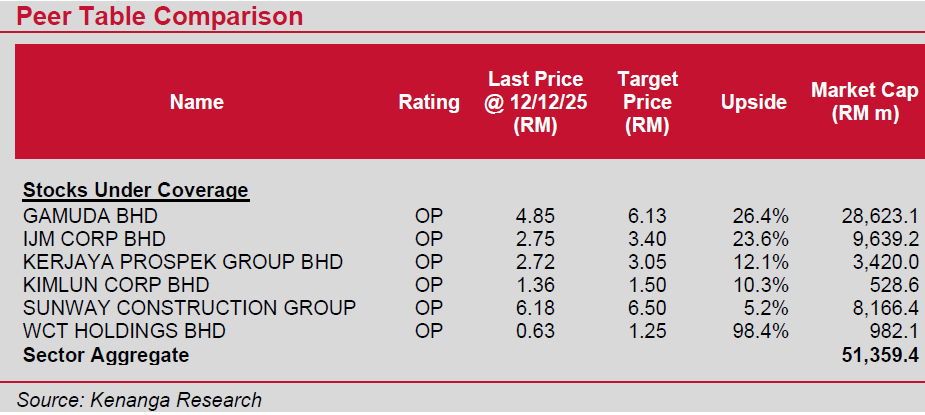

THE construction sector has delivered a strong two-year run, with the KLCON Index rising 70%, driven primarily by SUNCON (+214%) and GAMUDA (+122%).

This surge was underpinned by the rapid roll-out of data centre contracts. With several near-term data centre project awards in the pipeline and overall data centre development expected to stretch well into 2030, Kenanga expects data centre-related contracts to remain the dominant growth driver for the sector in 2026.

According to the Construction Industry Development Board (CIDB), RM182.3 bil worth of main contractor contracts were awarded year-to-date (YTD) as at end-November 2025, surpassing our full-year 2025 forecast of RM180 bil.

Private sector projects accounted for 79%, with government projects making up the remaining 21%. That said, matching the RM231.4 bil recorded in 2024 remains a tall order.

“For 2026, we maintain our contract award assumption of RM180 bil, supported by continued public-sector project rollouts and sustained private-sector momentum, particularly from data centres,” said Kenanga.

While the roll-out of major infrastructure works has been slower than expected, our constructive view on the sector in 2026 remains unchanged.

Sector visibility continues to improve on both public infrastructure and private development fronts.

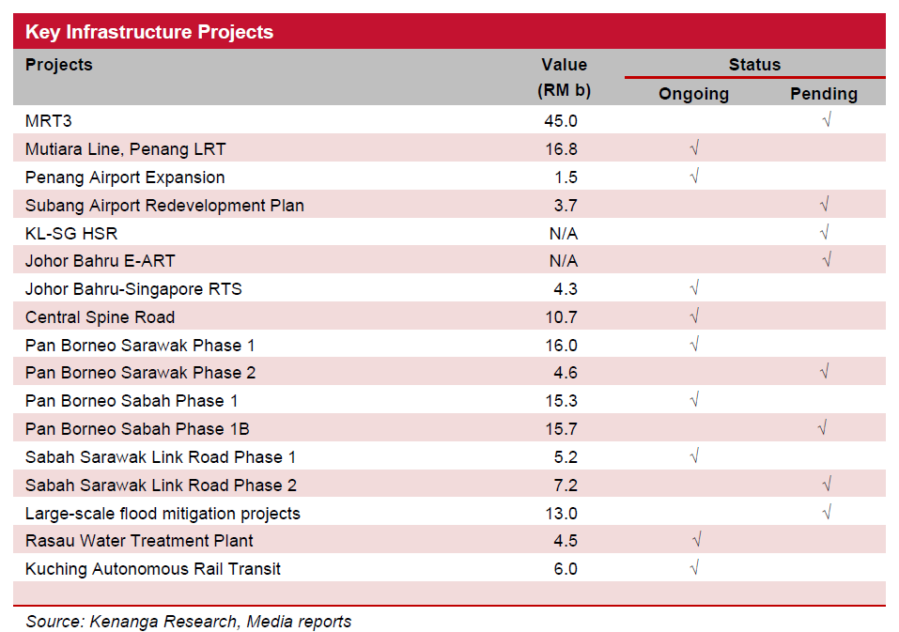

Although the timing for MRT3, now with final approval from the Transport Ministry, remains unclear, several key projects are poised for near-term roll-out.

These include the Penang LRT Mutiara Line Packages 2 & 3, Penang Airport expansion, Phase 2 of the Pan Borneo Highway, the Sabah–Sarawak Link Road, Subang Airport redevelopment, and the Johor E-ART.

In addition, the KL–Singapore High Speed Rail remains a medium-term catalyst.

Meanwhile, finalisation of the Upper Padas Water Dam (Sabah) and the Kerian Water EPCC (Perak) is still pending, though GAMUDA has already secured both water concessions.

In 2025, six major land transactions involved US tech giants, with Microsoft and Pearl Computing each acquiring two parcels for data centre expansion.

Notably, GAMUDA sold a 389-acre parcel at Springhill Industrial Park, Port Dickson to Pearl Computing for RM455.2 mil, alongside RM1 bil of enabling infrastructure works.

This positions GAMUDA favourably for follow-on work at the site, which can host 800MW-1,000MW of data centre capacity, translating into RM14 bil-RM20 bil in construction value.

GAMUDA has already secured two of Pearl Computing’s core and shell DC packages worth RM2.14 bil via ECOWLD, with M&E works pending award.

In October 2025, IJM also secured a milestone win from Pearl Computing – RM1.26 bil in core and shell works from SIMEPROP and RM874 mil in M&E works directly from Pearl Computing.

Two additional Pearl Computing data centres in the Klang Valley are pending awards, while initial tenders for Springhill are expected to roll out progressively starting quarter two of 2026 (2Q 2026).

GAMUDA, SUNCON, and IJM remain active bidders across these packages.

According to TENAGA, eight data centre projects (1.1GW) had signed Energy Supply Agreements (ESAs) YTD to September 2025, bringing the cumulative total to 49 projects (7.1GW), of which 18 projects (3.8GW) are already completed.

“We expect the data centre boom to persist for at least the next two years and maintain our assumption of 700MW of new annual capacity, equivalent to about RM21 bil worth of data centre construction value each year,” said Kenanga.

Despite slower than expected infrastructure project roll-outs, we remain bullish on the sector, supported by persistently strong data centre demand and sustained capex commitments from global tech firms. —Jan 12, 2026

Main image: Propertyguru