RHB upgrades their banking sector call to Overweight from Neutral, following their recent upgrade of Public Bank (PBK). While near-term earnings may not excite, banks are heading into 2026 on fundamentally sound footing with attractive dividend yields.

Corporate banks would benefit from strong loan pipelines while asset quality should hold up. Meanwhile, banks under the Standardised Approach are set to adopt new capital guidelines next year, which could pave the way for capital management initiatives.

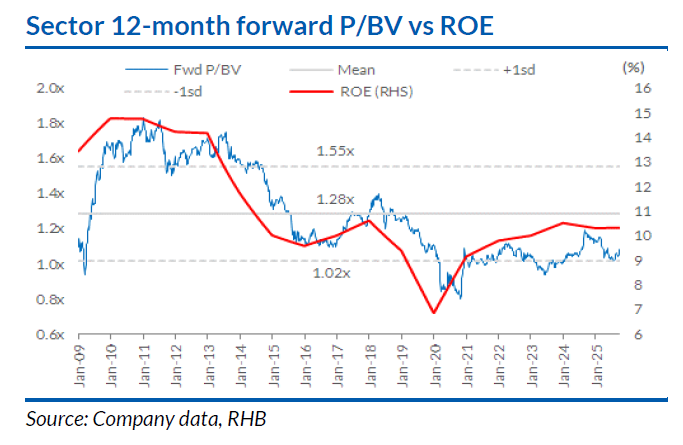

“Fundamentally, we think the sector remains sound. The domestic economy is expected to remain resilient, supporting our projection for 2026 sector profit after tax and minority interest (PATMI) growth to pick up as net interest margin (NIM) pressure eases, leading to stronger net interest income (NII) growth,” said RHB.

We would watch out for banks’ ongoing efforts to reduce funding cost and the repricing of deposits, given the sharp drop in policy and benchmark rates regionally.

A low interest rate environment could also be positive for loan demand, CASA growth, wealth management, and asset quality.

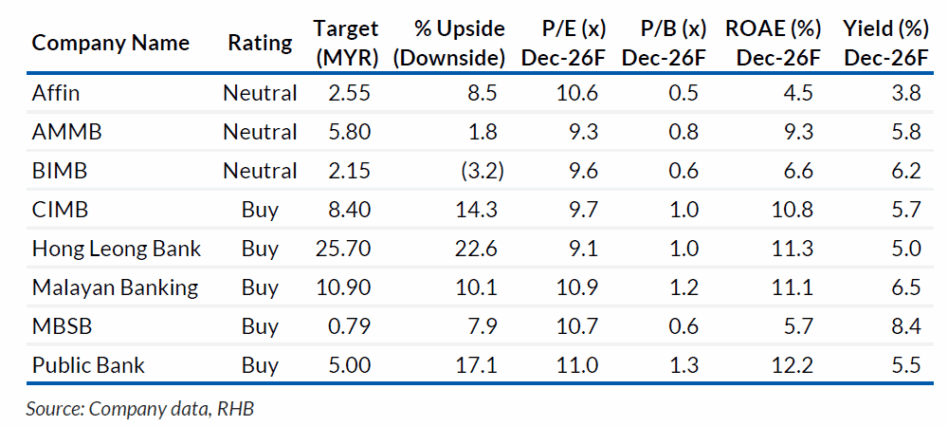

Bank Negara Malaysia’s (BNM) new capital framework on credit risk could see some banks unlocking excess capital that can be returned to shareholders – PBK and HLBK are key beneficiaries.

While harder to predict, the return of foreign institutional inflows would also be a key sector catalyst, with CIMB and PBK among the main recipients.

“We think the sector may see a lacklustre 3Q25 earnings season as domestic NIM will be impacted by July’s policy rate cut. In mitigation, we expect non-II to anchor operating income on the back of stronger wealth and markets-related fees while treasury & investments income could stay robust,” said RHB.

While we do not expect any major asset quality issues, the recent completion of an oil & gas corporate restructuring case paves the way for provision writebacks.

BNM, at its briefing in conjunction with the release of its 1H25 FSR, noted that the banking system stayed resilient in 1H25 despite global trade uncertainty and evolving geopolitical risks.

Banks’ asset quality remained intact, supported by stable household

and business GILs. Elsewhere, BNM is committed to helping banks transition to the Malaysia Overnight Rate and Malaysia Islamic Overnight Rate from the KLIBOR, a gradual process leading to the full cessation of the KLIBOR by 2029.

It also expects an aggregate neutral impact for banks under the internal ratings-based approach to capital calculations from the adoption of new Basel regulations for credit risk-weighted assets. —Oct 22, 2025

Main image: European Commission