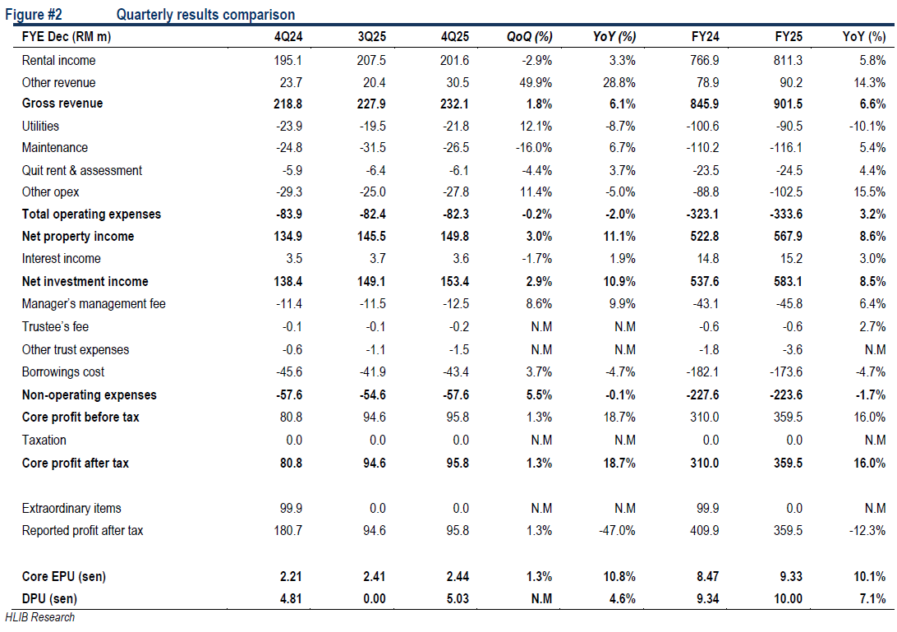

PAVILION REIT reported quarter four 2025 (4Q25) core net profit of RM95.8 mil (+18.7%) year-on-year (YoY), which brought 2025 earnings to RM359.5 mil (+16.0% YoY).

“The results were within ours and consensus expectations at 98% and 100% respectively,” said Hong Leong Investment Bank (HLIB).

Revenue was relatively flattish (+1.8%), while NPI expanded faster at +3.3%.

This was supported by lower operating expenses (-0.2%), mainly from reduced maintenance expenses (-16.0%). However, core profit grew only +1.3%, weighed down by higher manager’s fees (+8.6%) and borrowing costs (+3.7%).

Top line rose +6.1%, driven by stronger contributions from Pavilion Bukit Jalil (PBJ) (+7%) as well as contributions from the newly injected hotels. Meanwhile, core profit expanded +18.7%, supported by lower financing costs (-4.7%).

Retail occupancy improved to 97%, whereas Pavilion Tower’s office occupancy dipped slightly to 78%. Meanwhile, gearing eased to 40%.

HLIB expecta Pavilion Kuala Lumpur (PKL) and Elite Pavilion to continue enjoying robust footfall into 2026, underpinned by (i) Visit Malaysia 2026 initiatives and (ii) the mutual visa exemption between Malaysia and China. Earnings visibility will be further strengthened by the full-year contribution from the injection of Banyan Tree Kuala Lumpur (BTKL) and Pavilion Hotel Kuala Lumpur (PHKL), which are expected to provide a combined fixed RM33.5m in base rental (3.4% of our FY26f revenue).

“Coupled with mid-single-digit rental reversions, we expect Pavilion REIT to deliver improving earnings performance in 2026,” said HLIB.

HLIB maintains Buy with unchanged target price of RM2.02, based on an unchanged target yield of 5.2%, anchored to the five year historical average spread between Pavilion REIT and the 10-year MGS. —Jan 30, 2025

Main image: Ringgit