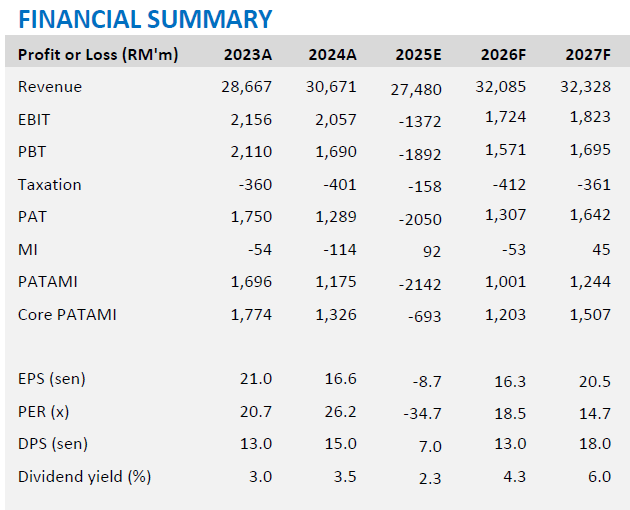

PETRONAS Chemicals Group Bhd’s (PCG) financial year 2025 (FY25) loss came in significantly below ours and consensus expectations.

“As such, we maintain NEUTRAL for PCG with an unchanged target price of RM3.01,” said MBSB Research.

FY25 revenue declined by 10% year-on-year (yoy) amid weaker prices and foreign exchange headwinds.

PCG recorded FY25 revenue of RM27.5 bil, supported by relatively steady sales volumes across its commodity and specialty chemicals portfolios.

“However, this marked a year-on-year decline, mainly due to softer average product prices, narrowing spreads, and persistent global oversupply, particularly within the Olefins & Derivatives and Specialties segments,” said MBSB.

The revenue performance was further weighed down by the strengthening of the Ringgit against the US dollar, which negatively impacted export earnings.

Operationally, plant utilisation averaged 88% in FY25, affected by a combination of unplanned disruption, notably a utilities outage at the Kertih Integrated Petrochemical Complex and feedstock supply disruption at PC Fertiliser Kedah.

While production volumes were largely maintained, these factors, together with weaker pricing conditions, resulted in lower overall revenue compared to FY24.

Losses after tax, amortisation and minority interest for FY25 was -RM2.1 bil a significant deterioration from FY24 profit after tax, amortisation and minority interest of RM1.1 bil, reflecting the sharp contraction in margins amid weaker product spreads and persistent market oversupply.

The earnings decline was further exacerbated by asset impairments at Perstorp, as well as unfavourable foreign exchange movements, including unrealised forex losses arising from the revaluation of shareholder loans and payables.

PCG’s FY25 performance was a testament to its close ties to the global economic conditions. Certain petrochemical companies had been plagued with oversupply and demand uncertainty, painting a continuously challenging environment for the group.

Nevertheless, PCG had remained focused on maintaining its high plant utilization rate to mitigate the external pressures and continues to engage with its clients to ensure a consistent supply of products and services.

“We believe PCG will continue to lean on its operational efficiency to weather the challenges of soft prices and demand uncertainties,” said MBSB.

PCG’s FY25 performance underscored the difficult operating environment for the global chemicals industry, marked by persistent oversupply, subdued downstream demand and weaker product spreads.

Group earnings were dragged into losses, primarily due to the Olefins & Derivatives and Specialty Chemicals segments, which were weighed down by pricing pressure, forex losses and asset impairments.

In contrast, the Fertiliser & Methanol segment remained resilient, supported by stable agricultural demand.

Looking ahead into FY26, the operating landscape is expected to remain challenging, as new capacity additions in China continue to pressure the market, while demand recovery remains uneven across key end markets. —Feb 24, 2025

Main image: OneTiger