FOLLOWING Hong Leong Investment Bank (HLIB)’s recent engagement with the Malaysia Healthcare Travel Council (MHTC), healthcare tourism revenue for the first quarter of 2026 was broadly on track to meet the full-year target of RM3.8 bil.

That said, MHTC noted that growth during the second quarter may have fallen short of earlier expectations due to disruptions caused by the Iran conflict.

The situation led to flight cancellations and higher airfares across parts of the Middle East, affecting travel demand. Despite these headwinds, the council has retained its RM3.8 bil revenue target for 2026 while awaiting the release of second-quarter figures.

“We expect demand for essential medical services, particularly complex and tertiary care, to remain relatively resilient as such treatments are generally less likely to be postponed,” said HLIB.

In contrast, elective procedures such as health screenings and in-vitro fertilisation (IVF) are more vulnerable to softer demand, as patients may delay travel in response to higher transportation costs.

Separately, HLIB believes IHH’s overseas operations are also exposed to the recent geopolitical tensions in the Middle East. Around 30% of Fortis Healthcare’s international patient revenue is derived from the Middle East.

Meanwhile, Acıbadem generated 14% of its 2025 revenue from healthcare tourism and has a significant presence in Türkiye, which geographically borders Iran.

Going into the second half of 2026, HLIB remains cautiously optimistic on a sequential recovery, underpinned by MHTC’s efforts to penetrate new source markets and improving geopolitical conditions following progress in US-Iran negotiations, which have contributed to a 30% decline in Brent crude oil prices from their peak, which has in turn eased jet fuel prices as well.

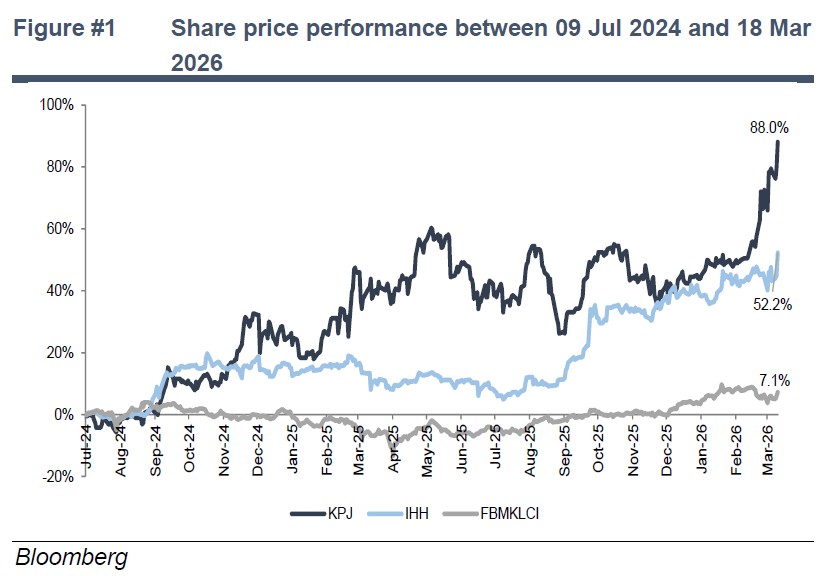

HLIB continues to prefer KPJ, underpinned by its stronger earnings margin expansion potential through ongoing cost optimisation initiatives across its secondary hospitals, as well as its gradual transition towards higher-margin tertiary care via the rollout of 15 Centres of Excellence by 2030.

In addition, KPJ stands to benefit from potential fund inflows should the KLCI expand to 50 constituents, while its relatively lower exposure to healthcare tourism provides greater earnings resilience amid recent geopolitical tensions.

HLIB also remains positive on SunMed, supported by its differentiated business model and strong clinical credentials.—July 10, 2026

Main image: charteredaccountantsworldwide.com