JUNE rubber sector results were soft, largely due to a 10-day production halt caused by abrupt natural gas supply disruptions.

Volume increases were evident in July exports, but much of the increase was headed towards non-US markets that have lower average selling prices (ASP)s.

Meanwhile, despite softer input costs, sector pricing power remains weak, reflecting persistent oversupply and aggressive competition in both US and non-US markets.

“Against this challenging backdrop, RSTON remains our sole sector Top Pick,” said RHB.

The softness was compounded by global container vessel shipment issues and deferment of customer orders amid uncertainties over US tariff policies.

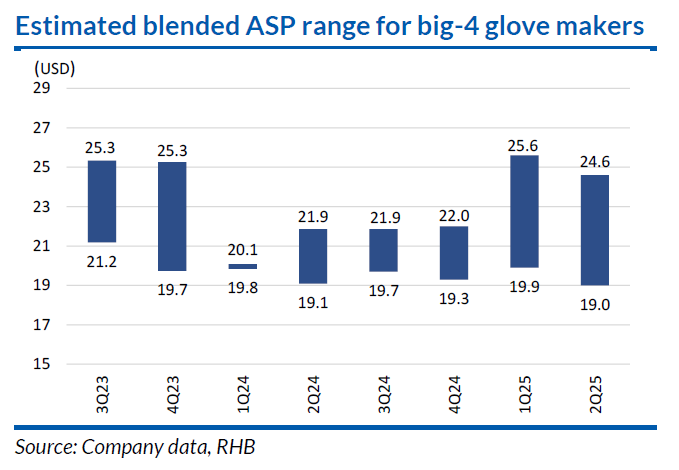

Profitability was also weighed down by the USD depreciating against the MYR. Industry-blended ASPs also declined sequentially, as cost pass-throughs remained difficult in the face of softening raw material prices.

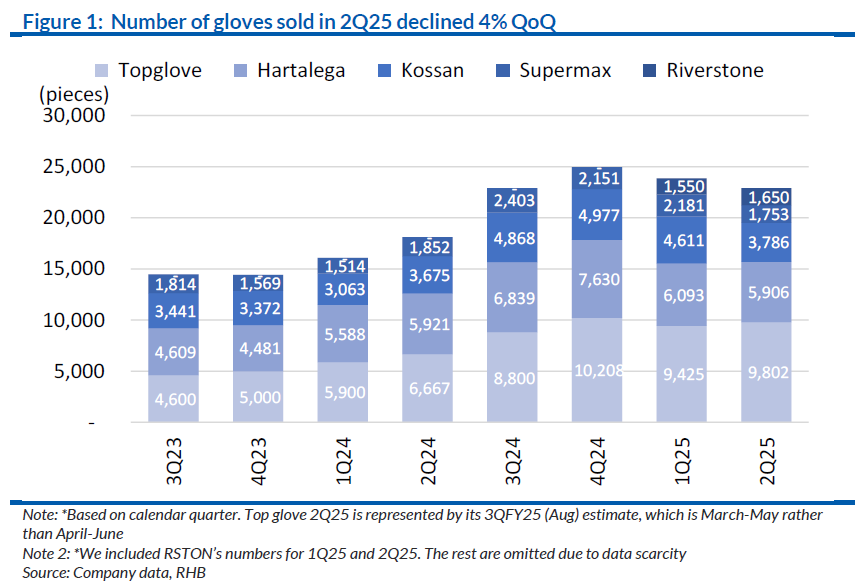

Malaysia’s glove exports rebounded 64% month-on-month (MoM) after four consecutive months of declines. However, the majority of the export volume increases were directed to non-US markets.

The US now accounts for 45% of Malaysia’s glove exports, down from 75% in June. This was despite flattish absolute shipment levels to the US.

Competition outside the latter nation remains far more intense due to aggressive pricing by Chinese manufacturers that continue to undercut regional peers.

Channel checks suggest that new capacities by Indonesia-based Chinese manufacturers are scheduled to begin operations in October.

Factory visits have likely already commenced, and large buyers typically require around four months of post-visit validations before placing major orders. In the best case, it may take 5-8 months before shipments begin.

We expect ASPs for generic gloves produced in these new plants to be USD1-2/1,000 pieces cheaper than the USD18-19/1,000 pieces currently offered by Malaysian manufacturers.

Overall, the commissioning of Chinese facilities in Indonesia and Vietnam, with an estimated total annual capacity of 10 bil pieces (6% of Malaysia’s Big Five capacities) poses a growing threat to domestic export share in the US market.

With consensus forecasts still running ahead of operating realities, the risk of earnings disappointments continues to outweigh any near-term valuation appeal.

Key risks to RHB’s sector call includes stronger USD, increase in glove ASPs, faster-than-expected capacity expansions, and lower-than-expected raw material prices. —Sept 19, 2025

Main image: Reuters