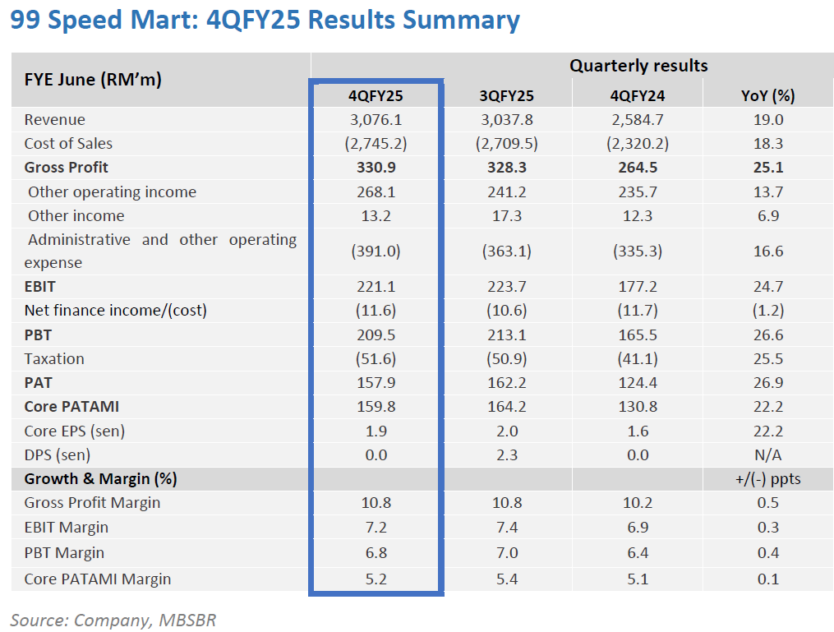

NOTE that 99 Speed Mart delivered a strong quarter four financial year 2025 (4QFY25) performance, with results coming in within expectations.

This is underpinned by continued network expansion, resilient same-store sales growth, and sustained demand for daily essentials.

The quarter was supported by positive contributions from new outlets, steady basket size improvement, other operating income growth, and increasing traction from its bulk sales e-commerce platform.

Margins remained stable despite higher operating costs from minimum wage adjustments and outlet additions. “We leave our forecasts unchanged and maintain our BUY call and target price of RM4.41,” said MBSB.

The Group ended the year with 3,037 outlets, following a net addition of 259 stores in financial year 2025 (FY25), while total sales transactions increased +17.4% year-on-year (yoy) with a slightly higher average basket size of RM21.7.

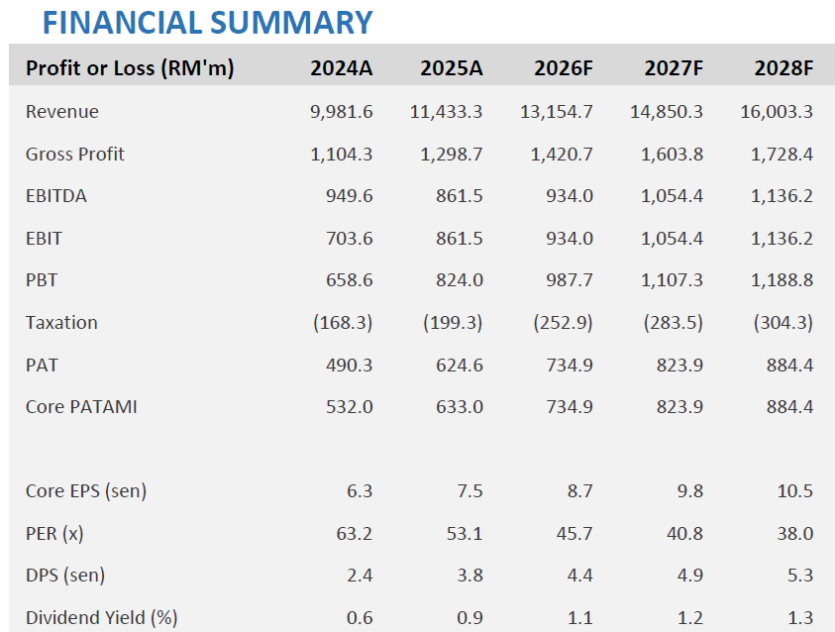

On a full-year basis, FY25 revenue grew +14.6% yoy to RM11.43 bil, underpinned by new store contributions and incremental sales from its bulk e-commerce platform, while total sales transactions grew +14.3% yoy to 532 mil and basket size averaged RM21.5 through the year.

99 Speed Mart’s 4QFY25 core profit after tax and minority interest (PATAMI) increased 22.2% (yoy) to RM159.8 mil, outpacing revenue growth, driven by stronger gross profit expansion and improved operating leverage from higher sales volumes and outlet expansion.

On a full-year basis, FY25 core PATAMI rose +19.0% yoy to RM632.9 mil, underpinned by resilient same-store sales growth (+7.8%yoy), disciplined cost management and sustained benefits from scale across its expanded store base, namely higher other operating income, which saw an increase of +15.3%yoy to RM939.6 mil that further supported profitability despite increased staff and depreciation costs.

“We maintain a positive view on 99 Speed Mart, underpinned by its scale-driven cost advantage, staples-focused demand profile, and disciplined rollout of ~250 outlets annually,” said MBSB.

Its “Near ’n Save” value positioning keeps it aligned with resilient mass-market spending, supported by stable employment and ongoing fiscal assistance.

Continued network densification, logistics optimisation and positive SSSG should sustain operating leverage, while expansion of its bulk sales platform offers incremental growth upside. —Feb 16, 2025

Main image: Malay Mail