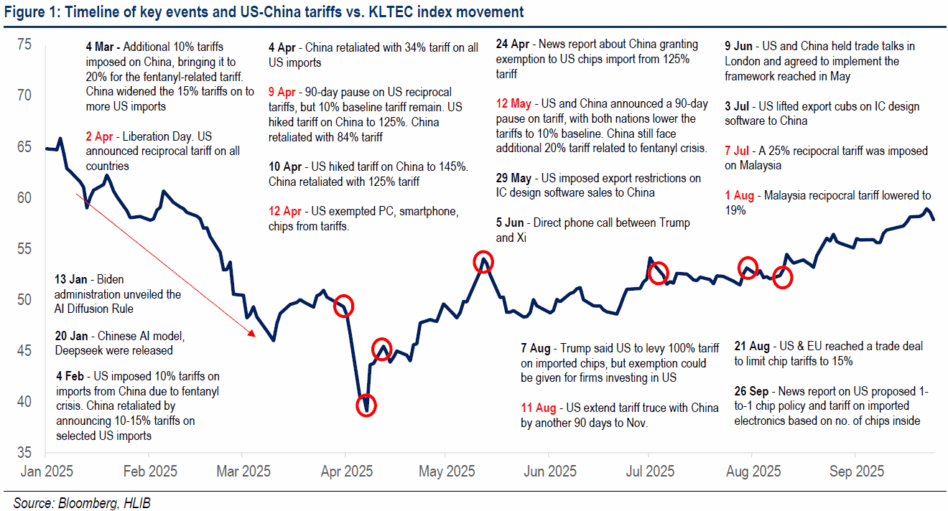

WITH the recent newsflow on US tariffs heating up, Hong Leong Investment Bank (HLIB) believes an announcement on Section 232 semiconductor tariffs could come soon.

“We take this opportunity to discuss recent developments below and assess potential tariff implications for each tech companies within our coverage,” said HLIB.

The WSJ reported on a draft US government proposal that would require semiconductor firms to match every imported chip with a domestically produced chip, or otherwise face penalties (potentially up to a 100% import tariff).

HLIB views the intention behind this policy move as a clear attempt to drive the reshoring of chip production, but key implementation details remain absent.

From a supply chain perspective, a strict 1:1 import/domestic output ratio is riddled with complexity, as the semiconductor supply chains are deeply globalised and interconnected.

A single IC chip is composed of dies, substrates, package, test, etc. Many of these steps are done across borders, for example, design in the US, wafer fabrication in Taiwan, packaging and testing in Southeast Asia, and final assembly in China.

To impose a strict 1:1 import-to-domestic output ratio, US authorities would need unprecedented supply-chain visibility, traceability systems, and audit mechanisms.

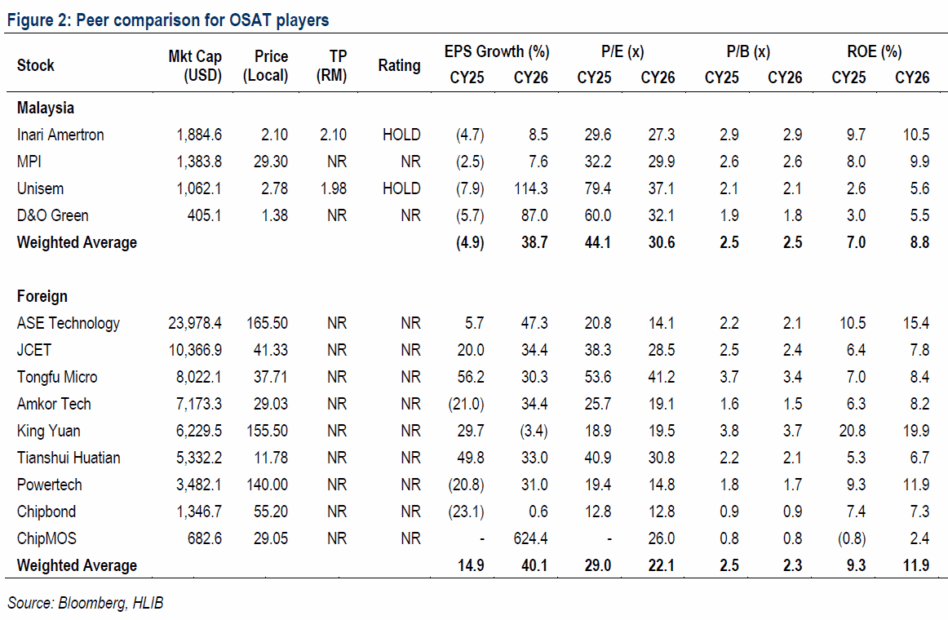

In summary, the direct tariff impact on Malaysia-listed tech stocks appears limited, given their relatively low direct exposure to the US market.

In addition, major US tech companies with huge domestic investments have been able to secure tariff exemptions, mitigating some of the headline risk, in our view.

That said, the greater risk lies in indirect or second-order effects, such as weaker end-demand, which are harder to quantify but could have a far bigger impact on the sector.

For now, the sector has yet to experience material disruption, given the ongoing tariff exemptions on chips and the temporary US-China tariff truce.

As noted earlier, Section 232 chip tariffs remain pending, the China tariff truce has been extended, and market is pricing in further Fed rate cuts — factors which have kept the tech sector trending higher recently.

From here, HLIB thinks focus will likely pivot to hard economic data to gauge the impact of reciprocal tariffs that took effect in August, while awaiting for the final decision on Section 232 sectoral tariffs, and the expiry of the 90-day China tariff truce in November. —Sept 29, 2025

Main image: The Star