THE lacklustre stock market sentiment as reflected by Bursa Malaysia’s FBM KLCI is expected to continue for the next few months despite forward valuations falling to two standard deviations below the post Global Financial Crisis (GFC) mean.

CGS-CIMB Research expects such trend to last until closer to 4Q 2023 when two significant re-rating catalysts emerge to spark a potential structural shift in liquidity flows and domestic sentiment.

These catalysts are:

- A convincing break down of the US Dollar Index (DXY) below the psychological 100 mark; and

- Further easing of political uncertainties in Malaysia post the six state elections that are expected to be held by end-August. This will help pave the way for Prime Minister Datuk Seri Anwar Ibrahim’s administration to focus on medium-term economic plans and policy reforms.

According to CGS-CIMB Research, the potential upsides – should both key catalysts materialise – should not be under-estimated by taking into consideration the following:

- Depressed valuations: The FBM KLCI trades at 13.9 times forward price-to-earnings ratio (P/E) while the FBM 100 is cheaper at 13.4 times versus historical means of 17.1 times and 17.7 times respectively.

- Improved domestic growth: Driven by a confluence of tail-end effects of the post COVID-19 economic re-opening, continued subsidies, higher minimum wage and labour market recovery.

- An undervalued currency: Supported by a healthy current account surplus and potentially better interest rate differentials.

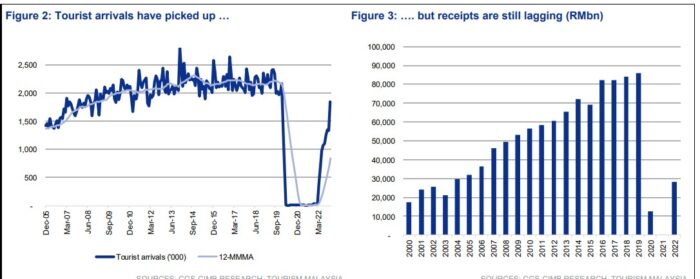

- Upside from a pick-up in tourism over the next 6-18 months: Chinese arrivals into ASEAN are only 20% of pre-pandemic levels so far but there is potential for arrivals to surpass the previous 2019 peak in about a year as projected by the research house’s economist Nazmi Idrus in a report entitled “China re-opening gains might be limited” dated May 2, 2023.

“This could provide further impetus to the economy and current account surplus, in our view, especially in 2024. Tourist receipts amounted to RM28.2 bil in 2022 compared to RM86.1 bil in 2019 and last year’s current account surplus of RM47.2 bil,” envisages analyst Chehan Perera in a Malaysia Strategy update.

While there is room for potentially one more greenback rally over the summer, CGS-CIMB Research expects this to be the beginning of the end to the rising US dollar trend.

“We expect the US Dollar Index (DXY) to break below 100 by 4Q 2023 and trade down to the 90-95 range over 2024, driven by muted US economic growth, a slightly dovish US Federal Reserve and absence of extraordinary monetary stimulus,” anticipated the research house.

“In addition, contrary to some expectations, we think Malaysia’s national unity coalition will perform reasonably well in the upcoming six state elections on the back of a robust domestic economy. The impact on liquidity flows into surplus countries such as Malaysia where domestic growth is good and the currency undervalued could be relatively strong.”

All-in-all, CGS-CIMB Research’s earnings gap analysis shows that the FBM KLCI could reach 1,610 points by year-end and 1,800 points by end-2024.

At the time of writing, the benchmark FBM KLCI index is down 1.73 points or 0.12% to 1,379.53 with Malacca Securities Research expecting support to be located at 1,370, while resistance is envisaged along 1,400-1,440. – June 6, 2023