THE ESCALATION of conflict in the Middle East is not only reshaping oil markets—it is also accelerating a quieter but equally significant shift in global energy priorities: the push towards solar power.

At the heart of this shift lies solar panel production. Unlike oil, which is geographically concentrated, solar manufacturing is increasingly decentralised.

Countries such as China, the United States, and members of the European Union have ramped up investments in photovoltaic manufacturing capacity, aiming to secure their own energy independence while reducing exposure to external shocks.

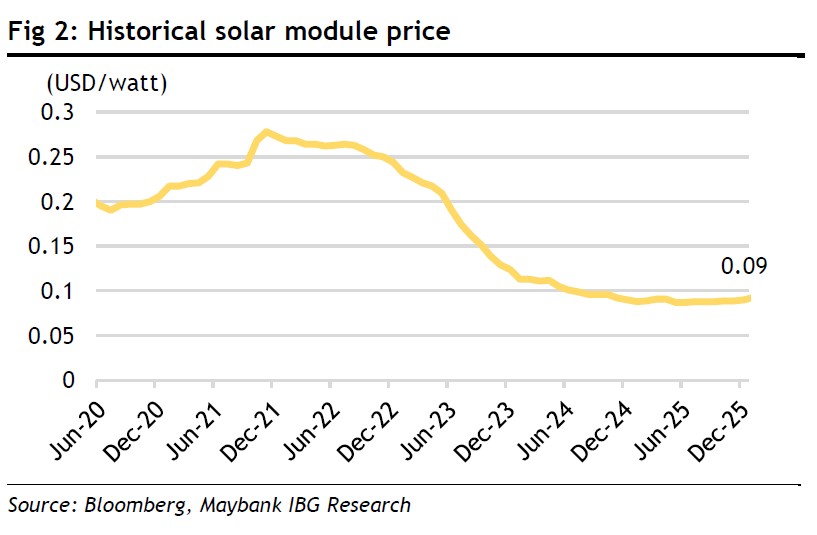

Maybank Investment Bank (MIB) reports that falling polysilicon and silver prices, which collectively account for 40-50% of module production cost, amid subdued solar panel demand have led to a notable reduction in module prices to USD0.11-0.12/watt, largely in line with industry expectations.

Meanwhile, ongoing tensions in the Middle East have heightened energy security concerns, reinforcing the longer-term structural shift toward renewable energy (RE) adoption.

“We remain Positive on the sector, underpinned by the structural upcycle in project deployment aligned with the National Energy Transition Roadmap (NETR) targets,” said MIB.

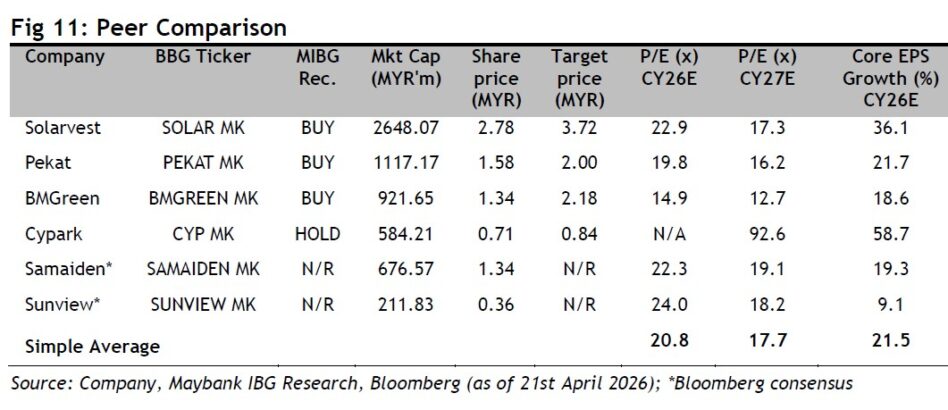

MIB’s top pick remains Solarvest. Recent geopolitical tensions in the Middle East, which have disrupted energy security, are likely to renew global focus on the transition toward RE.

“However, we believe any meaningful ramp-up in installed RE capacity on a grid level will take time, given the long lead times required for project planning and grid capacity allocation,” said MIB.

In the nearer term, MIB expects the recent reduction in TNB tariff AFA rebate to incentivise adoption of solar+BESS solutions for the C&I segment.

With better clarity that solar module prices are expected to stabilise at current levels or trend lower toward end of the year, they view this as a timely opportunity for investors to increase exposure to the sector.

MIB expects the RE sector to report stronger sequential results in quarter one 2026.

EPCC players with utility scale exposure are expected to be driven by completion of CGPP projects coupled with early-stage recognition from LSS5 projects.

While earnings for the rooftop solar players are expected to be driven by installation of solar + BESS solutions for the C&I segment. —Apr 22, 2026

Main image: Sembcorp