MALAYSIA HAS swiftly positioned itself as a major destination for data centre investments, attracting hyperscale players such as AWS, Google and Microsoft, which have collectively pledged more than USD16.5 bil.

Although non-disclosure agreements often keep project schedules under wraps, filings by listed contractors and fresh tenders—particularly in Springhill Industrial Park—point to a substantial, multi-year development wave already underway.

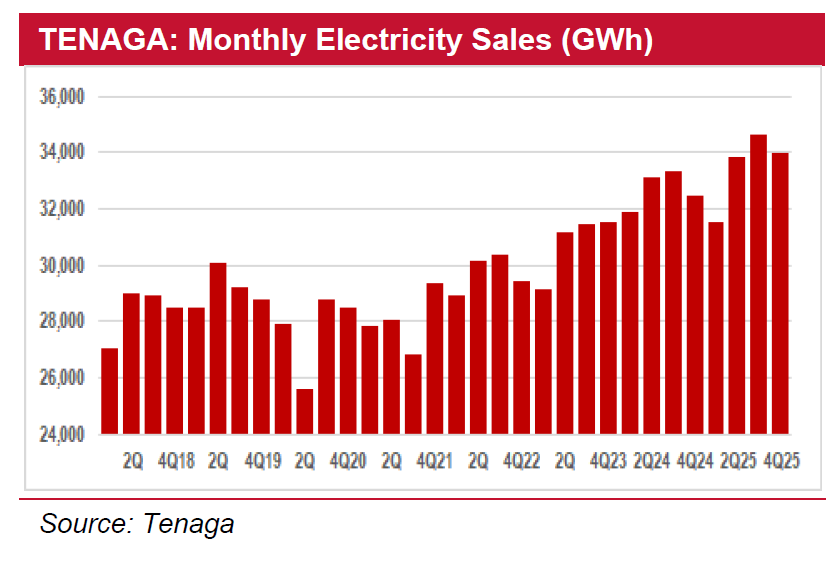

This shift signals a deeper transformation of the economy, where data centres are overtaking traditional sectors as the dominant source of baseload electricity demand.

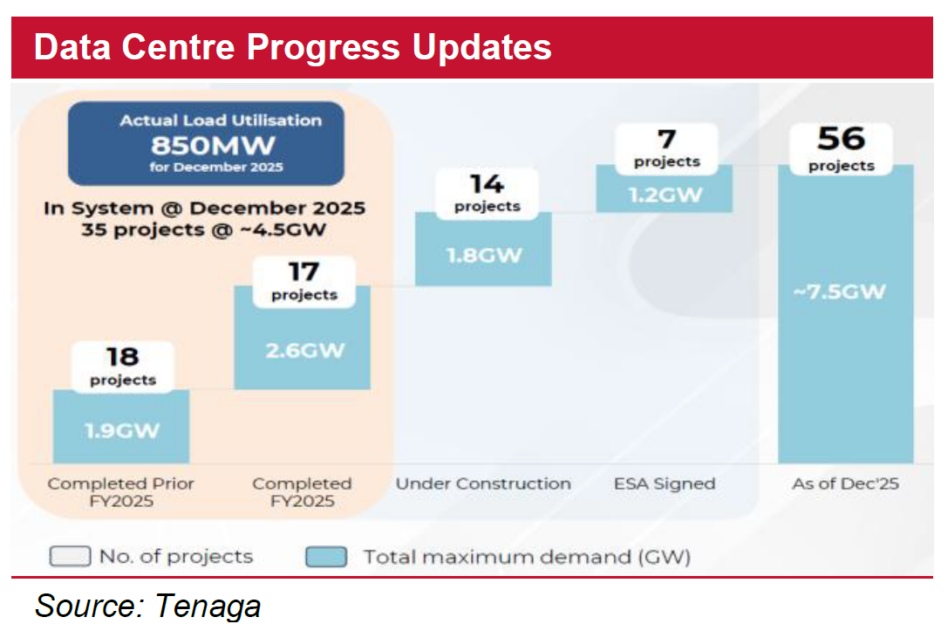

According to Kenanga, Tenaga’s 2025 filings indicate an extensive pipeline of 7,500MW spanning 56 projects, even as a sizeable gap between installed capacity and actual utilisation persists.

Total completed capacity has reached 4,500 MW, yet actual load stands at just 850 MW.

However, with load surging 6-fold since early 2024, this overhead represents a massive reservoir of pent-up demand poised to materialise as facilities reach full server-rack population through 2026.

With 6,400 MW of coal capacity retiring by 2031, natural gas has become Malaysia’s primary transition fuel, prompting the fast-tracking of two major RGTs.

Petronas is developing RGT3 in Lumut, while GASMSIA is progressing with an offshore RGT in Yan.

Strategic vertical integration is emerging as a key trend, with TENAGA and MALAKOF eyeing equity stakes in these terminals to de-risk fuel supply chains for their upcoming CCGT projects.

Simultaneously, TENAGA has entered a massive infrastructure super-cycle, with regulated capex jumping 108% to RM42.82 bil for the current regulatory period.

Driven by the Green Lane Pathway for data centres, this front-loaded investment will structurally expand TENAGA’s RAB, ensuring long-term earnings growth as the grid modernises to support 7,500 MW of new demand.

Ultimately, Malaysia’s power evolution is defined by the tension between rapid electrification and aging baseload capacity.

While the data centre wave secures multi-year demand upside, the looming retirement of 6,400 MW of coal necessitates an aggressive response through the NewGen26 tender and fast-tracked RGT projects.

Parallel to these shifts, the regulatory landscape is tightening; the 2026 Climate Change Bill and the implementation of a National Carbon Tax will act as catalysts for IPPs to accelerate decarbonisation and avoid margin erosion.

“We maintain our Overweight rating for the sector,” said Kenanga. —Apr 27, 2026

Main image: speakrj.com