WITH THE latest round of payer pressure largely absorbed, RHB reaffirms their positive view on the sector going into 2026. RHB expects robust demand for private healthcare services, owing to structural tailwinds including:

i) Organic and inorganic expansion.

ii) Medical tourism boon (Malaysia Year of Medical Tourism 2026 (MYMT2026).

iii) Demographic drivers, such as inelastic demand for healthcare services, a rising middle-class and growing health awareness, as well as a rapidly ageing society.

The private healthcare sector enters 2026 against a backdrop of increasingly active policy intervention, primarily aimed at containing healthcare inflation.

“While none of the recent initiatives, in our view, amount to a disruptive overhaul, these efforts collectively signal a gradual but structural recalibration of how private healthcare is delivered, priced, and regulated,” said RHB.

At the same time, the Government’s push towards public-sector reform – particularly at the primary and secondary care levels – is expected to generate spillover effects for private providers.

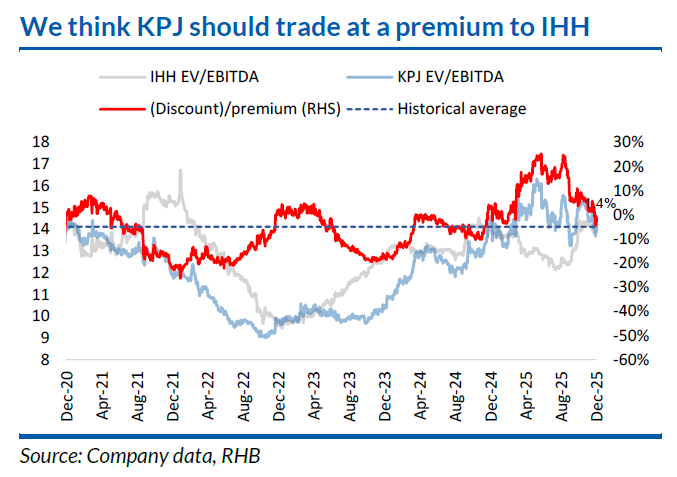

“We continue to favour KPJ for its robust margins and ROE, rising revenue intensity, and growing contribution from maturing hospitals, all of which provide better visibility on near-term earnings and margin expansion,” said RHB.

KPJ is entering a sweet spot as six hospitals transition from loss-making to bottom-line accretive, driving internal ROE expansion that is largely independent of medical tourism trends (5-7% of group revenue).

“Unlike IHH, we believe KPJ offers a refuge from MYR strength and lower growth dependency on medical tourism,” said RHB.

Also, while management remains focused on lifting revenue intensity via complex, high-value subspecialty cases, RHB thinks KPJ’s secondary care hospitals could be uniquely positioned to capture MHIT spillover, particularly where standardised “Base Plan” coverage meets the needs of the price-sensitive M40 segment, in their view.

RHB also maintains their BUY stance on IHH for its consistent execution, premium regional footprint, and affluent-patient focus that underpins its earnings resilience.

“Meanwhile, we like DBB for its solid earnings visibility and resilient pharmaceutical demand, from which the company is set to ride on margin tailwinds into 2026,” said RHB.

Risks identified by RHB include higher-than-expected operating costs, lower-than-expected patient visits/revenue intensity growth, and adverse regulatory changes.

Should the USD weaken meaningfully, IHH may face adverse FX translation effects on overseas earnings, while DBB could benefit from cost relief on imported active pharmaceutical ingredients. —Jan 27, 2025

Main image: Times Jobs