THE PLASTIC packaging sector continues to face multiple headwinds including trade disruptions from U.S. tariffs, intense competition and currency fluctuations, leading to poor visibility for calendar year 2026 (CY26).

However, demand for premium, consumer-used packaging products remained encouraging but even so, average selling prices (ASP) are facing pressures from falling resin prices, in addition to the above-mentioned factors.

This trend is also reflective in the charts, showing weaker profit before tax (PBT) despite broadly stable aggregate revenues.

“We see small direct impact for the Malaysian plastic packaging sector from higher U.S. tariffs as exports to U.S. amount to below 10% of overall revenue,” said Kenanga.

However, trade tension has created uncertainties for many businesses and a significant portion of plastic packaging films is used in B2B trades including inter-country trade to ease shipping and logistics.

Any slowdown or decline in global trade volumes is thus likely to dampen overall demand for plastic packaging materials.

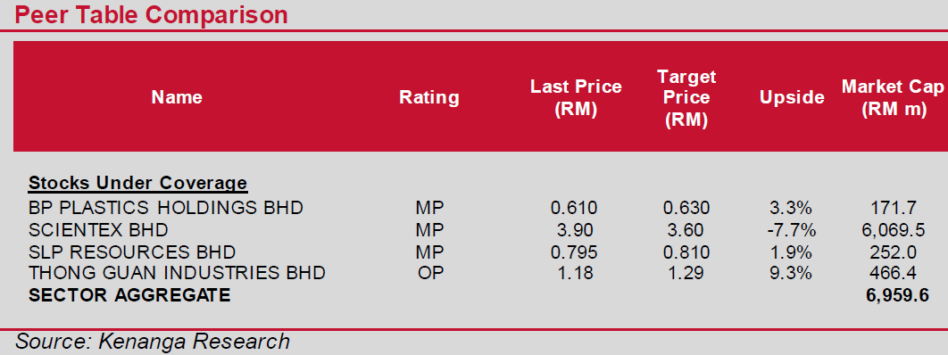

On that note, SCIENTX stood out for being the only player among our coverage that runs a plant in Arizona, USA, which in quarter two to quarter three of financial year 2025, has shown improved orders and possibly better ASP as well to meet US demand.

Since CY24, plastic packaging players have been facing not only slower demand growth but more intense competition as well due to overcapacity.

Part of this arises from manufacturers maintaining their old facilities even after having upgraded to newer ones, such as the new thin-gauge production lines.

This allows for operational flexibility but also very competitive marginal pricing for “old” packaging products. Compounding this is demand shifting away from China by some U.S. and European buyers which in turn compel Chinese players to offload stock at lower prices to other buyers such as those in SE Asia.

“Notably, following our visit to one of China’s largest plastic packaging exhibitions in Shanghai, our findings indicate that such competitive pressures are likely to persist with the likelihood of escalating further moving forward,” said Kenanga.

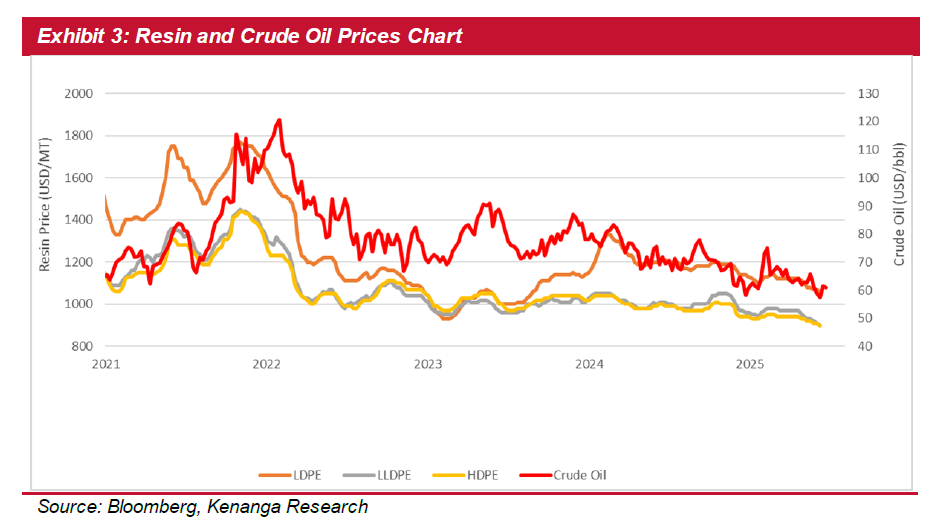

In the second half of calendar year 2025, Kenanga observed resin prices declining in the range of 10% to 15% on a year-on-year basis, leading to lower ASP in general for the sector.

Based on their on-the-ground checks with industry players, resin prices are anticipated to remain soft in the next 12 months, which is also consistent with the US Energy Information Authority’s bearish view on the global crude oil pricing trend for 2026. —Jan 23, 2025

Main image: Shutterstock