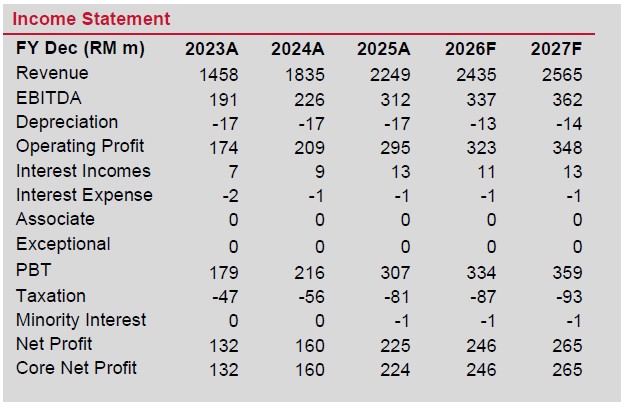

KERJAYA HAS secured a new construction contract worth RM529.3 mil through its wholly owned sub-subsidiary, Kerjaya Prospek (M) Sdn Bhd. The award was granted by first-time client BRDB Development Sdn Bhd.

The project involves the construction of a luxury residential development in Taman Duta, Bukit Tunku, Kuala Lumpur.

The development will comprise eight blocks of villa residences with a total of 146 units, alongside two dedicated car park blocks, two basement parking levels, a clubhouse and shared recreational facilities.

According to Kenanga Research, construction is slated to begin on June 15, 2026, with completion targeted within 33 months.

While the contract strengthens Kerjaya’s order book and provides earnings visibility over the medium term, margin expansion may remain challenging amid continued increases in construction material and labour costs.

The profit after tax margin for this project is expected to be in line at 10%.

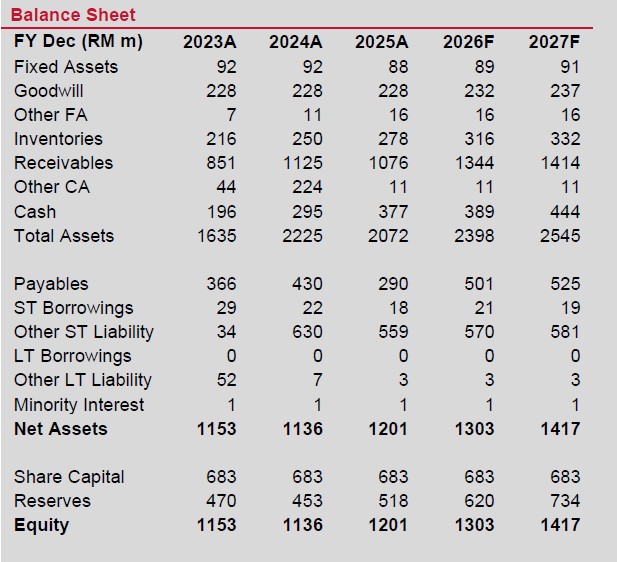

Management maintains a full-year 2026 job replenishment target of RM2.0 bil, backed by a healthy building tender book of RM2bil-RM3bil. In collaboration with its JV partner Samsung C&T, KERJAYA is also actively tendering for commercial factory projects locally.

Additional visible pipeline opportunities include up to RM2.0 bil worth of infrastructure packages at Andaman Island. It has also participated in the tender of Penang LRT Package 2.

Over the medium term, earnings visibility will be anchored by its 55%-owned Rivanis project, a 7-year strategic mixed redevelopment in Butterworth.

For upcoming launches, it plans to roll out two major developments next year: a project in Tanjung Bungah, Penang with a gross development value (GDV) of RM830 mil, and another at Jalan Puchong, Kuala Lumpur with an estimated GDV of RM800 mil.

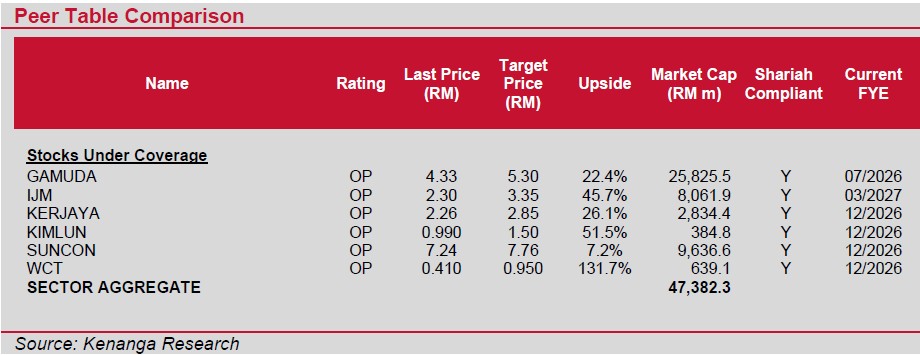

“We continue to like Kerjaya for its innovative and hence high-margin formwork construction method (10% net margin), lean and hands-on management team with a strong execution track record,” said Kenanga.

Also, Kerjaya possess strong earnings visibility underpinned by a sizable outstanding order book and recurring orders from related companies (such as E&O, KPPROP) of at least RM1bil a year.

Kenanga maintains Outperform for the stock. The stock also offers attractive dividend yields of more than 5%.

Risks to their call include further deterioration in the prospects for building jobs, rising input costs, and liquidated ascertained damages from cost overrun and delays. —June 16, 2026

Main image: dagangnews.com