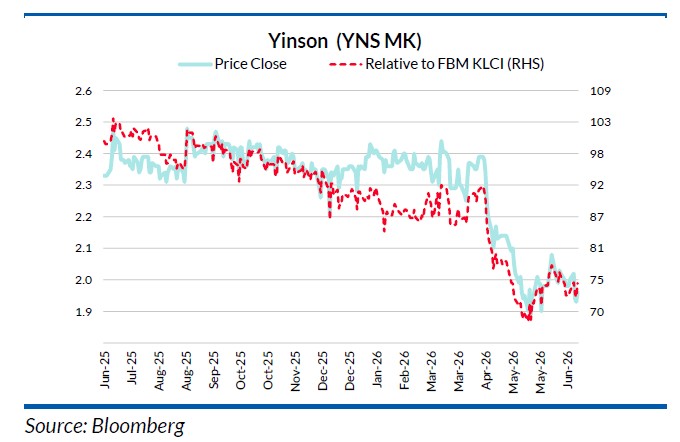

YINSON’S transition from project construction to long-term FPSO operations continued to bear fruit, lifting earnings and cash flow despite lower quarterly revenue.

Quarter one financial year 2027 revenue declined 15% year-on-year (YoY) to MYR1.05 bil, primarily due to the absence of Engineering, Procurement, Construction, Installation, and Commissioning (EPCIC) revenue.

This follows the completion of Floating Production, Storage, and Offloading (FPSO) Agogo and the commencement of its charter on 12 Aug 2025.

This was partly offset by higher recurring charter income from FPSO Agogo (MYR274 mil).

Nevertheless, core net profit surged by 26% YoY to MYR121 mil, driven by the full-quarter contribution from FPSO Agogo’s operations, marking the group’s continued transition from the EPC phase to the operations phase.

More importantly, operating cash flow turned positive at MYR689 mil, reflecting the group’s transition from an EPC-led business model to one that is increasingly underpinned by recurring charter income as construction-related cash outflows tapered off.

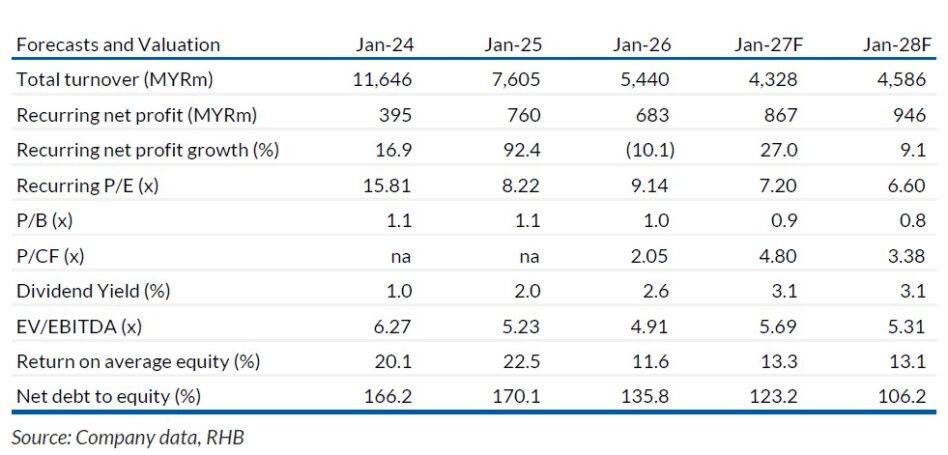

“We remain constructive in our medium-term outlook for Yinson, underpinned by a growing base of recurring FPSO charter income and a robust USD19.3 bil orderbook that provides long-term earnings visibility through 2050,” said RHB.

Underlying earnings should strengthen on the back of a full-year contribution from FPSO Agogo in 2027, while FSO Lac Da Vang remains on track for first oil in quarter four of 2026, providing an incremental earnings contribution towards the end of 2027 and a more meaningful uplift from 2028 onwards.

Meanwhile, the group’s balance sheet risk continues to improve following FPSO Agogo’s transition to non-recourse financing and stronger operating cash flow generation.

Key downside risks include the inability to win new jobs, and contract terminations.—June 26, 2026

Main image: Dagang News