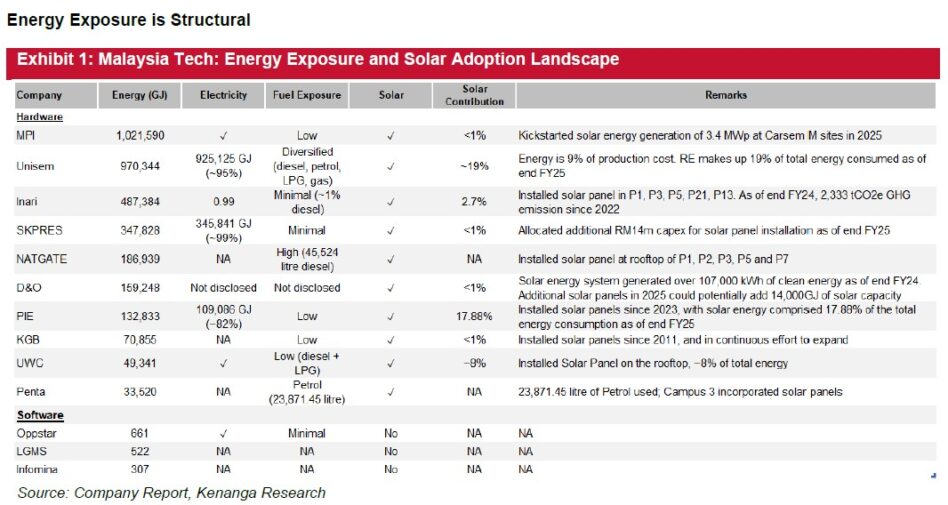

A REVIEW of the most recent annual reports at the company level suggests that electricity from the national grid continues to dominate the energy mix among Malaysian technology firms.

The data shows a clear concentration of consumption in grid power across the sector.

Companies such as Inari and Unisem rely overwhelmingly on electricity to meet their operational needs. Similarly, SKPRES and PIE demonstrate a strong dependence on grid supply.

This trend extends to smaller players like UWC, where electricity still forms the backbone of energy usage, with only minimal reliance on alternative fuels.

Taken together, the evidence points to a structurally grid-focused energy model within the industry. Other energy sources — including diesel, petrol and natural gas — tend to play a supporting role, typically reserved for backup or supplementary purposes rather than serving as primary inputs.

Although fuel consumption is not pervasive across all companies, it remains significant for certain players, exposing them to fluctuations tied to oil prices.

At the same time, solar energy is gradually gaining ground. A growing number of Malaysian tech firms are beginning to adopt solar solutions, with all companies in the sample either already implementing such initiatives or indicating plans to move in that direction.

“However, despite this progress, solar energy remains in the early stages of integration and has not yet reached a transformative level in terms of the overall energy mix,” said Kenanga.

The updated table also shows that solar adoption is becoming more widespread at the operational level, with installations now disclosed across a broader set of companies including MPI, Inari, NATGATE, SKPRES, D&O, PIE, KGB, UWC, and Penta.

Expansion efforts remain ongoing, as seen in MPI’s 3.4MWp rollout at Carsem M in 2025, SKPRES’s additional RM14m capital expenditure allocation, and D&O’s plan to add 14,000GJ of solar capacity in 2025.

While this points to a strengthening pipeline, current renewable penetration remains below 20% for nearly all companies except Unisem and PIE, indicating that solar is still insufficient to fully offset near-term energy shocks or meaningfully shield margins in the immediate term.

“In our view, this supports a medium-term positive read-through, but not yet a near-term earnings hedge,” said Kenanga.

From an investor perspective, while the sector is structurally exposed to energy cost volatility, the earnings impact is partially mitigated by cost pass-through mechanisms.

Broadly across the Malaysian tech sector, fluctuations in key input costs such as electricity are typically passed through to customers with a lag of ~1–2 quarters, cushioning longer-term margin erosion.

“Our engagement with management indicates that, given the industry’s reliance on short-cycle purchase orders, pricing for new orders is regularly adjusted to reflect prevailing cost dynamics, including energy prices,” said Kenanga.

That said, this lag effect implies that companies could still face temporary margin compression in the near term, particularly during periods of sharp energy price spikes.

As such, while Kenanga do not see energy cost inflation as a structural threat to profitability, it remains a timing-driven earnings risk, with near-term margins more vulnerable for players with higher energy intensity or limited hedging mechanisms.

Over the medium term, companies with stronger pricing discipline, higher renewable adoption, and better energy management are likely to outperform on margin resilience. —Apr 24, 2026

Main image: