THE LOCAL tech sector earnings were broadly mixed in the recently concluded quarter one calendar year 2026 (1QCY26) reporting season, with FX headwinds and selected cost inflation following the US-Iran conflict emerging as key swing factors.

Front-end semiconductor companies continued to benefit from healthy enquiry levels, driven by sustained investments in semiconductor fabrication facilities worldwide.

For outsourced semiconductor assembly and test players, earnings and business prospects remained largely steady as manufacturers continued to synchronise production plans with the evolving product strategies of their major customers.

Automated test equipment providers also remained well positioned to capitalise on the industry’s current growth cycle, with management expecting stronger demand for automation solutions in the quarters ahead.

However, the electronics manufacturing services (EMS) segment continued to face challenges.

Weaker demand from end markets, coupled with margin pressure arising from unfavourable foreign exchange fluctuations, weighed on near-term performance and outlook.

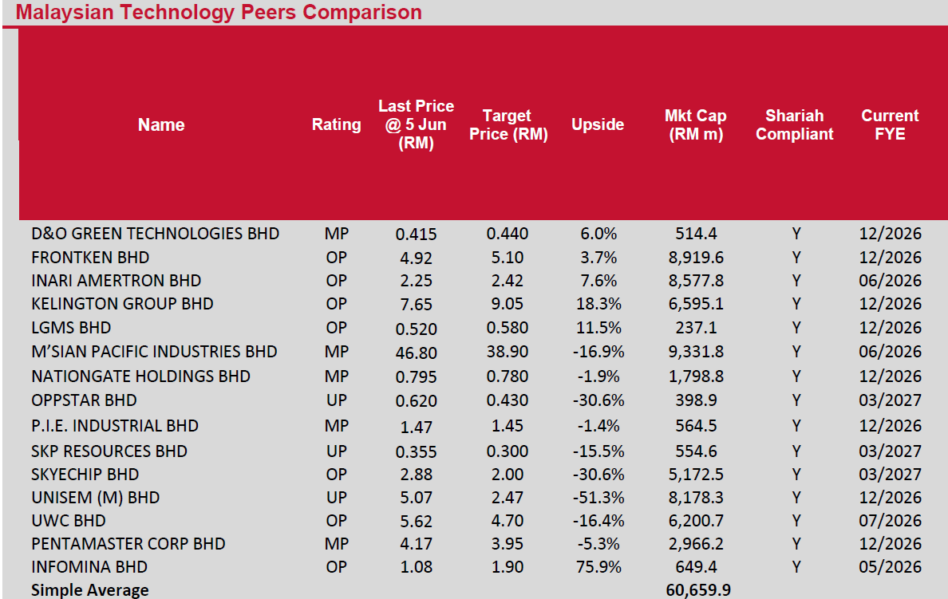

Kenanga Research (Kenanga) had downgraded SKPRES rating to underperform from Market Perform, given the ongoing margin pressure and uncertainty surrounding the company’s outlook.

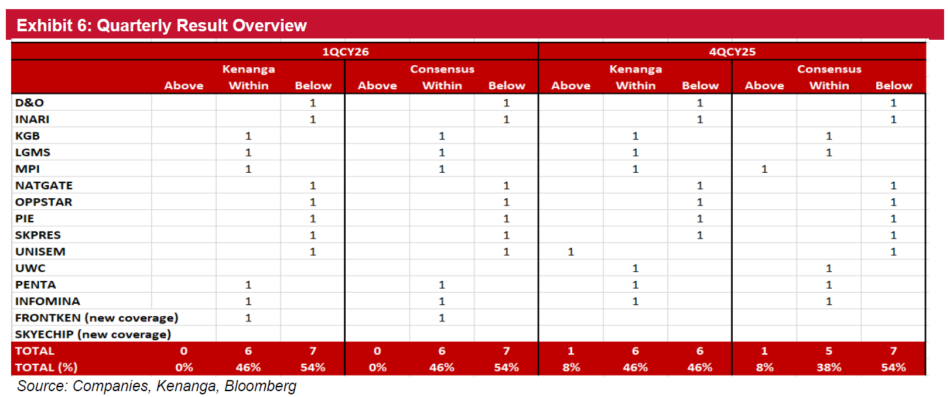

Overall earnings delivery softened versus the previous quarter.

Based on Kenanga’s coverage universe, none of the companies reported earnings above their or consensus expectations in 1QCY26.

Instead, 46%, or six companies, delivered results broadly in line with expectations, while 54%, or seven companies, came in below expectations.

This compares with the 4QCY25 reporting season, where 8% of companies exceeded expectations, 46% were in line, and 46% missed expectations.

The absence of positive earnings surprises in 1QCY26 suggests that earnings expectations had largely caught up with the sector’s recovery narrative, leaving less room for upside surprise.

In Kenanga’s assessment, the latest earnings season suggests a more differentiated outlook for the technology sector.

Although long-term growth catalysts such as artificial intelligence (AI) investments, global semiconductor fabrication expansion, advanced packaging requirements and increasing automation demand remain firmly in place, earnings performance in the near term is becoming less consistent.

This is largely due to factors including foreign exchange fluctuations, rising operating costs and varying demand trends across individual companies.

As a result, investors may need to adopt a more selective approach, focusing on businesses with stronger earnings visibility, resilient margins and meaningful exposure to front-end semiconductor activities, automated test equipment, advanced packaging and AI-driven supply chain opportunities.

At the same time, caution may be warranted for EMS companies that are more vulnerable to softer end-market demand and currency-related headwinds.

“While we continue to hold a constructive view on the longer-term prospects of the AI and semiconductor industry cycle, we believe disciplined stock selection will be increasingly important in navigating the sector over the coming quarters,” said Kenanga.

Kenanga continues to like the front-end names KGB, UWC, FRONTKN and software name INFOMINA due to their stronger order visibility, margin resilience and direct exposure to front-end, and AI-related supply-chain opportunities, while remaining cautious on EMS names with weaker end-demand and higher FX sensitivity.

Given that INARI, KGB, MPI, OPPSTAR and UNISEM have each surged by more than 50% over the past three months, a healthy pullback would not be surprising should sector momentum soften. —June 8, 2026

Main image: hcamag.com