CIMB hosted an analyst briefing to provide updates on the latest operational and corporate developments.

CIMB Niaga and CIMB group’s quarter four financial year 2025 (4QFY25) results are scheduled to be announced on 25 Feb and 27 Feb respectively.

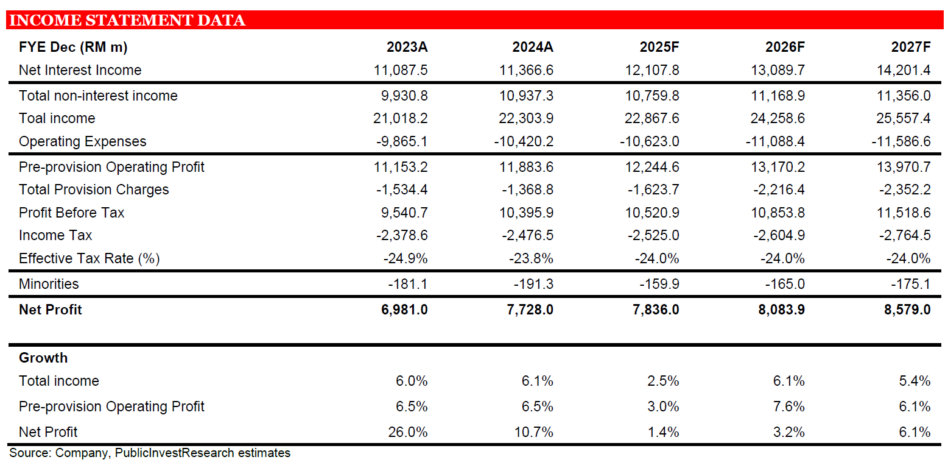

“We expect 4QFY25 results to remain resilient year-on-year (YoY), as the lower operating expenses and credit cost should help offset softer non-interest income (NOII),” said Public Investment Bank (PIB).

In addition, PIB gathered that Malaysia’s wholesale loans are gaining traction. PIB expects net interest margin (NIM) to improve sequentially on deposit repricing.

They continue to like CIMB on the back of potential NIM recovery, healthy asset quality that could translate to lower credit cost, and attractive dividend yield supported by its RM2 bil capital return program.

Loan growth momentum picked up significantly, due to strong drawdowns in Malaysia wholesale loans.

Meanwhile, Singapore loan growth momentum continue to be driven by retail (wealth financing) and commercial banking.

Indonesia saw a pick-up on the corporate loan sequentially, but will likely see a decline on a YoY basis, given the high base from 4QFY24. Loan growth from Thailand remains weak, dragged by chunky repayments and slow demand.

“While the group saw an increase in seasonal deposit competition similar to 4QFY24, we think that the repricing of deposits in Singapore and Thailand, supported by stabilising liquidity conditions at CIMB Niaga should help to offset the negative impact from the higher FD campaign rates,” said PIB.

PIB understands that the new deposit campaign rates for retail deposits were generally higher by 5-10 bps.

Following a strong 3QFY25 due to higher trading and FX income as well as NPL sales, NOII is expected to moderate on a quarter-on-quarter (QoQ) basis.

Nevertheless, PIB believes that NOII remains the key driver in supporting YoY earnings growth in FY25F.

“We also gather that the strong performance came in with higher bonus accruals in 3QFY25, which should see lower operating expenses sequentially,” said PIB.

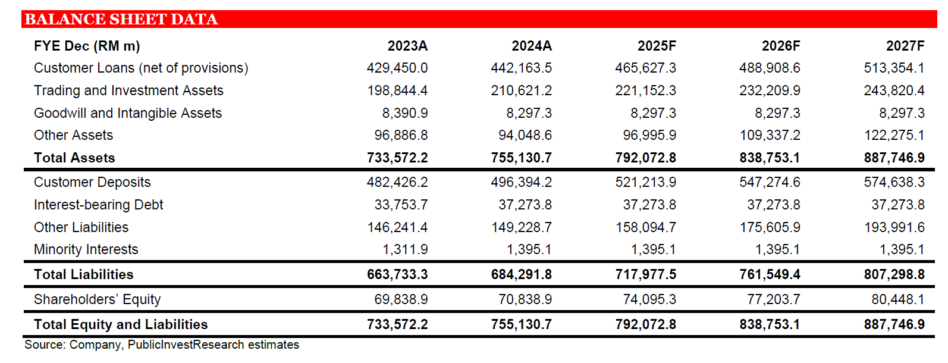

Management indicated that gross impaired loans ratio and loan loss coverage remained stable across key operating countries.

While its Indonesia operations saw a slight uptick in delinquencies from the consumer segment, this has yet to affect CIMB’s credit cost outlook or risk appetite.

“We expect net credit cost to ease sequentially, as CIMB updates its macroeconomic assumptions to reflect improving economic conditions, which should result in lower expected credit losses,” said PIB. —Jan 26, 2026

Main image: Utusan Malaysia