MBSB RESEARCH remains cautiously optimistic on the sector with 2026 earnings visibility underpinned by strong order books, ongoing data centre projects and the expected rollout or finalisation of major infrastructure jobs in the second half 0f 2026 under the 13MP and Budget initiatives.

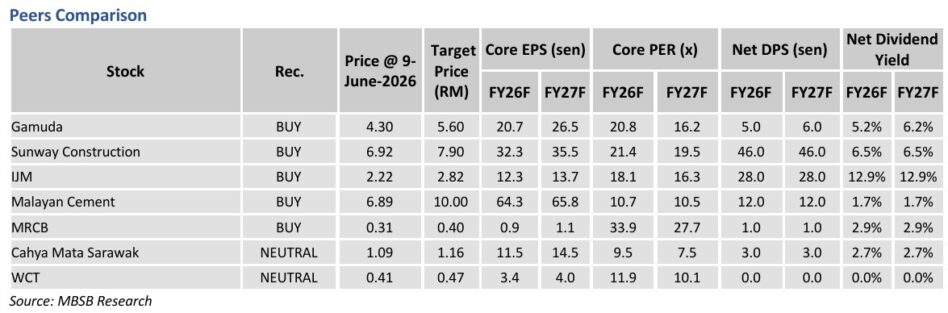

Contractors such as SunCon, IJM, MRCB and WCT continue to benefit from sizeable tender books and improving job flows, while Malayan Cement and CMS should remain a key beneficiary of stronger construction activity.

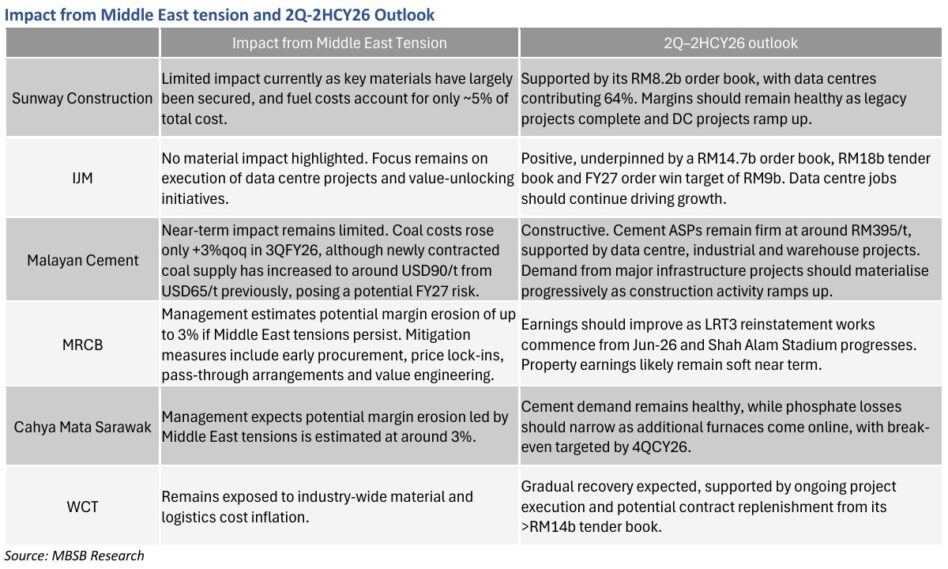

That said, near-term margins could face pressure from higher building material, coal and transportation costs, with the impact expected to be more visible in quarter two or three 2026 before gradually normalising.

Overall, MBSB expects the second half of 2026’s earnings to improve as project execution accelerates, partially offset by lingering cost inflation risks.

“Meanwhile, supported by continuous earnings growth, we anticipate a 2-7% dividend yield for stocks under our coverage,” said MBSB.

The average prices of steel bars in Malaysia heightened for the third consecutive month as of Apr-26, following a brief softening of prices in Jan-26.

Average prices rose +5.0% month-on-month in Apr-26 to RM2,347.50 per metric tonne, but still below the peak of RM3,500 per metric tonne recorded in Apr-22 during the height of the Russia-Ukraine conflict.

This was attributed to China’s elevated steel export levels in 2025, as its domestic demand remains sluggish amidst continuous property slump and weak industrial activity.

In line with the month-on-month trajectory, Apr-26 prices also rebounded to +5.2%yoy in Apr-26, translating to year-to-date growth of +8.8%.

As of Apr-26, the monthly average price for the binding substance has remained unchanged for the 5th consecutive month since Dec-25, holding steady at RM410 per metric tonne, supported by healthy demand from industrial developments and data centre projects.

However, while input cost pressures are beginning to emerge, the near-term impact remains manageable.

According to channel checks, coal costs increased marginally by +3% quarter-on-quarter in quarter one 2026 while electricity costs rose +8% quarter-on-quarter.

More recently, coal procurement costs have increased to approximately USD90/tonne from USD65/tonne previously.

This raises the possibility of higher cement production costs and potential price adjustments should elevated input costs across the construction supply chain persist throughout 2027.

“We maintain our POSITIVE stance on the construction sector, backed by a resilient private sector demand and stronger public project execution,” said MBSB.

Despite construction cost hikes brought about by cost inflation, MBSB expects the impact on sector earnings is expected to remain manageable, particularly for larger contractors with stronger contractual protections and more favourable project mix.

Data centre demand also remains structurally strong, with contractors continuing to secure hyperscale mandates as part of Southeast Asia’s ongoing digital infrastructure boom, supported by robust leasing demand, cost competitiveness, and long-term client partnerships.

Coupled with active industrial job flows and the multi-year public infrastructure roadmap under RMK-13 – including large-scale public transport infrastructure expansion, flood mitigation, and the projected RM430.0 bil federal development allocation, complemented by RM120.0 bil in GLIC funding and RM61.0 bil in PPP and private capital, MBSB expects earnings visibility to strengthen into 2026.—June 10, 2026

Main image: Getty Images