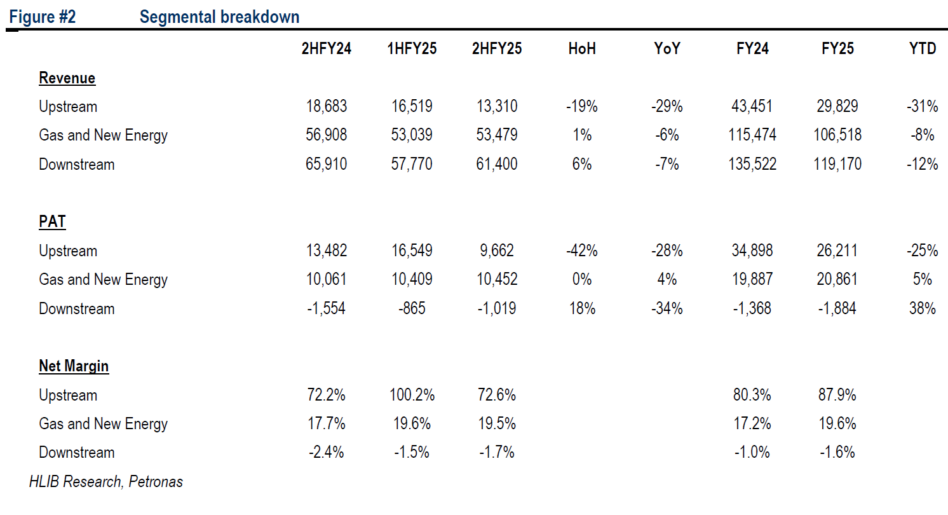

PETRONAS reported second half of 2025 (2H25) core earnings of RM19.3 bil. The weaker set of performance was primarily due to lower revenue contribution across all three core segments, including Upstream, Gas & New Energy and Downstream segments.

“Revenue remained largely stable, inching up by +1%, supported by stronger contributions from the Downstream segment (+6.3%) on the back of higher sales volumes in petroleum and petrochemical products,” said Hong Leong Investment Bank (HLIB).

However, this was partially offset by weaker Upstream revenue (-19%), due to lower average realised prices and sales volumes.

Meanwhile, the Gas segment was broadly flat (+0.8%), with improved LNG sales volumes delivered in Peninsular Malaysia.

However, core earnings fell -20%, mainly due to higher operating expenses, finance costs and lower contribution from share of JV and associates.

Financial year 2025 (FY25) capital expenditure (capex) fell by 23% year-on-year (YoY) to RM41.6 bil, as the Group recalibrates spending following the peak investment cycle seen previously.

This moderation is in line with Petronas’ focus on optimising capital allocation and pacing project execution amid a softer oil price environment and evolving energy transition priorities.

“Notably, spending remains anchored towards core upstream developments, including investments in the Kasawari Gas Field and oil field development in Angola,” said HLIB.

Petronas’ FY25 results reflect a phase of cyclical normalisation rather than structural deterioration in fundamentals, in HLIB’s view.

The softer earnings were largely driven by weaker realised prices and margin pressures across core segments, while the continued losses in Downstream underscoring the persistent challenges in refining and petrochemical spreads.

The reduction in capex signals a more disciplined investment stance amid a softer oil price environment, with net cash improving by +7% to RM82.8 bil in FY25.

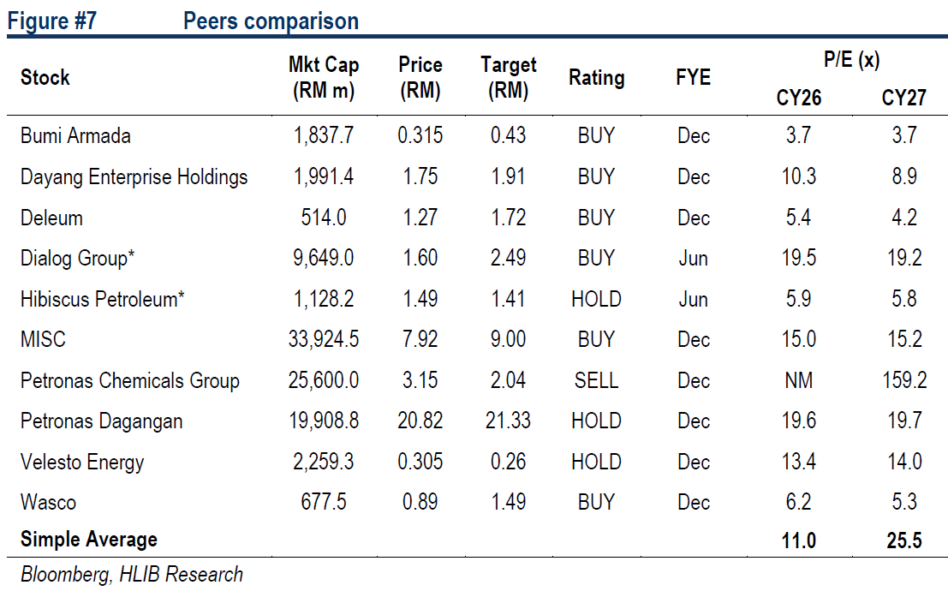

“We maintain our Overweight rating on the sector with most of the names under our coverage hovering at attractive undemanding valuations including Wasco, Armada, Dayang, and Deleum,” said HLIB. —Mar 2, 2026

Main image: Organo