SIME Darby’s (SIME) quarter one financial year 2026 (1QFY26) core profit of MYR335 mil came in largely within expectations, primarily driven by a surprise turnaround from the

China motor segment, but offset by a weaker-than-expected performance from the industrial business.

Its motor segment returned to the black with MYR126 mil in core profit before interest and tax (PBIT), led by China thanks to the special rebates received, narrowing discounts, and stronger sales.

The industrial segment’s PBIT margin eased to 6.6% due to:

i) Delayed new equipment deliveries in Australia (now expected in 2QFY26).

ii) Likely lower after-sales contributions,which typically have higher margins.

SIME expects quarter-on-quarter (QoQ) sales improvement and a slight margin uptick ahead, supported by higher average selling price and lower inventory costs.

“As such, we anticipate the company to book stable earnings for 4QCY25, further underpinned by robust Perodua sales, while the China motor division may remain volatile given the intensifying competition in that market,” said RHB.

TCM recorded another loss-making quarter, no thanks to the weak sales volume and high fixed costs.

RHB thinks this will continue, since management has yet to outline a clear strategy to address declining sales and mounting losses.

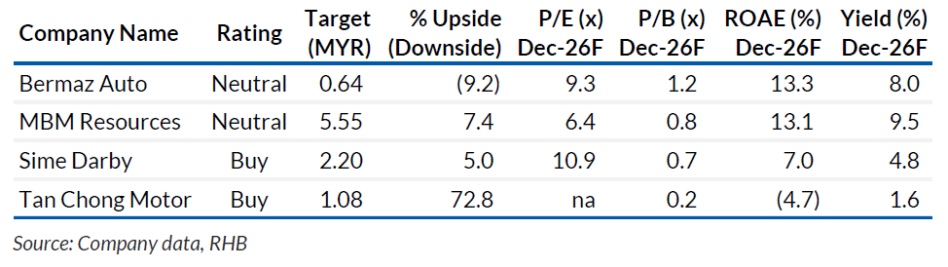

That said, RHB reiterate their BUY call, based on the intrinsic value of its underlying assets, although the time of realisation is uncertain at this juncture.

“We are also positive on TCM’s recent letter of intent with Perodua to rent out some of its assembly lines for the latter’s EV project, as this may help the group manage its fixed costs better by optimising the existing assembly plant’s capacity,” said RHB.

For MBM, the positive deviation mainly came from higher-than-expected Perodua sales volumes and share of associates.

This brought the nine months of 2025 (9M25) core earnings to MYR233 mil. Management guided that Perodua’s backlogs remained resilient at 89k (from 90k last quarter) and RHB has also lifted their sales volume assumptions for this marque accordingly.

“We recently lifted our 2025 total industry volume forecast to 795k units from 730k units, which implies a 3% YoY decline, on the back of supportive macroeconomic trend and seasonally stronger 4Q25 figure,” said RHB.

Key downside risks to RHB’s sector recommendation include softer-than-expected orders and deliveries, price hikes on complete knockdown cars post the Open Market Value or OMV duty revision, and intense price competition. The opposite represents the upside risks. —Dec 26, 2025

Main image: VisionX