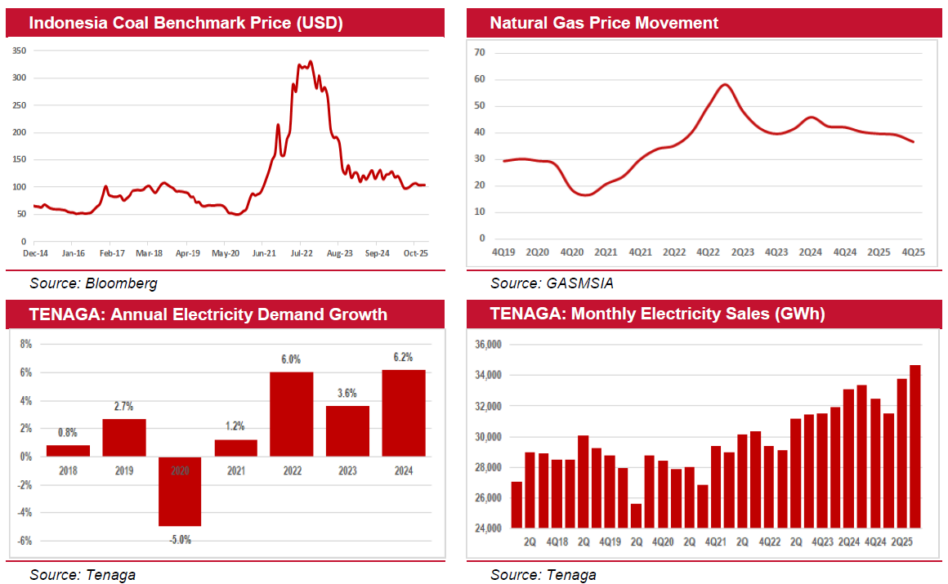

WE MAINTAIN our financial year 2026 (FY26) electricity demand growth forecast at 3.5%. Following a seasonal contraction in quarter one financial year 2025 (1QFY25), electricity sales in Peninsular Malaysia rebounded strongly in 2QFY25 and remained firm in 3QFY25.

This is underpinned mainly by commercial demand linked to data centre expansion.

The nine months of financial year 2025 (9MFY25) electricity sales grew by 1.6%. Data centre load utilisation rose sharply to 710MW in Sep 2025 from 503MW in Jun 2025.

As at Sep 2025, 29 data centre projects with total capacity of 3,800MW have been completed, including 11 projects (1,900MW) commissioned during 9MFY25.

Eight new Electricity Supply Agreements (ESAs) were signed, adding 1,100MW, bringing the total to 49 ESAs with cumulative capacity of 7,100MW.

While demand growth is embedded within the IBR framework and capped by revenue mechanisms, stronger demand still enhances plant efficiency and drives higher transmission capex to meet data centre-related high-voltage requirements, both of which are earnings-positive for TENAGA.

With a tight timeline to deliver 6GW-8GW of new generation capacity by 2030 to meet structurally rising demand from data centres, outcomes for greenfield power plant RFPs are expected by end-2025 or early-2026. Construction is likely to commence from end-2026, alongside ongoing extensions of existing and expiring PPAs.

With no new coal-fired plants planned, gas-fired generation remains the key swing capacity to support demand growth. Natural gas consumption in Peninsular Malaysia is already heavily driven by the power sector, with TENAGA reporting a 36.4% gas mix in FY24.

Kenanga expects gas-fired generation to rise toward 50% by 2030, supported by:

(i) data centre-driven electricity demand.

(ii) progressive coal plant retirements.

(iii) the addition of 6GW-8GW of new gas capacity.

In mid-June, Petronas confirmed plans for a third regasification terminal (RGT), with PETGAS the likely operator given its ownership of the existing Sungai Udang (Melaka) and Pengerang (Johor) terminals.

Lumut has been cited as the preferred location due to its proximity to MALAKOF’s gas assets and TNB Janamanjung (4,100MW coal plant), where three 700MW units are set to retire by 2030 and the remaining 1,000MW by 2040 – making them prime candidates for gas conversion.

“We also understand GASMSIA is keen to participate in future RGT developments to support longer-term earnings growth. No new RGT assumptions have been incorporated into our forecasts at this stage,” said Kenanga.

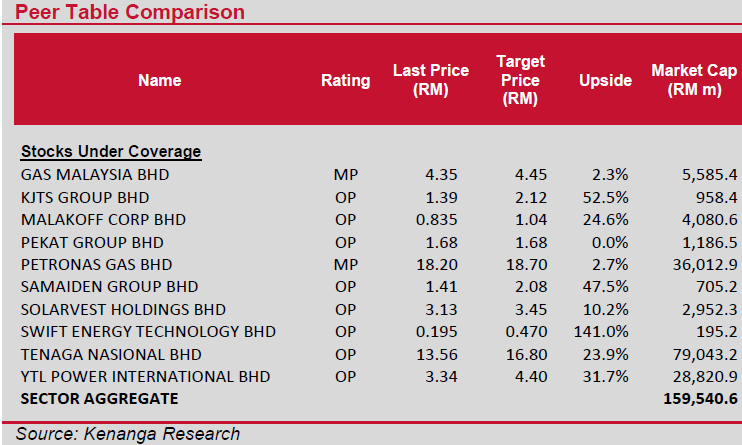

Kenanga continues to rate the utilities sector OVERWEIGHT. TENAGA remains their tp[ pick, as the long-term primary beneficiary of the data centre boom, given its exposure to demand growth, the T&D capex up-cycle, and new capacity build-outs.

Meanwhile, the IRB tax dispute has been fully resolved, with TENAGA securing MoF approval for Investment Allowance on qualifying capex, to be offset against future taxable income. Independent power producers such as MALAKOF and YTLPOWR also stand to benefit from both brownfield extensions and greenfield opportunities.

Meanwhile, rising gas demand underpins positive earnings prospects for PETGAS and GASMSIA. Overall, the sector offers earnings resilience underpinned by regulated assets and stable cash flows, supporting attractive yields of up to 6%, particularly from GASMSIA. —Jan 9, 2025

Main image: Getty Images