MALAYSIA’S OIL and gas sector may be entering another growth phase, with analysts expecting stronger Petronas spending over the next two years amid resilient global crude oil prices.

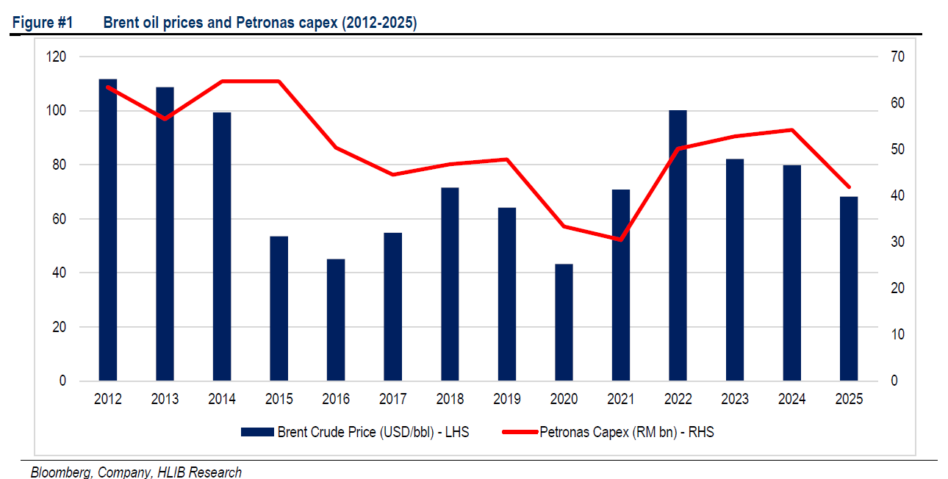

Petronas’ capital expenditure (capex) has historically tracked Brent crude oil prices with a correlation of 51%, albeit with a 1-year lag, reflecting project lead times and disciplined capital allocation.

During the 2012-2014 high oil price cycle, when Brent averaged USD107/bbl, Petronas sustained elevated annual capex of RM57-65 bil.

Similarly, the higher Brent price environment in 2022 supported a recovery in Petronas capex to RM53-54 bil in 2023-2024 as sector activity normalised post-pandemic.

“Also, we note that Petronas’ actual capex has generally moved within or close to its guided range,” said Hong Leong Investment Bank (HLIB).

Petronas’ net cash remained consistently positive over the last decade, providing a buffer for dividends.

“Should this historical relationship hold, we think that the sustained high Brent crude prices in 2026 (which we project to average USD90/bbl) could potentially translate into a new capex upcycle by 2027,” said HLIB.

Based on their observation, OGSE players’ revenue demonstrates a broad positive correlation with Petronas capex, though with a lag due to project award cycles and execution timelines.

During periods of stronger Petronas capex, such as 2012-2015 and 2022-2024, OGSE revenue trended higher, supported by improved activity levels, stronger order flows and better asset utilisation.

Conversely, the moderation in Petronas capex during 2016-2021 coincided with weaker OGSE revenue and margin pressure across the sector.

That said, the relationship is not perfectly linear, as revenue performance is also influenced by project mix, contract timing, utilisation rates, cost inflation and company-specific execution.

“Overall, the trend supports our view that a sustained recovery in Petronas capex would be positive for domestic OGSE players, with earnings impact likely to materialise progressively rather than immediately,” said HLIB.

HLIB views the possible Petronas capex upcycle in 2027 as positive for domestic OGSE players, particularly those with direct exposure to upstream development, HUC, maintenance, marine support, fabrication and pipeline-related works.

“We believe Dialog stands out as a key beneficiary given its strong exposure to tank terminal operations and 660 acres of available buffer land in Pengerang, which could potentially support an additional 4-5m cbm of storage capacity,” said HLIB.

With its strategic midstream positioning, we see growing opportunities for Dialog to further expand its storage footprint within the Pengerang region.

Based on HLIB’s channel checks, activity levels at Pengerang terminals have picked up recently, supported by vessel diversification and rerouting of trade flows amid the ongoing SoH disruptions.

“We maintain our Overweight rating on the sector, underpinned by sustained elevated Brent prices, potential Petronas capex upcycle by 2027, and rising energy security investments across the region,” said HLIB.

They believe the sector remains supported by stronger upstream earnings, improving OGSE order flows and longer-term demand for storage, pipeline and energy infrastructure. —May 18, 2026

Main image: scoop.my