THE LATEST quarterly earnings season produced a mixed bag of results for plantation companies, with four of the seven firms reporting performance broadly in line with expectations. GENP, JPG and TSH, however, fell short of forecasts.

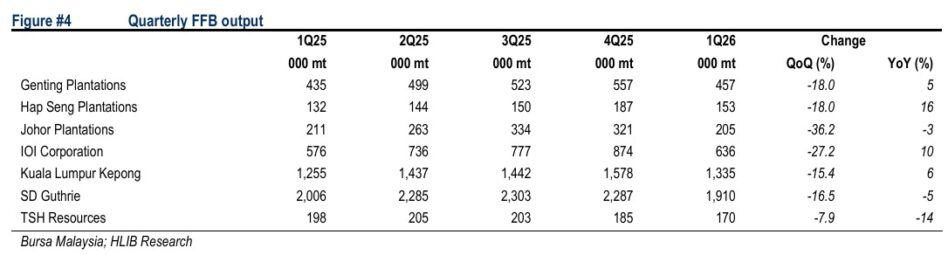

The weaker results at GENP and TSH were mainly driven by lower-than-expected FFB production.

For JPG, earnings were affected by softer realised price premiums, largely due to higher inventory levels and increased procurement of external crop.

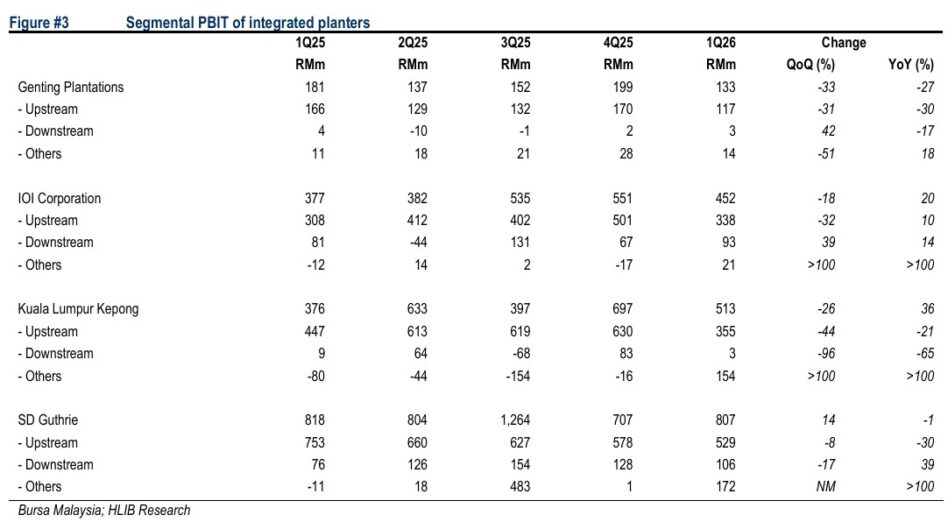

Aggregate core earnings fell -16% quarter-on-quarter (QoQ) to RM1.25 bil in quarter one 2026 (1Q26), dragged mainly by seasonally lower cropping activities and softer realised palm product prices.

Although feedstock costs eased during the quarter, downstream operations delivered mixed results across the sector.

GENP and IOI registered quarter-on-quarter improvements in downstream earnings, while KLK and SDG experienced softer performances.

According to Hong Leong Investment Bank (HLIB), the divergence reflects differing demand trends across product segments and regional markets, with some businesses benefiting from stronger market conditions while others faced weaker consumption patterns.

Aggregate core earnings fell -11% to RM1.25 bil, dragged mainly by lower realised palm product prices.

During the quarter, five out of seven planters registered positive fresh fruit bunch (FFB) output growth, supported by overall favourable weather conditions and improved labour supply.

Meanwhile, JPG and TSH saw declines in their FFB output, due mainly to less favourable weather conditions in Johor (arising from dry weather) and Sumatera (due to severe flooding).

Downstream performances were mixed. With IOI and SDG recording improved YoY downstream contributions, while KLK experienced a decline.

The differing performance trends were likely attributable to varying hedging positions and currency translation effects within the refinery sub-segment, as well as differing demand conditions across product categories and geographical markets.

Most planters maintained their earlier FFB output guidance, as management generally believes that the emerging El Nino phenomenon is unlikely to materially impact near-term productivity.

During the quarter, several planters highlighted mounting cost pressures stemming from the geopolitical conflict in the Middle East, particularly due to concerns over fertiliser supply disruptions and rising freight and energy costs.

If prolonged, these developments could place upward pressure on CPO production costs.

While the overall operating environment remains challenging amid persistent industry overcapacity, integrated planters appear to have turned slightly less bearish on the segment’s near-term prospects.

This is driven by heightened price volatility, lower feedstock costs (particularly PK), and more active restocking activities by certain customers within the oleochemical sub-segment, partly due to supply chain concerns arising from the Middle East conflict.

“We maintain our Overweight stance on the sector, supported by near-term CPO price strength driven by elevated crude oil prices,” said HLIB.

However, the research house warns that the current upcycle is likely to be front-loaded, with medium-term risks arising from supply-side adjustments in competing vegetable oils.

For targeted exposure, HLIB advocates purer upstream planters that have already locked in their fertiliser cost for the year, which provides greater margin visibility, such as JPG and SDG. —June 5, 2026

Main image: plantationsinternational.com