BANK Negara Malaysia (BNM) kept the Overnight Policy Rate (OPR) unchanged at 2.75% at its fifth Monetary Policy Committee (MPC) meeting of the year, in line with Kenanga’s expectations and market consensus.

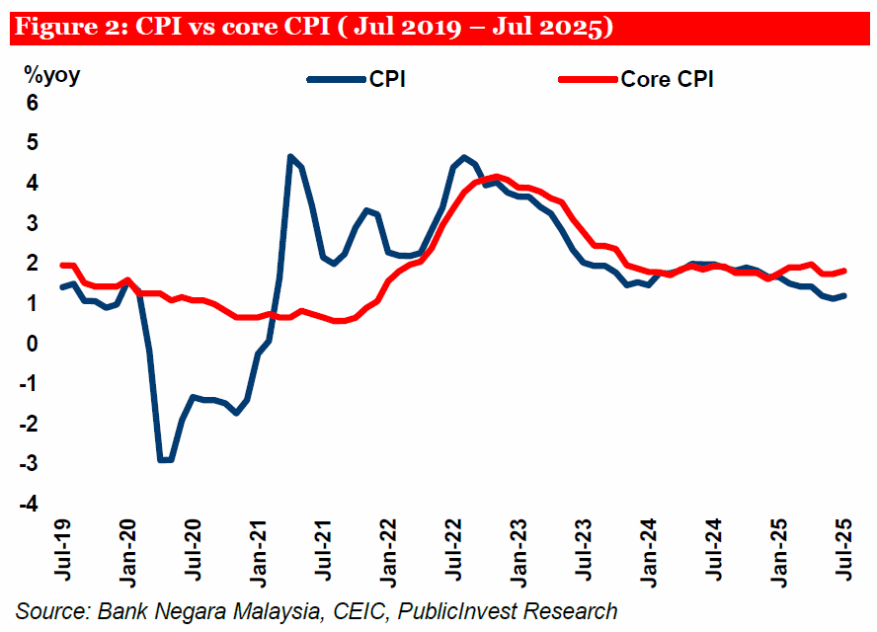

BNM characterised the current policy stance as appropriate and supportive of the economy amid prevailing price stability.

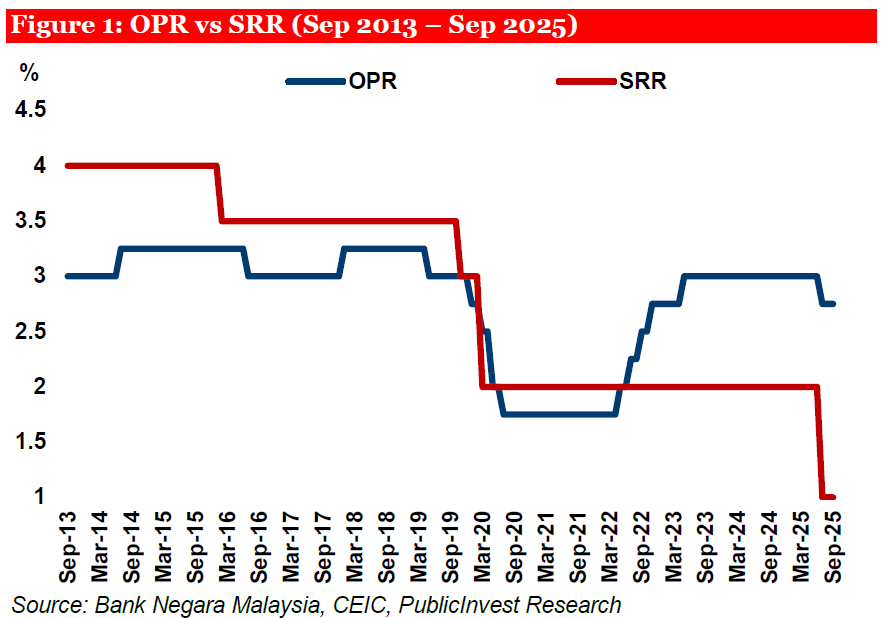

The Statutory Reserve Requirement (SRR) was also held steady at 1.00%, following the 100bps reduction delivered in May.

The Malaysian economy expanded by 4.4% year-on-year (YoY) in the first half of 2025 (1H25), supported by sustained private consumption and robust investment activity.

“The economy remains on track to grow within the official range of 4.0% to 4.8% for the full year, underpinned by resilient domestic demand and targeted fiscal support,” said Kenanga.

BNM noted that looking ahead to 2026, household spending is expected to remain firm, aided by steady employment gains, positive wage growth, and income-related policy measures.

Investment activity is expected to continue to strengthen, driven by the rollout of multi-year infrastructure and industrial projects across both public and private sectors.

The high realisation rate of approved investments, alongside catalytic initiatives under the national master plans and the Thirteenth Malaysia Plan (13MP), is likely to provide an additional lift to medium-term growth momentum.

BNM continues to acknowledge that the outlook remains exposed to downside risks, largely stemming from weaker external demand conditions.

The September statement retains references to slower global trade, softer sentiment, and lower-than-expected commodity production as the key drags on growth.

However, unlike in July, the narrative introduces moderating counterweights, including ongoing demand for E&E products, resilient tourism activity, and the possibility of favourable outcomes from remaining US trade negotiations.

The overall tone is incrementally more balanced, suggesting that while external risks have not receded, the domestic outlook remains supported.

BNM retained its view of sustained global growth momentum, underpinned by resilient consumer spending and near-term front-loading.

However, the September statement places greater emphasis on the transition from uncertainty to implementation.

Compared to July, the tone subtly evolves, while labour market strength, accommodative fiscal policy, and looser global monetary settings continue to support the growth outlook, the risk narrative has shifted.

The earlier focus on “uncertainties surrounding tariff developments” has now been replaced with a more grounded assessment, as announced tariff measures take effect, particularly on product-specific lines.

Importantly, BNM acknowledges that while front-loading activities are likely to fade, the overall impact of trade restrictions could persist, albeit to a less severe degree.

The inclusion of lingering geopolitical tensions reaffirms downside volatility, but the statement also introduces upside potential via possible breakthroughs in remaining US trade negotiations and pro-growth policy actions in major economies. —Sept 8, 2025

Main image: AFP