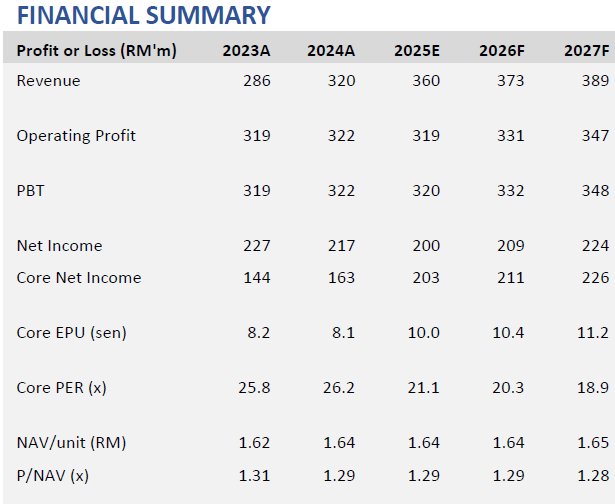

AXIS REIT nine months of financial year 2025 (9MFY25) core net income of RM153.3 mil came in within expectations, making up 76% and 73% of MBSB Research and consensus full year forecasts respectively.

Axis REIT announced distribution per unit (DPU) of 2.65sen for quarter three (3Q) FY25, bringing total distribution per unit (DPU) to 7.80sen in 9MFY25.

On a sequential basis, 3QFY25 core net income was marginally higher at RM52.2 mil, in line with higher topline. The earnings growth was largely supported by positive rental reversion of its industrial assets.

On a yearly basis, 3QFY25 core net income was higher at RM52.2 mil (+28% yoy), bringing 9MFY25 core net income higher at RM153.3 mil (+27% yoy).

The higher earnings were mainly due to contributions from newly acquired assets and positive rental reversion. Meanwhile, earnings per unit (EPU) grew by a milder quantum of 9.8% yoy due to dilutive impact from unit placement in 4QFY24.

Axis REIT remains on active acquisition to expand its industrial portfolio. Recall that Axis REIT announced acquisition of an industrial asset in Port Klang for RM80 mil in August 2025.

Besides, Axis REIT announced acquisition of an industrial asset in Klang for RM50 mil in September 2025. Meanwhile, Axis REIT is targeting to grow its portfolio via asset acquisition with estimated value of acquisition targets at RM300 mil.

“We see the active asset acquisitions underpin the long-term earningsgrowth of Axis REIT,” said MBSB.

MBSB sees the earnings outlook for Axis REIT to remain steady as earnings from industrial assets remain resilient. Nevertheless, distribution yield is unattractive at 4.3%. Hence, we maintain our Neural call on Axis REIT. —Oct 24, 2025

Main image: Axis REIT