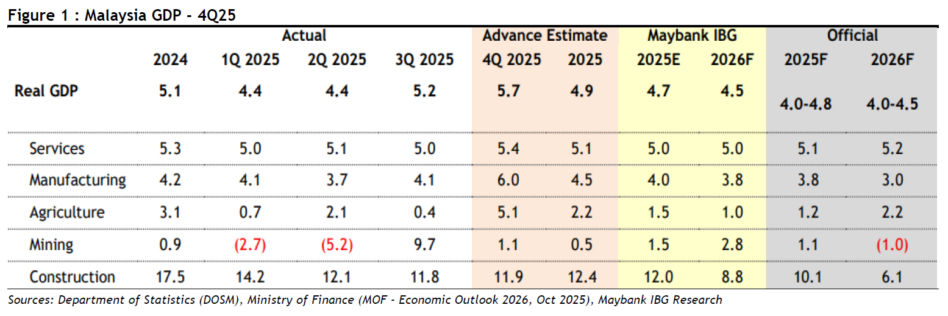

MALAYSIA’s quarter four 2025 (4Q25) real GDP advanced estimates based on Oct-Nov 25 data suggests that the economy posted another quarterly growth that surpassed 5%.

Domestic and external trade data indicate sustained domestic demand growth momentum, namely resilient consumer spending and on-going investment upcycle but weaker net external demand.

Final 4Q/full-year 2025 GDP will be out on 13 Feb 2026. The strong fundamentals together with the global AI boom are placing the MYR in pole position to outperform its regional FX peers in 2026.

Electronics exports are set to remain robust this year, improving Malaysia’s trade balance, while data centre construction continues to attract sizable foreign direct investment inflows.

These trends are unfolding alongside a broader domestic investment upcycle that appears set to remain firm in 2026.

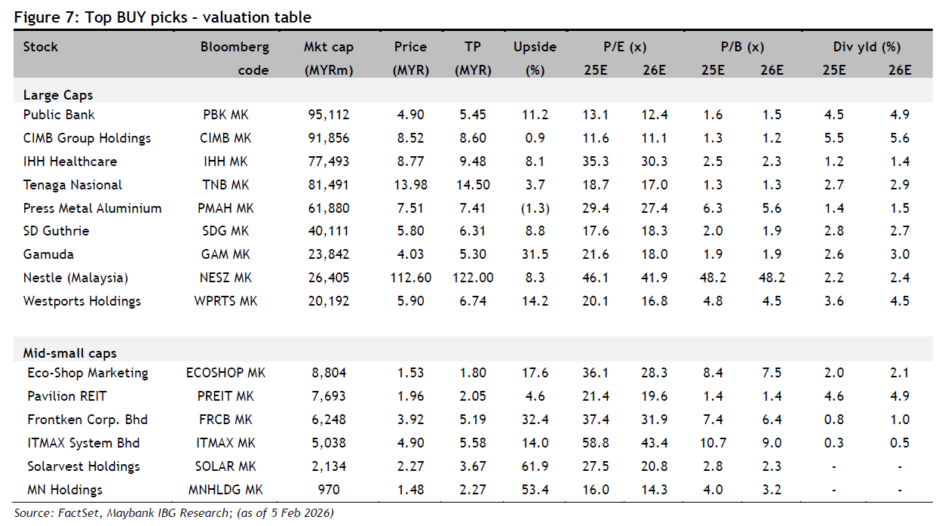

“Sectors we expect to see seasonally stronger results are autos, aviation consumer, ports & logistics and REITs,” said Maybank Investment Bank (MIB).

Aviation should also see strong tailwinds from the stronger MYR and lower jet fuel prices. With new job wins, MIB expects the construction and M&E players to deliver a stronger quarter ahead.

Meanwhile, MIB expects a better results season for healthcare (hospitals) and property sectors; the former should see payor pressures subside hence volumes would normalise, while the latter should see stronger progress billings.

“The tech sector, both hardware and software could see mixed results with forex volatility a key swing factor but in general, we expect most of the tech companies to post results within expectations,” said MIB.

Plantations too could see a mixed bag of 4Q25 earnings; while headline earnings could trend lower quarter-on-quarter due to softer crude palm oil prices, companies with a bigger presence in East Malaysia could perform better (IOI, KLK, SOP, TAH, THP).

The utilities sector could also see mixed results on a company specific basis (note MLK, YTLP and MFCB) but others should post stable earnings.

Similarly, the renewable energy players could see a mixed set of results as EPCC players should be driven by accelerated project recognition but companies relying on solar rooftop jobs could be weaker.

“Telcos should see stable earnings in 4Q25; however, we flag possible upside risk to dividends for fixed broadband players (TM and TIME),” said MIB.

The gloves sector should see flattish growth. MIB expects the banks to deliver within expectations earnings with no major surprises.

Expectations are however high on banks’ capital management plans, especially on higher dividends.

“We expect interest in Malaysian equities to stay strong for 2026, driven by improved market liquidity, sustained govt policy optimism, and a resurgence of emerging market foreign inflows,” said MIB. —Feb 9, 2026

Main image: AMRO