THERE has been no significant impact to earnings of Kossan Rubber Industries Bhd despite the recent surge in COVID-19 and monkey pox cases, according to AmBank Research.

While Kossan expects earnings to normalise in 2Q FY2022, the research house foresees lower quarter-on-quarter (qoq) earnings due to excess global supply dragging average selling prices (ASP) even further.

“Kossan anticipates the ASP for blended gloves to stay under pressure for the next six to 12 months owing to price adjustments amid intensified competition,” revealed the research house following a recent meeting with the Big-Four glove maker.

“However, the company believes that its strong cash balance of RM2.3 bil will help the group navigate through the headwinds.”

Against such backdrop, AmBank Research reiterated its “hold” rating on Kossan with a lowered fair value of RM1.23/share (from RM1.60/share previously) based on FY2023F PE (price-to-earnings ratio) of 14.9 times which is one standard deviation below the five-year pre-pandemic average PE of 17 times.

On this note, the research house slashed its net profit estimates for FY2022F by 8% and that of FY2023F by 13% due to:

- 10%-25%-point cut in plant utilisation rate from the normalised level of 85%;

- Higher operating cost from increased natural gas price and electricity tariffs; and

- Lower nitrile glove average selling price (ASP) assumptions of US$24.50/US$24.7 per 1,000 pieces (previously US$25.00/24.90 per 1,000 pieces) for FY2022F/FY2023F.

“Our FY2022F–FY2024F earnings are below consensus by 14%-35%,” AmBank Research pointed out.

While the glove maker’s utilisation rate has recovered to 75% compared to 70% in April 2022, this remains below its normalised level of 85%. This is sufficiently supported by its current workforce of above 7,000 although the management is seeking more workers, according to AmBank Research.

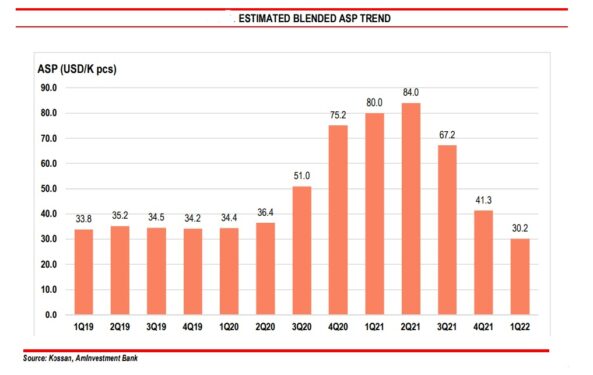

Recall that Kossan’s 1Q FY2022 net profit tumbled 58.6% qoq to RM90.6 mil from blended ASP prices falling 22-27% to an estimated USS$30 per 1,000 pieces.

“This compressed profit margin (is) further exacerbated by the lower utilisation rate of 70% (from 85-90% in 1Q FY2021) stemming from rising competition from glove suppliers and heightened raw material prices, partly offset by higher demand in technical rubber products,” justified AmBank Research.

“We expect nitrile glove ASP to stabilise at US$25,000 per 1,000 pieces within our FY2022F-FY2023F assumptions. We estimate Kossan’s breakeven ASP for nitrile gloves at US$22.50 per 1,000 pieces.”

Very broadly, AmBank Research remains cautious on the industry’s medium-term prospects given that market consolidation could suppress ASP until 1H FY2023 coupled with lower sales due to logistic disruptions and intensified competition.

“The stock currently trades at a high FY2022F PE of 16 times amid a structural downturn compared to troughs of below 10 times over the past five years,” added AmBank Research.

At the close of yesterday’s (July 14) trading, Kossan was up 1 sen or 0.78% to RM1.29 wiith 2.65 million shares traded, thus valuing the company at RM3.3 bil. – July 15, 2022