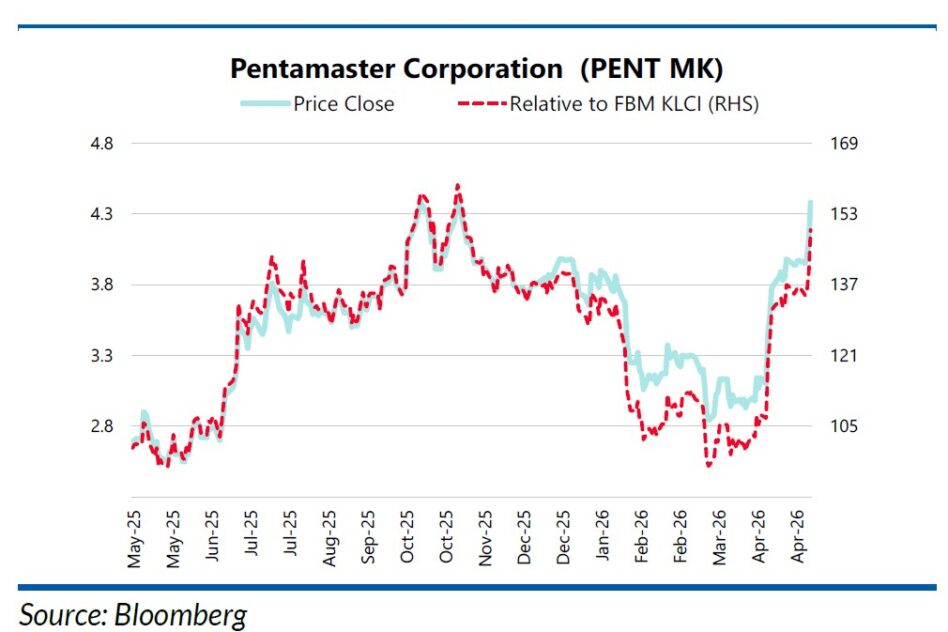

PENTAMASTER CORP posted a strong start to 2026, with its first-quarter core profit after tax, amortisation and minority interests rising 46.7% year-on-year, broadly meeting market expectations.

The performance was largely driven by robust expansion in its factory automation solutions (FAS) division.

The company’s outlook for financial year 2026 remains positive, underpinned by a healthy order book worth RM480 mil.

Growth momentum is expected to continue on the back of sustained demand in the FAS segment, alongside a gradual rebound in the automated test equipment (ATE) business as the global semiconductor capital expenditure cycle gains traction.

“We continue to like the stock for the intensified semiconductor capex cycle and pivot to advanced packaging and artificial intelligence (AI)-driven automation solutions,” said RHB.

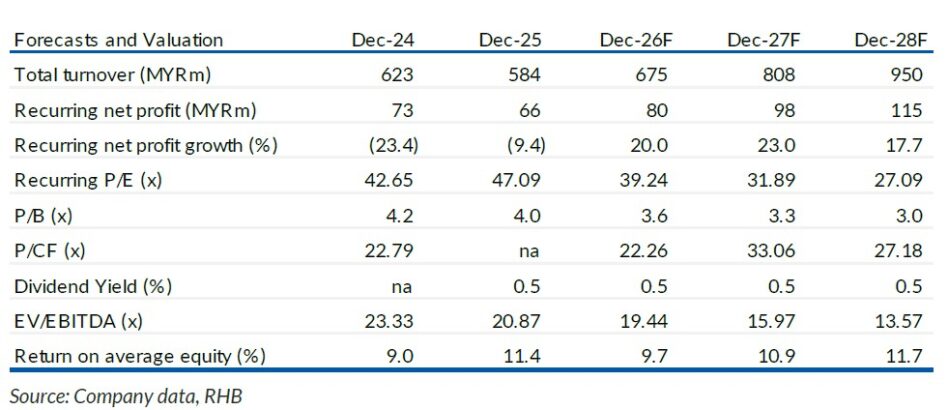

1Q26 revenue of MYR180.4 mil (+37.1% YoY) and core PATAMI of MYR15.8 mil came in at 20% and 19% of RHB and Street’s estimates.

RHB deems the results as in line given expectations of better quarters ahead.

“Robust showing from FAS was contributed by electro-optical and medical customers, and a low base effect. This more than offset a 9% drop in ATE amid lower sales from both automotive and electro-optical related applications,” said RHB.

Earnings before interest, tax, depreciation and amortisation margins, however, were affected by product mix as the test handler for semiconductor segment is of lower margins and further weighed down by higher costs from the healthcare segment, which reported LBT of 9.2 mil vs 5.7 mil in 1Q25.

Sequentially, core PATAMI was lower by 26.8%, given that 4Q25 profitability was further boosted by non-recurring income from project cancellation charges of MYR12 mil – otherwise, it would have increased by 21% QoQ.

Pentamaster Corp’s outstanding orderbook comprises medical (55%), consumer/industrial (24%), electro-optical (5.5%), automotive (10.5%), and semiconductor (5%) segments.

Management expects FAS to continue benefiting from stronger project pipelines from smartphone assembly and testing applications, automation solutions for server and data centre infrastructure, and medical manufacturing and assembly processes.

For ATE, stronger demand is seen for silicon carbide or SiC front-end wafer burn-in solutions, smart sensor test solutions, and test handlers’ equipment amid a positive outlook for semiconductors, particularly in AI and high-performance computing or HPC applications.

New advanced packaging test solutions roadmap under the 9 Samurai initiative are expected to be the next growth wave into 2027. —May 8, 2026

Main image: Dagang News