RHB MAINTAINS a positive stance on the technology sector for financial year 2026, especially as a key allocation for Shariah-compliant funds, supported by improving fundamentals, strong growth potential and a constructive outlook for the industry.

Among the companies under its coverage, six reported results that were in line with expectations, while five fell short due to softer sales, margin pressure, an unfavourable product mix, foreign exchange fluctuations and rising costs.

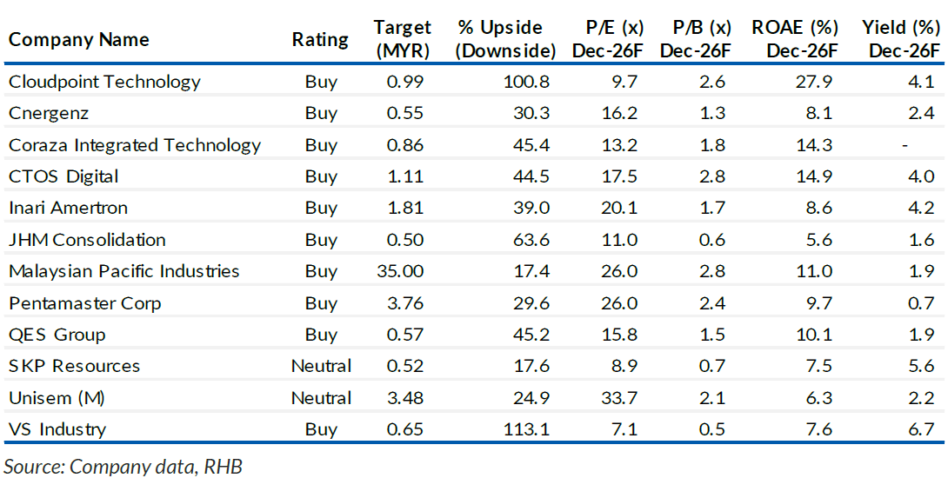

CORAZA was the sole outperformer, supported by margin expansion from economies of scale and robust revenue.

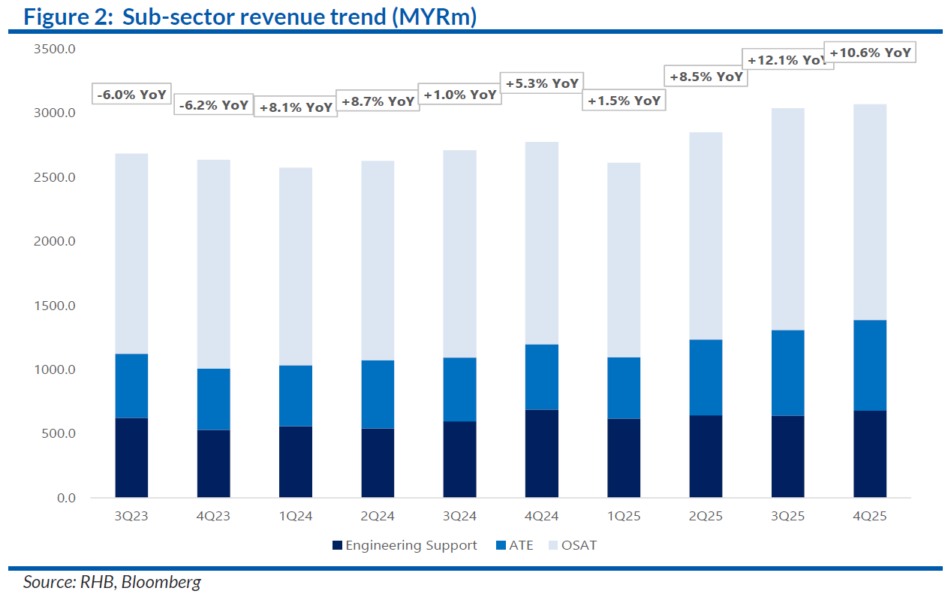

Sector core profit after tax, amortisation, and minority interest rose 1.3% year-on-year (YoY) and 28.1% quarter-on-quarter (QoQ).

Six companies posted stronger YoY earnings in quarter four 2025 (4Q25) while eight recorded better QoQ performance.

Most companies recorded YoY revenue growth, and the sector YoY revenue growth stood at 3.1% in 4Q25 and 8.4% year-to-date despite forex headwinds.

While margins were pressured by delayed repricing and cost pass-through, overall growth prospects remain supported by replacement cycles, automotive recovery, AI-driven upgrades, stronger server/peripheral demand and rising power management integrated circuit (PMIC) needs.

Management guidance remains constructive with improving loadings into 2026 and programme wins from project transfers and supply chain reallocation.

On the US-Iran conflict, Malaysia has minimal direct exposure as trade with Iran and the broader Middle East accounts for only 0.1% and 4.2% of total trade.

However, higher energy costs and a prolonged conflict could indirectly slow the semiconductor capital expenditure cycle and dampen electronics demand in the medium term.

Other key risks identified by RHB are such as elevated memory prices, obsolescence of technology, loss of customer/projects and forex.

RHB maintains Overweight on the sector. The improving sector revenue and earnings growth momentum should continue to prevail in 2026, supported by the ongoing global semiconductor recovery and robust AI-related demand.

Encouragingly, a broader-based recovery is already evident in the improving orderbook, revenue growth and earnings trends reported by many local technology names.

Engineering support and automated test equipment manufacturers should see sustained growth on rising semiconductor volumes and complexity.

OSAT players are positioned for recovery, though performance may vary by exposure.

The electronics manufacturing services segment remains challenging amid customer cost-down demands, sub-optimal utilisation and limited visibility.

Meanwhile, software and ICT players benefit from structural trends in digitalisation, cloud adoption, cybersecurity and IT refresh cycles. —Mar 16, 2026

Main image: PAMIR