PETRONAS’ first half of 2025 (1H25) cumulative revenue declined 15% due to both decline in production volume and average realised prices in the upstream division.

That aside, downstream division and gas division also saw decline in top line due to lower realised prices and due to lower volume of gas processed. Core profit declined 37% as a result of relatively stable year-on-year (YoY) overhead costs and slightly higher finance costs.

Nevertheless, gross margins for upstream and gas divisions remained largely unchanged YoY while only downstream saw a deterioration of margins in 1HFY25.

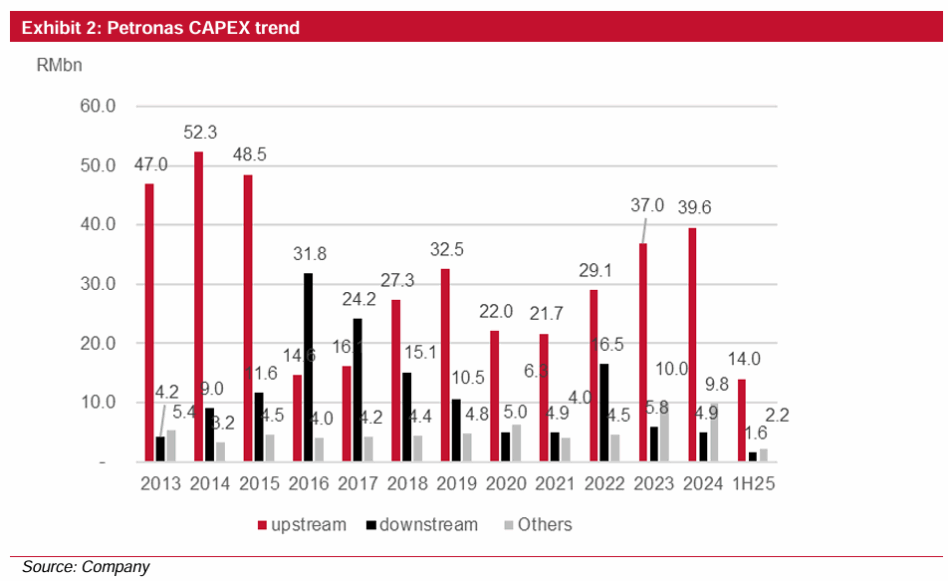

Petronas capital expenditure (capex) for both upstream and the gas divisions were at RM14 bil in 1HFY25, a 31% YoY decline which shows the group’s intention to slow down its upstream capex amid tepid Brent crude prices and uncertainties on the details of gas aggregation rights being passed over from Petronas to PETROS.

RM1.6 bil were spent on downstream and RM2.2 bil were spent on green energy and others.

Nevertheless, we took slight comfort in the group’s cash generative ability as it recorded an operating cash flow of RM48 bil, a 12% increase despite the larger drop in its top line.

Based on previous track record, the group’s capex spent of RM40-50 bil was back in 2017-2019, whereby upstream serve providers witnessed a slowdown in activities.

But what might be different in this cycle is the fact that the downstream capex requirements will be lower due to the lack of new announcements in Pengerang, Johor, leaving a bigger wriggle room for upstream capex in FY25F.

It is well recognised that Petronas is undergoing a strategic transformation focused on portfolio optimisation, as well as improvements in productivity and operational efficiency.

In line with this shift, we do not rule out the possibility that Petronas may increasingly allocate its upstream capex towards Peninsular Malaysia and Sabah versus towards Sarawak, pending the finalisation of gas aggregation profit-sharing arrangements with the Sarawak state government.

Beyond capex, we also see heightened likelihood of opex rationalisation, which could result in a scaling back of opex-related maintenance activities in FY25F and potentially into FY26F, particularly if Brent crude prices remain subdued.

As such, we anticipate that most upstream service providers will face a softer orderbook or reduced asset utilisation in the near term, barring a material improvement in the sector’s macro outlook.

In the short term, we still prefer to avoid upstream service providers subsector due to uncertainty of Petronas capex and opex trends albeit we recognize admittedly that some of the counters’ valuation have dropped to extremely attractive levels.

Near-term catalysts appear to be few and far between for upstream service providers. We have recently turned positive on the downstream segment as we have upgraded PCHEM given the supply increases globally might not be as flush as expected earlier.

This is due to China’s proposed anti-involution policy (which could at least result in a temporary shutdown of significant capacities of petrochemical facilities in China) and Korea’s commitment to cut capacity to weed out aging and unprofitable plants. —Sept 2, 2025

Main image: The Star