ACCORDING to the latest NAPIC first half of 2025 (1H25) data, Malaysia’s property market recorded 196,232 transactions worth RM107.7 bil, reflecting a 1.3% decline in volume but a 1.9% increase in value compared with 1H24.

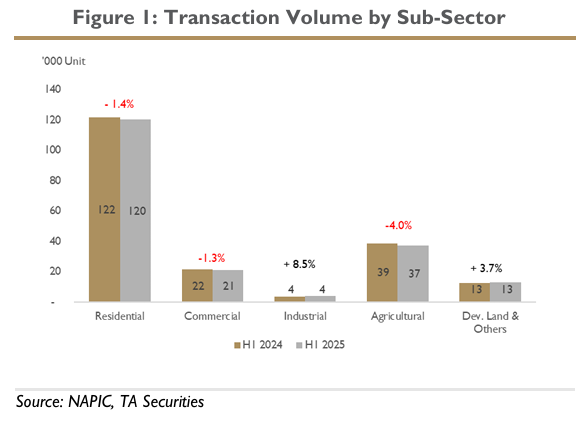

Market activity was mixed across segments: commercial and agricultural volume contracted by 1.3% and 4.0%, while industrial and development land transactions grew by 8.5% and 3.7%.

In value terms, commercial, industrial, and development land rose 3.1%, 5.6%, and 18.3% respectively, while agriculture fell sharply by 11.3%.

Within the residential segment, which accounts for the bulk of market activity, transactions slipped 1.4% year-on-year (YoY) in volume and edged down 0.1% in value.

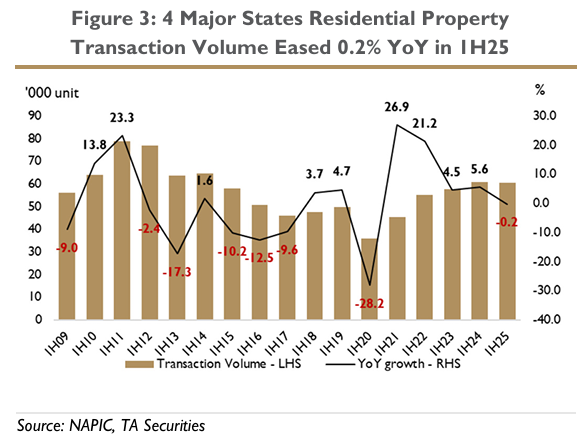

The four major states, namely Kuala Lumpur, Johor, Selangor, and Penang, which collectively account for around half of national transactions, also posted only slight contractions of 0.2% in volume and 0.1% in value compared with 1H24.

“We observe that the moderation is relatively mild in historical context. Residential activity remains well above post-pandemic lows, and the slight pullback mainly reflects a high-base effect after several years of strong growth,” said TA Securities.

Given ongoing local policy adjustments and external uncertainties, some cooling in transaction momentum is not unexpected.

By state, Johor stands out as a bright spot, with residential transaction volumes and values holding up better than peers. We attribute this resilience to spillover optimism from the Johor–Singapore Special Economic Zone (JS-SEZ) and ongoing infrastructure projects such as the RTS Link.

This reinforces our view that Johor will remain a structural growth driver for the sector, particularly for developers with strategic landbank exposure in Iskandar Malaysia.

The overhang of homes worsened in 1H25, with the number of completed-but-unsold residences rising 16.3% in volume to 26,911 units and 17.9% in value to RM16.4 bil from end-2024. While this marks a reversal after several quarters of decline, we do not view the increase as alarming.

Comparisons with the 2021 peak (36,900 units worth RM22.8 bil) are less meaningful, as market activity during that period was distorted by the pandemic standstill.

Instead, benchmarking against the 2018 2019 levels, when overhang volumes already exceeded 30,000 units, provides more realistic context, as today’s levels remain below pre-pandemic highs.

Crucially, the previous surge in overhang was the lagged outcome of the supply spike in 2012–2015. Since then, developers have become more disciplined, with incoming residential supply trending well below historical peaks over the past decade.

This discipline suggests that the current uptick is unlikely to snowball into a structural oversupply cycle, as the pipeline of new completions is much smaller than in past cycles.

Overall, we note the NAPIC data as evidence of healthy consolidation rather than structural slowdown. Residential demand remains intact in affordable and landed segments, while absorption has slowed in higher priced projects.

Importantly, developers’ disciplined approach to new supply lowers the risk of another prolonged oversupply cycle. —Sept 9, 2025

Main image: Construction21.org