RHB’s outlook for the cement and aluminium sectors remains upbeat, underpinned by potential project wins from upcoming Budget 2026 announcement and easing trade volatility. Margins should also remain stable, supported by the stabilising prices of raw materials.

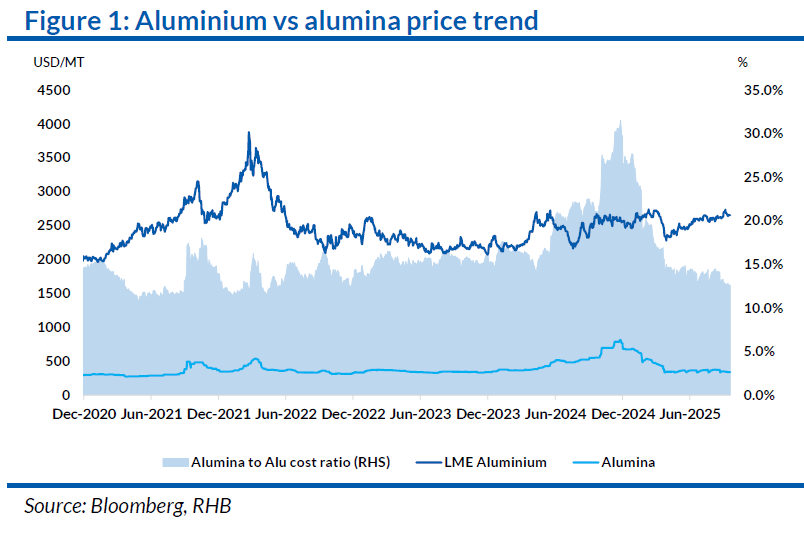

Press Metal (PMAH)’s 1H25 core earnings of MYR950 mil, +2% year-on-year (YoY) were supported by the increase in aluminium prices YoY, though earnings before interest, tax, depreciation and amortisation margins narrowed, due to higher alumina prices over the period (+12% YoY).

Meanwhile, LMC’s FY25 (Jun) core profit of MYR678 mil (+35% YoY) was mainly driven by stronger margins from improved operational efficiencies and lower coal costs.

“We believe geopolitical risks are largely priced in at this juncture,” said RHB.

LME aluminium has recovered to USD2,600-2,700/tonne, after dipping to USD2,300/tonne in April on US tariff concerns. The 90-day delay in US tariffs on China potentially lifted sentiment and eased nearterm demand risks.

On supply, global supply output was up only +1% YoY in year-to-date (YTD) Aug 2025, with Europe constrained by limited smelting capacity while China remains capped at 45 mil tonnes, underpinning near-term price support.

That said, Main Japanese Port (MJP) premium has fallen 73% YTD due to higher supply in Asia, whereas the US-Midwest premium surged 230% YTD.

Costs remain supportive for smelters. Alumina prices have halved YTD to USD334/tonne vs 31% in Dec 2024), well below the 5-year average of 17.6%, as Guinea’s supply chain normalised. Prices should stay favourable with 1 mil tonne new capacity in Bintan.

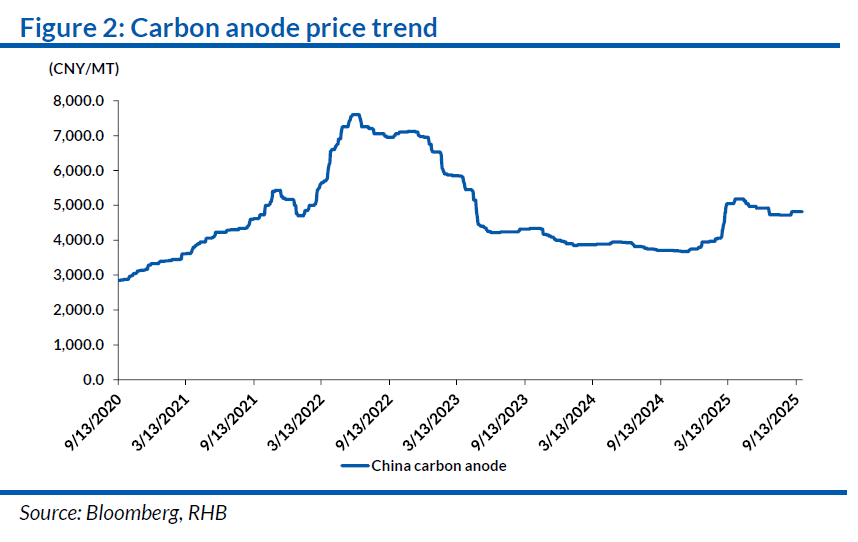

Carbon anode prices, meanwhile, have trended higher in YTD Aug 2025 (+25% YoY), due to rising petroleum coke prices as some refineries in northeast China undergo maintenance, hinting at tighter supply.

LMC kept average selling price (ASP) stable in FY25, despite gradual hikes by peers. With a dominant 60-70% market share and stabilising coal prices, it is comfortable maintaining current ASP levels.

“We expect stability to persist, underpinned by demand from infrastructure projects anticipated in the Budget 2026 announcement,” said RHB.

Key downside risks are rising input costs and a global slowdown, which could tamper construction activity and weaken demand for aluminium and cement. —Oct 7, 2025

Main image: A & L