YEAR-TO-DATE production of 10.77 mil MT is running at 4% above the 10-year Malaysia Jan−Jul output of 10.35 mil MT. However, the stronger-than-average trend in output is in line with expectations.

Oilworld is expecting 19.3 mil MT of palm oil from Malaysia in calendar year 2025 (CY25), while the USDA is forecasting 19.4 mil MT and Kenanga is estimating 19.2 mil MT, all above the historical 10-year average of 19.0 mil MT.

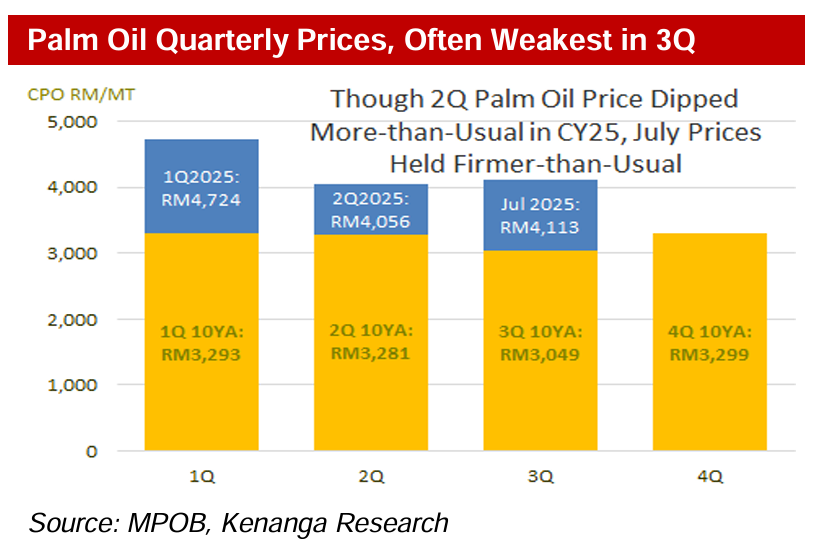

Typically, global edible oil price corrects by about 4% quarter-on-quarter (QoQ) in 3Q, and then recover in 4Q. Historically, Malaysian crude palm oil (CPO) prices also softened in 3Q by 7% QoQ but so far, July CY25 CPO price has held steady.

“We attribute this to the more-than-usual dip in 2Q CY25 palm oil prices after trading at premium to soyabean oil for seven months in CY24 then into 1QCY25 as well,” said Kenanga.

Edible oil supply is expected to improve by only 1−2% in CY25 whereas trend-line demand growth is closer to 3−4% YoY.

As such, edible oil prices, including palm oil prices, are expected to stay relatively firm in order to contain demand growth below trend line. Supply outlook for CY26 is better but only slightly.

With a forecast YoY increment of 2−3% in supply, CY26 closing inventory should stay flat or nudged up a little (2−3%) as elevated prices temper down demand.

However, the overall supply-demand scenario remains tight with little room to accommodate supply disruption from poor weather, supply-chain or geopolitics.

Softer CPO prices should weigh down upstream margins but overall cost pressure is tempered somewhat by elevated PK prices which are still stronger by 45% YoY even after correcting in June.

Meanwhile, PKO price discount to rival coconut oil has widened again on tight coconut supply due to dry weather.

While the direct impact of US tariff is limited as palm oil-based fatty acids are exempted, the lingering uncertainties and worries over slower economic activity are limiting order size and nearer term deliveries.

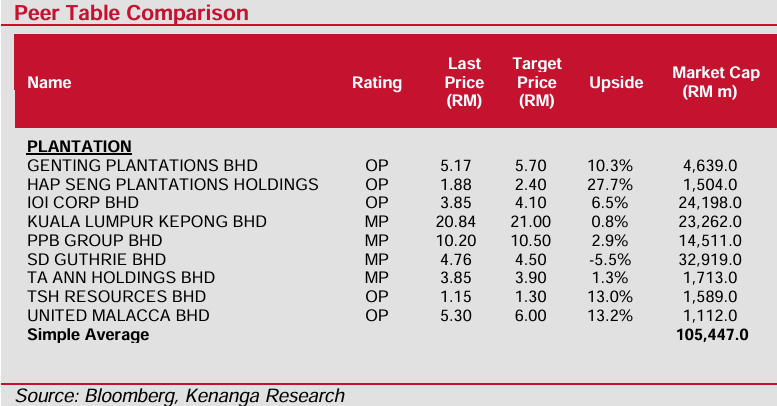

2Q CY25 plantation earnings are expected to soften but only slightly, so healthy profits can still be expected on expected CPO prices of RM4,100 and RM4,000 per MT over CY25−26 respectively.

There is no strong upside catalyst, thus our NEUTRAL weight for the sector. —Aug 12, 2025

Main image: The Edge