ONCE A niche manufacturing segment, the semiconductor industry now sits at the centre of global economic competition and technological advancement.

The industry, however, is not without its complexities. It is highly cyclical, often swinging between periods of shortage and oversupply.

But in February 2026, the global semiconductor industry maintained its strong growth momentum, with sales reaching USD88.8 bil, up 7.6% month-on-month (MoM) and 61.8% year-on-year (YoY), according to the Semiconductor Industry Association.

This marked the 28th consecutive month of YoY growth, driven by sustained demand from key areas, particularly data centre infrastructure and AI-related investments.

The continued expansion of data centre and cloud infrastructure, especially for generative AI workloads, has fuelled demand for high-performance logic chips and high-bandwidth memory, which account for more than half of total semiconductor sales.

“Overall, the global semiconductor market is expected to remain on a strong growth trajectory for the remainder of the year,” said TA Securities.

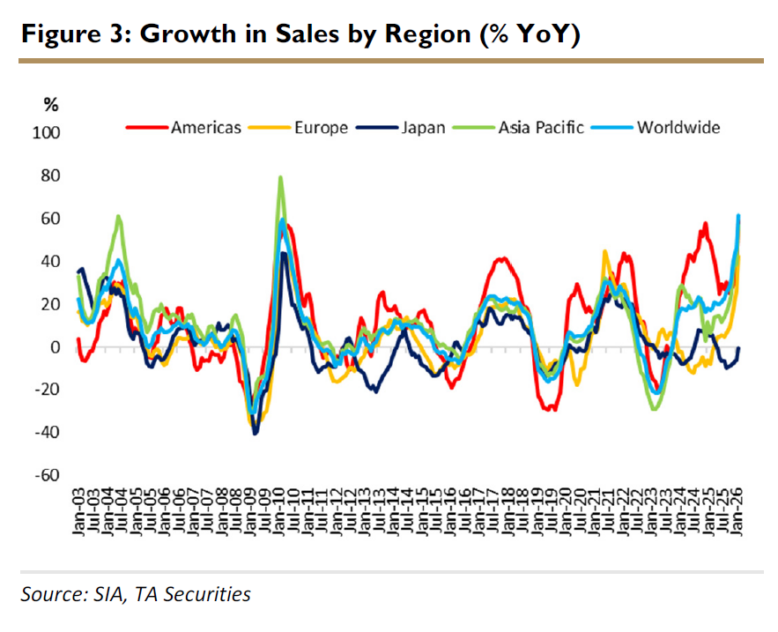

In terms of regional performance, YoY growth in February 2026 was broad-based across most regions, with the exception of Japan, which recorded a marginal decline of 0.3%.

The strongest growth was recorded in the Asia Pacific/All Other region (+93.5% YoY), followed by the Americas (+59.2% YoY), China (+57.4% YoY), and Europe (+42.3% YoY).

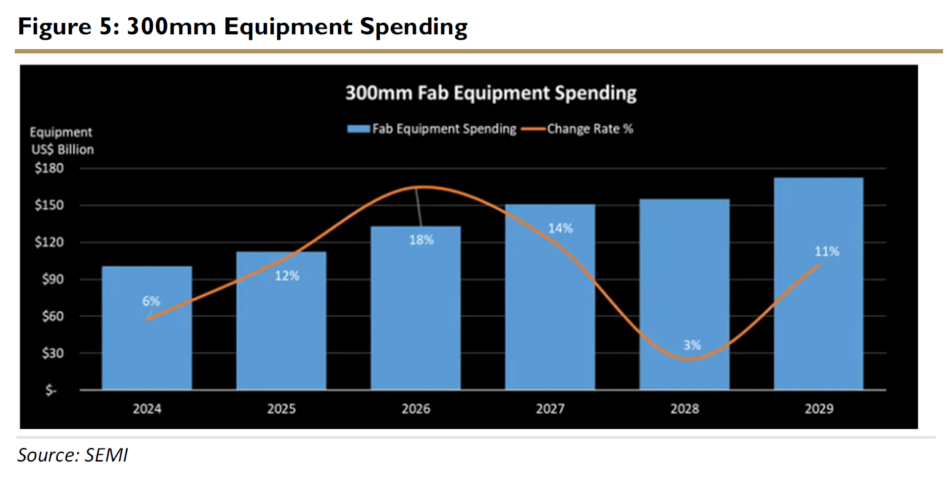

According to SEMI, global 300mm fab equipment spending is projected to grow by 18% to USD133 bil in 2026 and a further 14% to USD151 bil in 2027.

This expansion is expected to be continue driven by surging demand for AI chips used in data centres and edge devices, as well as increasing efforts by key regions to enhance semiconductor self-sufficiency through the development of localised industrial ecosystems and supply chain reconfiguration.

“Looking further ahead, investment is forecast to rise by 3% to USD155 bil in 2028, followed by an additional 11% increase to USD172 bil in 2029,” said TA.

The logic and micro segment are expected to lead equipment investment, with total spending projected at USD228 bil between 2027 and 2029, supported by robust demand from the foundry sector.

Demand for advanced node capacity remains strong, driven by increasingly stringent requirements from AI-related applications.

Despite continued growth projected for global semiconductor sales, supported by robust AI related demand, TA maintains a cautious stance on the semiconductor sector.

The outlook remains clouded by rising memory costs, which have led to higher prices for electronic products and could potentially dampen end-user demand.

In addition, ongoing tensions in the Middle East have resulted in higher logistics and material costs for the sector.

In addition, ongoing tensions in the Middle East have resulted in higher logistics and material costs for the sector.

That said, the overall impact is expected to remain manageable, as a portion of these costs can be passed through to customers.

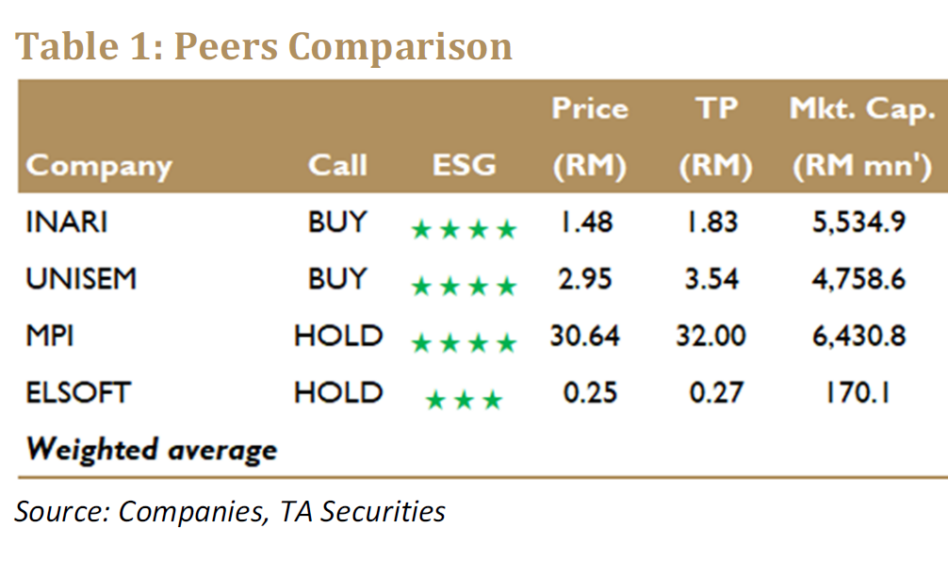

“All in all, we maintain our NEUTRAL stance on the semiconductor sector. We maintain our BUY recommendations on INARI and UNISEM, and HOLD recommendations on MPI and ELSOFT,” said TA.—Apr 15, 2026

Main image: KPMG