MBSB Research maintains an upbeat outlook on the consumer sector, underpinned by resilient domestic spending conditions.

Key factors include steady employment levels, contained core inflation, ongoing government assistance through STR and SARA, as well as strengthening tourism activity in the lead-up to Visit Malaysia 2026.

“While the escalation in the Middle East has introduced a more tangible cost headwind, we believe the structural tailwinds underpinning consumer spending are sufficient to warrant maintaining our constructive sector stance for now,” said MBSB.

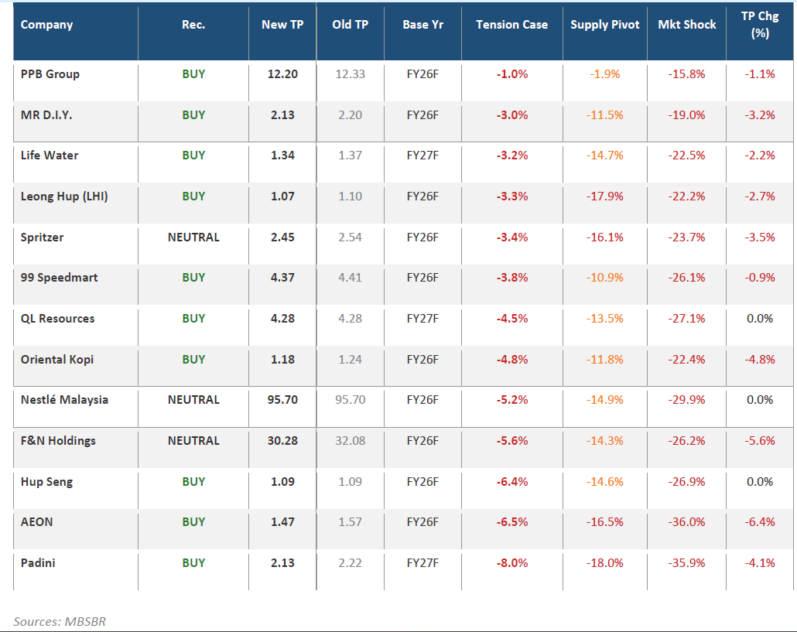

Their top picks are Leong Hup International (LHI) for its defensive exposure to staple protein demand, MR D.I.Y. for its resilient value-driven retail model and procurement scale advantages, and 99 Speedmart, which stands to benefit from downtrading behaviour and remains well insulated through its centralised logistics platform.

The escalation in the Middle East has moved beyond the level of a hypothetical risk. With the conflict now entering its fifth week, oil prices remain elevated, freight rates have risen materially, and fertiliser markets have repriced.

The Strait of Hormuz is functioning at a fraction of the capacity, with a significant risk premium being reflected in procurement costs, logistics quotes, and supplier pricing across the consumer supply chain.

99 Speedmart is one of the most defensive names under a Middle East shock. ~70% of revenue is derived from food essentials and ~85% of its customer base skews toward B40/M40 households, supporting demand resilience.

The fully centralised procurement and logistics platform preserves shelf availability and supplier negotiating power, while meaningful other operating income (OOI) from supplier-funded allowances enhances profitability despite thin gross margins. SARA and other government assistance related spending continues to underpin traffic.

“We maintain a positive view on 99 Speed Mart, underpinned by its scale-driven cost advantage and staples-focused demand profile,” said MBSB.

Its “Near ’n Save” value positioning remains well aligned with resilient mass-market spending, and continued network densification should sustain operating leverage.

However, MBSB now factors in near-term margin pressure from higher logistics and operating costs related to the Middle East disruption.

The group’s defensive demand profile and centralised procurement model should help contain the impact, but earnings momentum will be modestly lower than previously assumed.

LHI faces direct transmission through soy and corn accounting for ~70% of COGS. However, chicken and eggs remain staple proteins, end-demand is comparatively resilient, and the industry has greater scope to reprice than many discretionary consumer businesses.

“We remain constructive on LHI’s prospects despite the earnings trim. Firm domestic demand. Ongoing cost discipline and operational optimisation are expected to sustain margin improvement, even as geopolitical uncertainty adds a layer of near-term cost volatility,” said MBSB. —Mar 27, 2026

Main image: Veeve