MALAYSIA’S data centre (DC) industry continued to expand in 2026, driven in part by geopolitical developments that prompted many Western operators to shift investment focus from the Middle East to Southeast Asia.

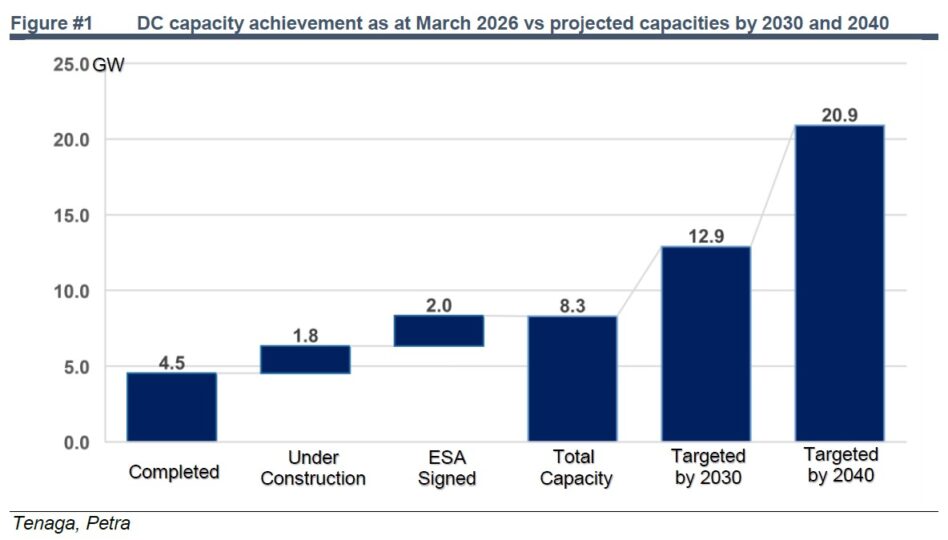

Tenaga has already secured Energy Supply Agreements totalling 8.3GW, while discussions are ongoing for an additional 10GW of capacity.

This trajectory aligns closely with the Ministry of Energy Transition and Water Transformation’s long-term target of achieving 20.9GW of data centre capacity by 2040.

As data centre capacity grows, electricity demand is rising in tandem. YTL Power has doubled its planned data centre capacity in Kulai to 1.2GW from the original 600MW, reflecting robust demand from Western operators.

The company is also exploring further land acquisitions in the Klang Valley with the intention of eventually expanding total capacity to 2.4GW.

Utility demand remained resilient during the first quarter of calendar year 2026, underpinned mainly by the data centre segment.

Data centre electricity load utilisation climbed to 1,054MW in March 2026, more than double the 485MW recorded a year earlier.

Electricity consumption across Peninsular Malaysia increased 7% year-on-year during the quarter, while gas usage for power generation rose 17.8% and solar generation expanded 11.3%.

Tenaga also registered a new record peak electricity demand of 21.5GW on April 23, surpassing the previous high of 21GW recorded in May 2025.

Utility demand is expected to remain on an upward trajectory in the second half of 2026 as more data centre projects come online.

The rapid growth in electricity consumption from data centres, coupled with Malaysia’s commitment to achieving net-zero emissions by 2050, is expected to accelerate investments in new gas infrastructure to support rising demand while replacing ageing coal-fired generation.

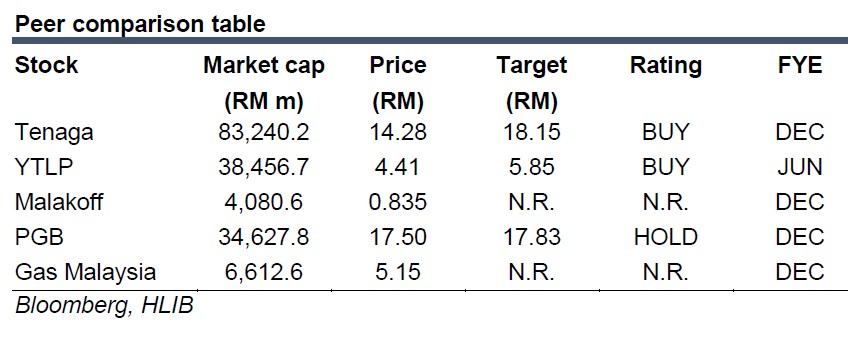

Companies with strong financial positions and proven execution capabilities, such as Tenaga, YTL Power and Petronas Gas, are viewed as key beneficiaries.

The Energy Commission has awarded the Tenaga-Aurora consortium a 1.4GW combined-cycle gas turbine (CCGT) project in Paka under the NewGen25 programme, while further CCGT tenders scheduled for 2029 to 2031 are expected to create additional opportunities.

Separately, Petronas Gas and Gas Malaysia have received approval to develop the RGT-3 and RGT-4 regasification terminals, with Tenaga partnering Petronas Gas on the RGT-3 project.

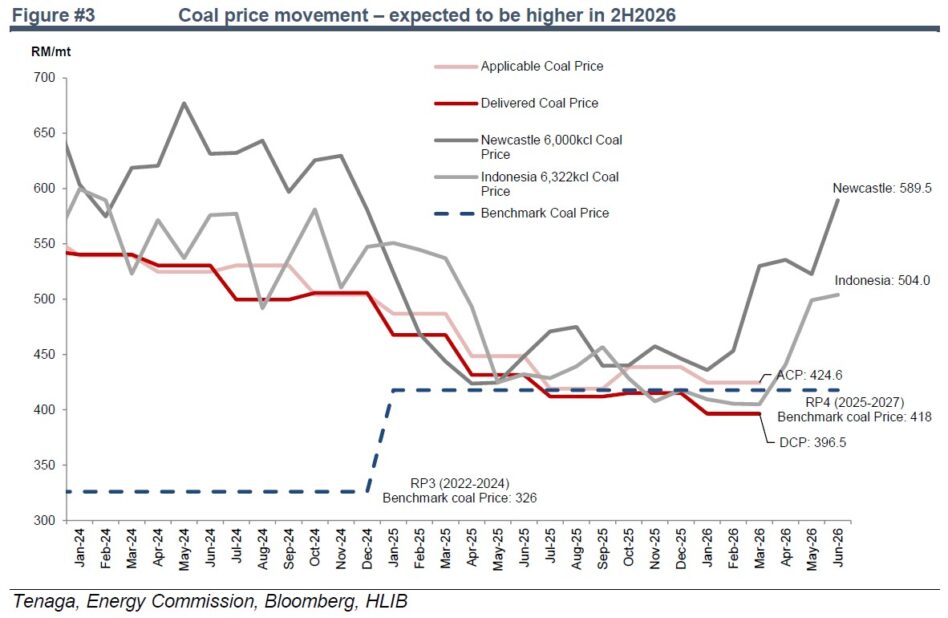

Global coal and gas prices climbed following the outbreak of the Iran conflict in March 2026.

However, the impact on Malaysia’s domestic gas pricing is expected to be felt only after a lag of about four months under Petronas’ pricing mechanism, with higher gas prices taking effect from July onwards.

Coal prices were also supported by Indonesia’s export restrictions and stronger seasonal demand from Northeast Asia before easing towards the end of June amid concerns over slowing global economic growth.

Newcastle coal averaged about US$128 per metric tonne in June, while Petronas’ regulated gas tariff increased to RM35.95 per mmbtu in April.

Given the sector’s resilient earnings outlook and stable dividend prospects, the research house continues to maintain an OVERWEIGHT recommendation on Malaysia’s utilities sector.—July 6, 2026

Main image: The Borneo Post