MAYBANK IB Research has initiated coverage on Wasco Greenergy Bhd (Greenergy) with a buy rating and a 12-month target price of 85 sen which is a 21% premium to its current share price of c.70 sen but still below the latter’s IPO (initial public offering) price of RM1.

The Shariah-compliant renewable-energy (RE) arm of Wasco Bhd (previously Wah Seong Corp Bhd) has debuted on the Main Market of Bursa Malaysia on Dec 11 with its shares traded between a high of 98 sen (on its maiden trading day) and 60.5 sen for the past one month.

According to the research house, its 85 sen target price is pegged to a 14x price-to-earnings ratio (PER) on Greenergy’s FY2026E earnings per share (EPS) which is the simple average multiple of its locally-listed peers – BM GreenTech Bhd (previously Boilermech Holdings Bhd) and Kawan Renergy Bhd.

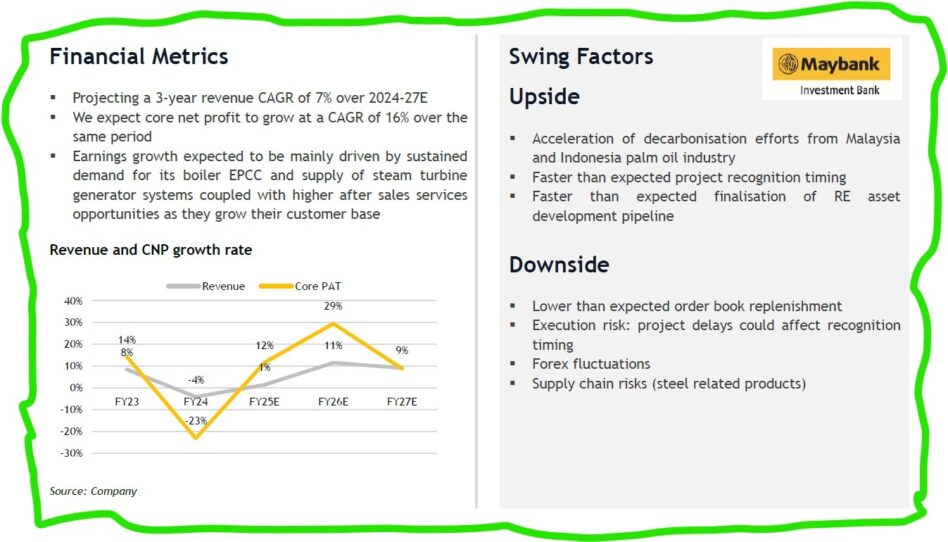

“Our FY2026/2027 EPS growth is underpinned by an upcycle of biomass boiler orders as successful bidders of the FiT (Feed-In Tariff) programme are expected to begin supplying electricity to Tenaga Nasional Bhd (TNB) by 2028,” justified analysts Jeremie Yap and Thong Kei Jun in the Maybank IB Research’s initial coverage report.

“(From here, they are expected) to continue industry drive towards decarbonisation, thus resulting in boiler & steam turbine orderbook replenishments.”

On the value proposition side, the research house acknowledges Greenergy as a comprehensive RE systems provider specialising in customised steam energy and steam turbine generator solutions

“It has proven track record with over 52 steam energy EPCC (engineering, procurement, construction, and commissioning) projects and 316 turbines delivered to 1,500+ customers,” observed Maybank IB Research.

“Post listing, the group intends to deepen its presence in the RE segment by expanding into an asset ownership model with an initial focus on biomass-based steam power plants.”

Prospect-wise, Greenergy holds a leading market share in steam turbine generator systems, with c.17% market share of Malaysia and c.22% in Indonesia. In this regard, the group is the second largest player in Malaysia’s biomass boiler market by commanding c.14% market share

In Malaysia, the overall biomass boiler and steam turbine markets is forecasted to grow at a CAGR (compound annual growth rate) of 9% and 8.1% respectively from 2024 to 2029E driven by growing adoption by palm oil plants and factories to achieve decarbonisation goals.

On contrast, the Indonesian biomass boiler and steam turbine markets are anticipated to expand at a CAGR of 11.2% and 8.6% from 2024 to 2029E underpinned by increasing adoption across key industrial sectors such as paper, rubber, F&B (food & beverage) and palm oil processing.

At the current valuations of 10x PER on Greenergy’s FY2026E EPS, Maybank IB Research expects Greenergy to present an opportunity to investors to gain exposure to a growing RE sector.

“Budget 2026 has announced plans to introduce another 300MW of quota for bioenergy and hydro projects under FiT2.0,” noted Maybank IB Research.

“While details are scarce at this juncture, we believe this development could further raise Greenergy’s total addressable market for biomass EPCC projects.”

At 2.40pm, Greenergy was down 1.5 sen or 2.11% to 69/5 sen with 496,000 shares traded, thus valuing the company at RM348 mil. – Jan 27, 2026

Main image credit: CGS International Securities Malaysia/Facebook