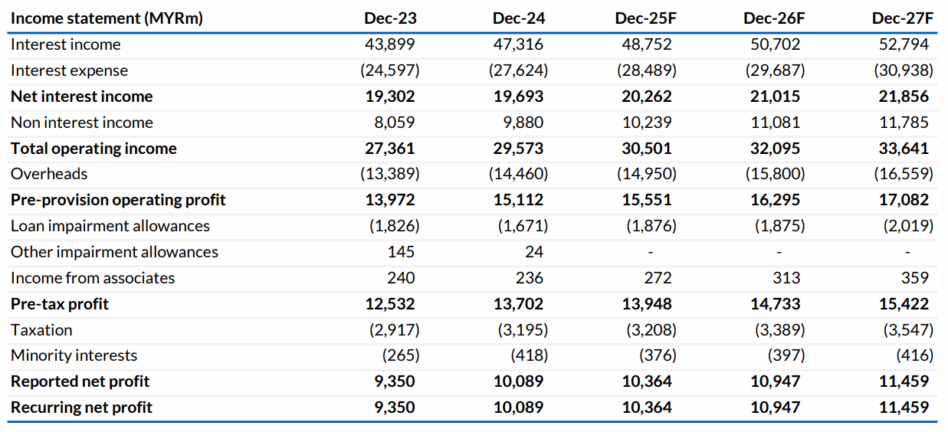

MALAYAN Banking’s quarter three 2025 (3Q25) results are in line, according to RHB.

Net interest margin (NIM), surprisingly, expanded quarter-on-quarter (QoQ) as liability management efforts helped offset the impact of lower policy rates regionally.

Looking ahead, MAY’s healthy corporate loan and IB pipelines should contribute positively to its operating income, while ongoing liability management and deposit repricing efforts should continue to help support a rebound in NIM.

“Stay BUY on attractive dividend yields,” said RHB.

Despite lower policy and benchmark rates across its home markets, 3Q25 NIM ticked up 2bps QoQ.

MAY attributed this to proactive liability management where it:

i) Shed higher-cost money market deposits and turned to cheaper-term money in Malaysia.

ii) Raised the loan-to-deposit ratio (LDR) in Singapore to 85% from 79% in 2Q25.

iii) Released high-cost CASA in Indonesia.

Also, CASA growth was a robust 4% QoQ and helped replace the costlier deposits. Hence, CASA ratio rose to 40% in 3Q25 from 38% in 2Q25.

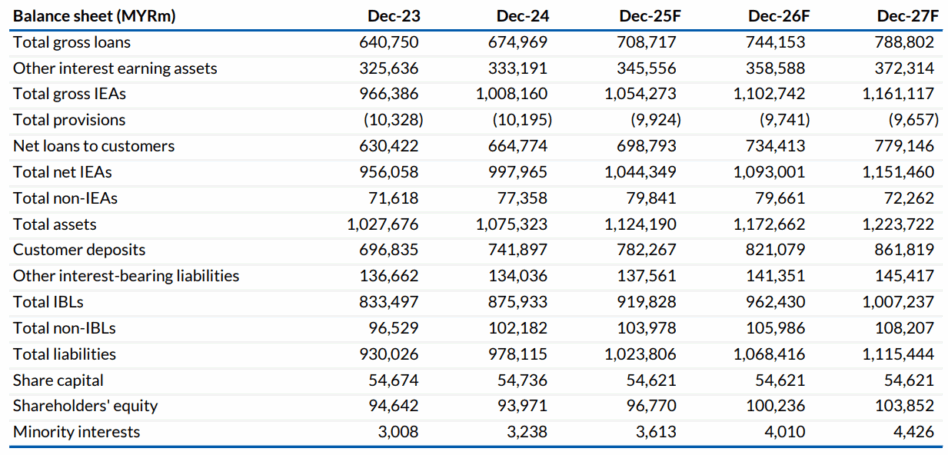

Annualised loan and deposit growth was +1% and flat while group LDR was 92%. Gross impaired loan ticked up 2% QoQ mainly due to a judgemental downgrade of a domestic corporate borrower from construction.

That said, there was a net writeback in loan expected credit loss (ECL) due to better recoveries from non-retail and the completion of an oil & gas borrower’s restructuring case.

Non-loan ECL, though, rose QoQ as post completion of restructuring, MAY’s entire exposure is now classified under investments (mixture of loans and investments previously).

Reported LLC was 110% due to the transfer of provisions to securities from loans, and new impaired corporate borrower but MAY was comfortable with the level, pointing to its management overlay of MYR2.5 bil.

Domestic deposit repricing is expected to continue for another 3-4 months and would be positive for NIM, partly offset by the seasonal deposit competition.

Looking ahead, its corporate loan and IB pipelines are strong, and MAY thinks it is a matter of timing for the drawdowns and deals to be executed. It expects domestic corporate loans growth to pick up in 4Q25, and accelerate further in 2026. —Nov 24, 2025

Main image: New Straits Times