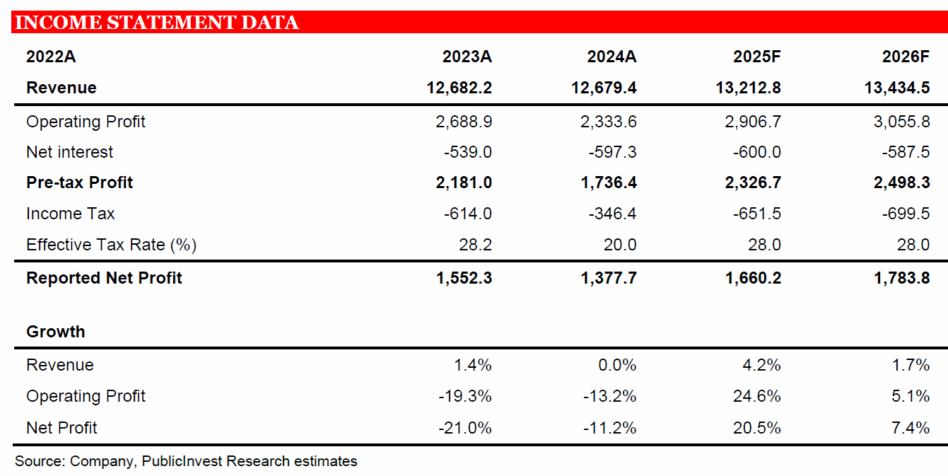

CELCOMDIGI Bhd’s (CDB) posted a net profit of RM341 mil for quarter three financial year 2025 (3QFY25), down 22% year-on-year (YoY) mainly due to higher costs and provision for expected credit losses.

For the nine months of financial year 2025 (9MFY25), results were below expectations due to higher allowances for credit losses.

As of end September, CDB’s network integration and modernisation has reached over 90% completion, providing customers with improved service quality as the monthly data usage increased to 40GB per user.

The group remains on track to deliver steady-state annualised cost savings of RM700-800 mil beyond FY27.

“We maintain our Neutral rating with a revised target price of RM3.80,” said Public Investment Bank (PIB).

Service revenue increased 1.5% YoY, driven by higher contribution from postpaid, home fibre and enterprise solutions. Postpaid revenue rose 4.2% on higher subscriber base and continued migration to convergence plans.

Prepaid revenue was stable despite a slight decline in subscriber base from effective base management to focus on retaining quality subscribers.

3QFY25 profit after tax, amortisation, and minority interest fell 22% YoY, mainly due to higher traffic-related costs and higher provision for expected credit losses.

Management has guided that it is looking at improving the collection process in order to control the increase in ageing trade receivables.

“In the near-term, we are concerned over the viability of Digital Nasional Bhd (DNB) in championing the primary role in the deployment of 5G wholesale network in Malaysia,” said PIB.

As competition is likely to heighten once U Mobile fully rolls out the second 5G network in mid-2026, having partnering with more experienced tech suppliers like Huawei and ZTEC, PIB believe DNB’s market share will be affected.

Holding a 19.44% stake, CDB has so far invested RM350 mil in DNB, including RM116.67 mil shareholder advance that will be interest-free and likely to be treated as prepayments to offset future access fee payments.

“We do not rule out the possibility of further advances or equity investments required to sustain the operations of DNB while it continues to be a loss-making unit,” said PIB.

For now, the fundamentals of CDB remain intact as it gradually reaping the benefits of the synergistic merger that should lead to further cost savings and market share gain.

The major shareholder of CDB, Telenor ASA, has indicated plans to develop a sovereign and sustainable “artificial intelligence factory” in Malaysia.

Given its experience in Norway, Telenor sees an opportunity to work with the Malaysian government to develop a scalable AI infrastructure, which could also offer services to CDB’s sizable customer base of over 20 mil users. —Nov 18, 2025

Main image: New Straits Times