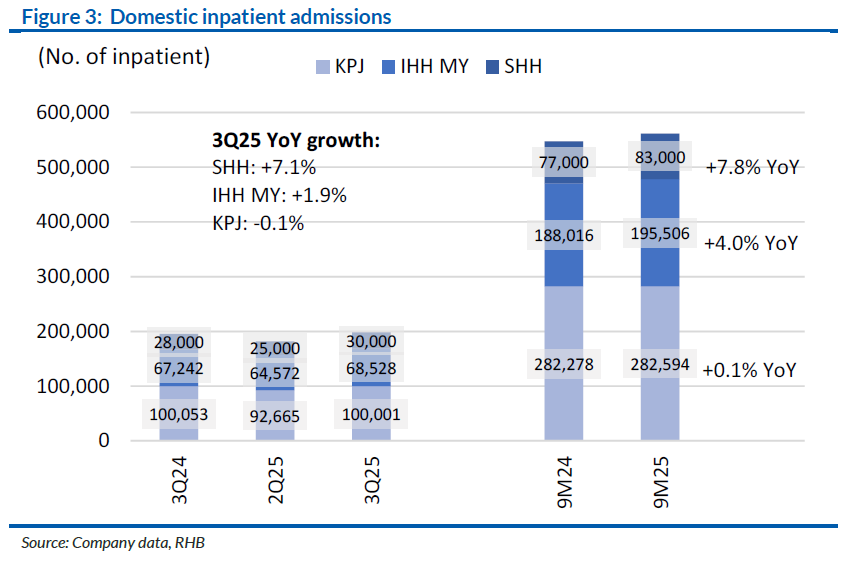

SECTOR results for Sep 2025 were broadly in line. Effects of payer pressure are visible, with a clear shift towards day-care models that are weighing on inpatient volumes.

Still, quarter three 2025 (3Q25) revenue intensity continued to rise, while earnings before interest, tax, depreciation and amortisation (EBITDA) margins benefitted from higher bed occupancy and operational efficiencies.

With the current iteration of payer pressure largely concluded, managements’ forward guidance was generally optimistic, hinging on sustained uplift in revenue intensity, selective bed expansions at high-occupancy hospitals, and holistic cost management.

“Sector domestic inpatient admissions in 3Q25 slowed to +1.7% year-on-year (YoY) amid payer pressure that is driving a structural shift in the case mix towards day care, with KPJ appearing to be the most impacted,” said RHB.

Nevertheless, revenue intensity continues to trend upwards on a favourable mix of higher-value cases, efficiency gains, and a steady pick-up in medical tourists.

3Q25 domestic EBITDA margins dipped marginally, weighed by hospitals still under gestation and payer pressure.

Both operators under coverage are sharpening cost controls and scaling up centralised procurement of medical devices, consumables, and pharmaceuticals to defend margins.

“Looking ahead, we believe the structural shift towards day care could underpin longer-term EBITDA margin expansion, as day care offers greater efficiency and lower overheads,” said RHB.

With adequate scale, day-care margins are typically higher, while freed-up inpatient capacity can be redeployed to higher acuity or surgical cases – addressing capacity bottlenecks while being payer friendly.

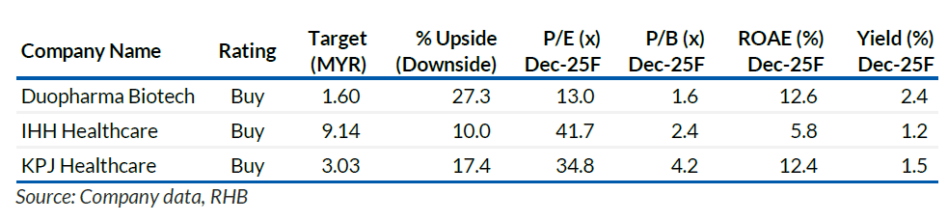

RHB still favors KPJ for its superior margins and ROE, rising revenue intensity, and growing contribution from maturing hospitals, providing better visibility on near-term earnings and margin expansion.

“We continue to like KPJ as a solid turnaround play and as the strongest proxy to Malaysia’s thriving private healthcare landscape,” said RHB.

They also maintain BUY on IHH for its consistent execution, premium regional footprint, and affluent-patient focus that underpins its earnings resilience.

Meanwhile, RHB likes DBB for its solid earnings visibility and resilient pharmaceutical demand, which is set to ride on margin tailwinds into 2026. Higher-than-expected operating costs, lower-than-expected patient visits/revenue intensity growth, and adverse regulatory changes. —Dec 5, 2025

Main image: world economic forum